Pfs assignment 3

ŌĆóDownload as PPT, PDFŌĆó

1 likeŌĆó2,209 views

This document provides an overview of demand, supply, and market equilibrium. It begins with introducing the key concepts of demand, including the law of demand which states that as price increases, quantity demanded decreases. Supply is also introduced, with the law of supply stating that as price increases, quantity supplied also increases. Market equilibrium is explained as the price where quantity demanded equals quantity supplied. The document then discusses how equilibrium can change if either demand or supply shifts due to various factors such as income, prices of related goods, technology, and more. Examples are provided to illustrate these concepts and how equilibrium adjustments occur when demand or supply changes.

Pfs assignment 3

- 1. Chapter 2 & 4 DEMAND, SUPPLY & MARKET EQUILIBRIUM 1

- 2. Presentation This presentation is a mash up of 3 sources. They are: ŌĆóHariff, A.(2011). Chapter 4, The forces of Supply and Demand. ŌĆóKanth, J.(2013). Demand and Supply. ŌĆóShin, S.(2011). Chapter 2, Demand and Supply Market Equilibrium. 2

- 3. Chapter Outline ŌĆó 1.1 Introduction: Market and the Circular Flow ŌĆó 1.2 Demand (DD) ŌĆó 1.3 Supply (SS) ŌĆó 1.4 Market Equilibrium ŌĆó 1.5 Change in Equilibrium (SS & DD) ŌĆó 1.6 SS/DD Analysis: Example 3

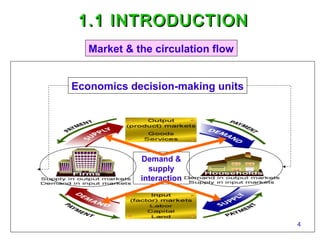

- 4. 1.1 INTRODUCTION Market & the circulation flow Economics decision-making units Demand & supply interaction 4

- 5. Markets 5

- 6. 1.2 DEMAND Relationship between price & quantity demanded How many packs of ŌĆśai yu bingŌĆÖ will student buy at a price of RM2? What if the price is RM1.50? ŌĆó Quantity consumers are both willing and able to buy at each possible price during a given time period, other things constant. ŌĆó can be defined as the purchase of product 6

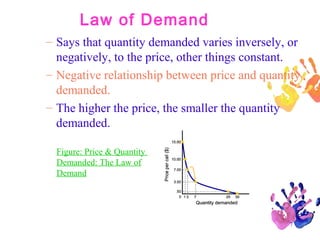

- 7. Law of Demand ŌĆō Says that quantity demanded varies inversely, or negatively, to the price, other things constant. ŌĆō Negative relationship between price and quantity demanded. ŌĆō The higher the price, the smaller the quantity demanded. Figure: Price & Quantity Demanded: The Law of Demand 7

- 8. Demand Schedule & Demand Curve ŌĆō The demand schedule is a table that shows the relationship between the price of the good and the quantity demanded. ŌĆō The demand curve is a graph of the relationship between the price of a good and the quantity demanded. ŌĆó Downward sloping & to the right because law of demand. 8

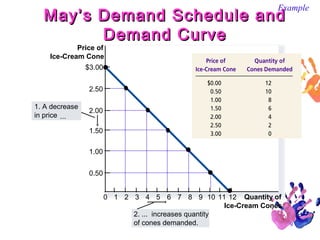

- 9. MayŌĆÖs Demand Schedule and Demand Curve Example Price of Ice-Cream Cone $3.00 2.50 1. A decrease in price ... 2.00 1.50 1.00 0.50 0 1 2 3 4 5 6 7 8 9 10 11 12 Quantity of Ice-Cream Cones 2. ... increases quantity of cones demanded. 9

- 10. Individual Demand & Market demand ŌĆō The individual demand is the relationship between the quantity demanded by a single buyer and its prices ŌĆō The market demand is the relationship between the total quantity demanded by all consumers in the market and its price. 10

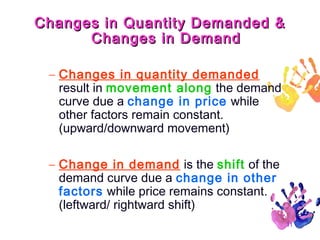

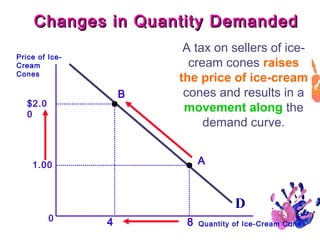

- 11. Changes in Quantity Demanded & Changes in Demand ŌĆō Changes in quantity demanded result in movement along the demand curve due a change in price while other factors remain constant. (upward/downward movement) ŌĆō Change in demand is the shift of the demand curve due a change in other factors while price remains constant. (leftward/ rightward shift) 11

- 12. Changes in Quantity Demanded Price of IceCream Cones B $2.0 0 A tax on sellers of icecream cones raises the price of ice-cream cones and results in a movement along the demand curve. A 1.00 D 0 4 8 Quantity of Ice-Cream Cones 12

- 13. Change in Demand ŌĆó A shift in the demand curve either to the left or right caused by any changes that alters the quantity demanded at every price. Such as: ’é¦ ’é¦ ’é¦ ’é¦ ’é¦ Income Prices of related goods Tastes Expectations Number of buyers 13

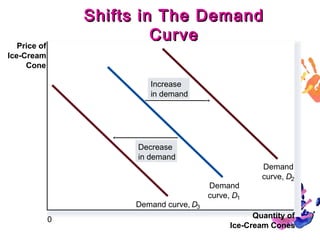

- 14. Shifts in The Demand Curve Price of Ice-Cream Cone Increase in demand Decrease in demand Demand curve, D3 0 Demand curve, D1 Demand curve, D2 Quantity of 14 Ice-Cream Cones

- 15. Substitution Effect ŌĆó Substitution Effect: ŌĆó - When the price of a good rises, consumers will substitute away to other goods ŌĆó - Holding real purchasing power constant, an increase in the price of a good relative to others, raises the opportunity cost of consuming that good, and therefore demand strictly decreases ŌĆó - for ALL goods then: Ōåæ own price, SE sees Ōåō quantity demanded

- 16. Changes in Consumer Income ŌĆó Goods can be classified into two broad categories: ’é¦ Normal goods: the demand increases when income increases and decreases when income decreases ’é¦ Inferior goods: the demand decreases when income increases and increases when income decreases 16

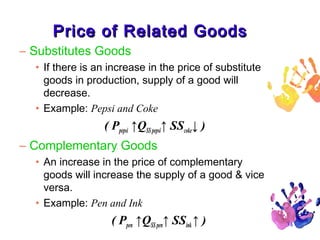

- 17. Changes in Price of Related Good - - (i) Substitute Goods A product that can be used in place of another product A change in the price of substitute products affect the demand for the product in the same direction in which the price change. E.g: tea vs coffee; a bus ride vs an LRT ride ( P coffee Ōåæ Q dd coffee Ōåō DD tea Ōåæ) 17

- 18. Changes in Price of Related Good - - (ii) Complementary Goods A product that is used in conjunction with another product. The change in the price of a complementary product affects the demand for the product in the opposite direction to the change price. E.g: a disk and computer, pen and ink. ( P pen Ōåæ Q dd pen Ōåō DD ink Ōåō ) 18

- 19. Taste & Preference ŌĆō Tastes and preferences of consumers change significantly. ŌĆō If a product become more fashionable, the demand for it will increase and if the same product becomes outdated, the demand for it will fall. ŌĆō E.g: Changes in music, apparel or recreation. 19

- 20. Expectations ŌĆō The higher the expected future price of a product, the higher the current demand for that product and vice versa. ŌĆō E.g: When the government plans to increase the price of sugar the following week, the demand for sugar will immediately increase. 20

- 21. Population or Number of Buyers ŌĆō A larger population with a high rate of growth creates greater demand for goods and services. ŌĆō E.g: An increase in the population of UTAR would increase the demand for houses, F & B, and other goods and services. 21

- 22. 1.3 SUPPLY ŌĆó Supply indicates how much of a good producers are willing and able to offer for sale per period at each possible price, other things constant ŌĆó Law of supply states that the quantity supplied is usually directly related to its price, other things constant ’é¦ The lower the price, the smaller the quantity supplied ’é¦ The higher the price, the greater the quantity supplied 22

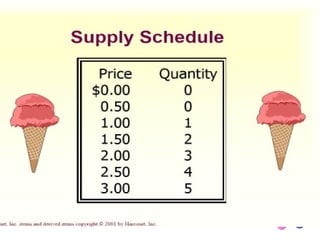

- 23. Supply Schedule & Supply Curve ŌĆō The supply schedule is a table that showing how much of a product firms will set at different prices. ŌĆō The supply curve is a graph illustrating how much of a product a firm will set at different prices. ŌĆó Upward slopping & to the right due to the law of supply. 23

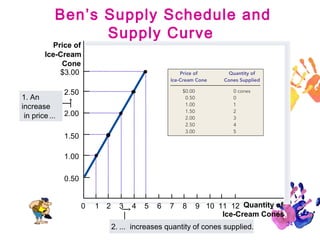

- 24. BenŌĆÖs Supply Schedule and Supply Curve Price of Ice-Cream Cone $3.00 1. An increase in price ... 2.50 2.00 1.50 1.00 0.50 0 1 2 3 4 5 6 7 8 9 10 11 12 Quantity of Ice-Cream Cones 2. ... increases quantity of cones supplied. 24

- 25. 25

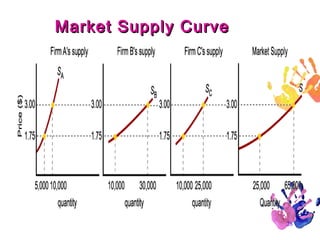

- 26. Individual Supply & Market Supply ŌĆō The individual supply is the relationship between price of good and the quantity an individual producer is willing and able to sell per period, other things constant. ŌĆō The market supply is the sum of all that is supplied each period by all producers of a single product. 26

- 27. 27

- 29. 29

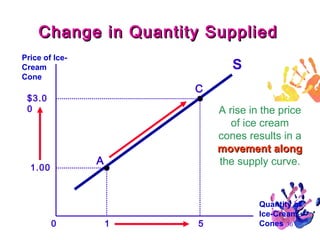

- 30. Change in Quantity Supplied Price of IceCream Cone S C $3.0 0 A rise in the price of ice cream cones results in a movement along the supply curve. A 1.00 0 1 5 Quantity of Ice-Cream Cones 30

- 31. Changed in Supply ŌĆó A shift of the supply curve, either to the left or right. ŌĆó Determinants of supply other than the price of the good ’é¦ Technology ’é¦ Prices of related goods ’é¦ Expectation ’é¦ Number of sellers 31

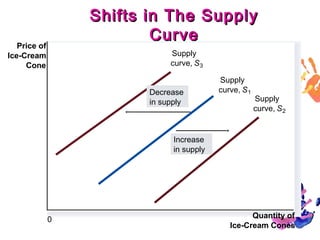

- 32. Shifts in The Supply Curve Price of Ice-Cream Cone Supply curve, S 3 Decrease in supply Supply curve, S 1 Supply curve, S 2 Increase in supply 0 Quantity of 32 Ice-Cream Cones

- 33. Technology ŌĆō Represents the economyŌĆÖs knowledge about how to combine resources efficiently. ŌĆō If a better technology is discovered, production costs will fall. Thus, suppliers will be more willing & able to supply the good at each price. ŌĆō Example: when new technology are introduced in the production of sushi, supply of sushi will increase and shift the supply curve. 33

- 34. Price of Related Goods ŌĆō Substitutes Goods ŌĆó If there is an increase in the price of substitute goods in production, supply of a good will decrease. ŌĆó Example: Pepsi and Coke ( Ppepsi ŌåæQSS pepsiŌåæ SScokeŌåō ) ŌĆō Complementary Goods ŌĆó An increase in the price of complementary goods will increase the supply of a good & vice versa. ŌĆó Example: Pen and Ink ( Ppen ŌåæQSS penŌåæ SSink Ōåæ ) 34

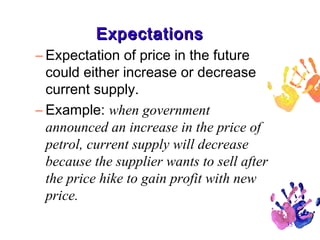

- 35. Expectations ŌĆō Expectation of price in the future could either increase or decrease current supply. ŌĆō Example: when government announced an increase in the price of petrol, current supply will decrease because the supplier wants to sell after the price hike to gain profit with new price. 35

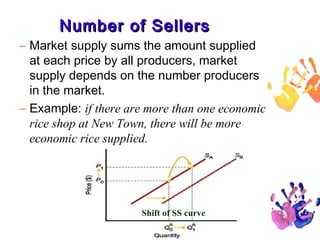

- 36. Number of Sellers ŌĆō Market supply sums the amount supplied at each price by all producers, market supply depends on the number producers in the market. ŌĆō Example: if there are more than one economic rice shop at New Town, there will be more economic rice supplied. Shift of SS curve 36

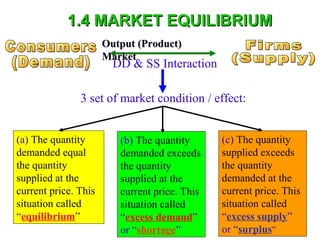

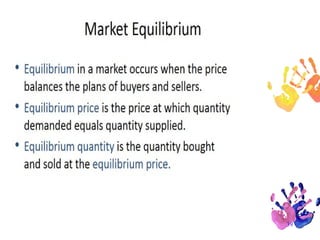

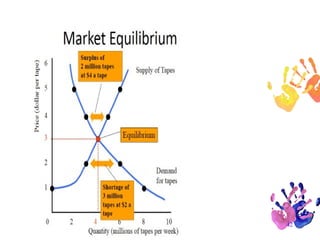

- 37. 1.4 MARKET EQUILIBRIUM Output (Product) Market DD & SS Interaction 3 set of market condition / effect: (a) The quantity demanded equal the quantity supplied at the current price. This situation called ŌĆ£equilibriumŌĆØ (b) The quantity demanded exceeds the quantity supplied at the current price. This situation called ŌĆ£excess demandŌĆØ or ŌĆ£shortageŌĆØ (c) The quantity supplied exceeds the quantity demanded at the current price. This situation called ŌĆ£excess supplyŌĆØ 37 or ŌĆ£surplusŌĆØ

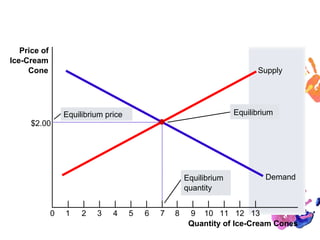

- 38. Equilibrium Price of Ice-Cream Cone Supply $2.00 Equilibrium Equilibrium price Equilibrium quantity 0 1 2 3 4 5 6 7 8 Demand 9 10 11 12 13 Quantity of Ice-Cream Cones 38

- 39. 39

- 40. 40

- 41. 41

- 42. 42

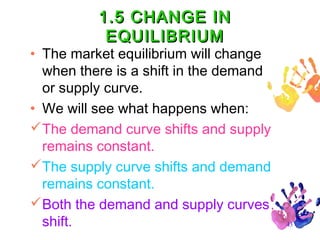

- 43. 1.5 CHANGE IN EQUILIBRIUM ŌĆó The market equilibrium will change when there is a shift in the demand or supply curve. ŌĆó We will see what happens when: ’ā╝The demand curve shifts and supply remains constant. ’ā╝The supply curve shifts and demand remains constant. ’ā╝Both the demand and supply curves shift. 43

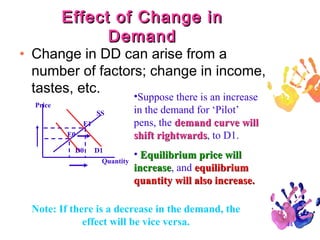

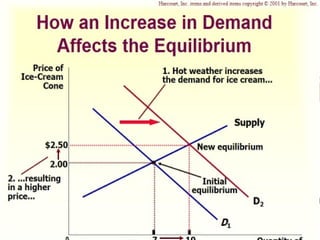

- 44. Effect of Change in Demand ŌĆó Change in DD can arise from a number of factors; change in income, tastes, etc. ŌĆó Price SS E1 E0 D0 D1 Quantity Suppose there is an increase in the demand for ŌĆśPilotŌĆÖ pens, the demand curve will shift rightwards, to D1. rightwards ŌĆó Equilibrium price will increase, and equilibrium increase quantity will also increase. Note: If there is a decrease in the demand, the effect will be vice versa. 44

- 45. 45

- 46. 46

- 47. 47

- 48. 48

- 49. 49

- 50. References This presentation is a mash up of 3 sources. ŌĆóKanth, J.(2013). Demand and supply. http://www.slideshare.net/jnchandrakanth/demand-and-supply29294711 Accessed 06 March 2014 ŌĆóShin, S.(2011).Chapter 2, Demand and Supply, Market Equilibrium. http://www.slideshare.net/SusuJie/chap2-7165119 Accessed 06 March 2014 ŌĆóHariff, A.(2011). The market forces of Demand and Supply. http://www.slideshare.net/AminHanif/lecture-4-10007901 Accessed 06 March 2014 50