Super Project

Download as PPTX, PDF7 likes24,801 views

The document summarizes the valuation of the Super Project being considered by General Foods. It identifies three methods used by General Foods to evaluate projects - incremental, facilities used, and fully allocated - each with advantages and disadvantages. The document recommends evaluating the Super Project using an incremental cash flow analysis that accounts for relevant cash flows and avoids non-cash expenses. It concludes the Super Project has a positive NPV and IRR above the discount rate under two of the three methods, so the investment should be undertaken.

More Related Content

What's hot (20)

Similar to Super Project (20)

Super Project

- 1. Valuation of the Super Project Group Members: XXX XXXXX XXX XXXXX Gordon Schwabe XXX XXXXX 27.01.2013

- 2. AGENDA 1. Case summary 2. Problem statement 3. Clarifying problems & solutions 4. Comments on the 3 evaluation approaches 5. Recommendations on evaluation 6. Cash flow statement 7. Conclusion Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 2

- 3. Case Summary âĒ General Foods is a large corporation organized by productl âĒ Super is a proposed new instant desert, based on a âflavored, water- soluble, agglomerated powder.â âĒ General Foods has numerous projects with a strict criteria to judge their value for the company âĒ There are basically three types of capital investment proposals at General Foods: âĒ Safety âĒ Quality âĒ Increased profit Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 3

- 4. Problem Statement âĒ 3 methods, each passes with advantages and disadvantages âĒ Incremental / Facilities used / Fully allocated âĒ Memos indicate that General Foodsâ finance personnel are questioning the same criteriaâs ability to accurately reflect the value of the Super project âĒ No precise estimation of company value, because of the high variance in the evaluation methods Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 4

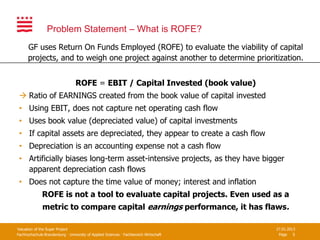

- 5. Problem Statement â What is ROFE? GF uses Return On Funds Employed (ROFE) to evaluate the viability of capital projects, and to weigh one project against another to determine prioritization. ROFE = EBIT / Capital Invested (book value) ï Ratio of EARNINGS created from the book value of capital invested âĒ Using EBIT, does not capture net operating cash flow âĒ Uses book value (depreciated value) of capital investments âĒ If capital assets are depreciated, they appear to create a cash flow âĒ Depreciation is an accounting expense not a cash flow âĒ Artificially biases long-term asset-intensive projects, as they have bigger apparent depreciation cash flows âĒ Does not capture the time value of money; interest and inflation ROFE is not a tool to evaluate capital projects. Even used as a metric to compare capital earnings performance, it has flaws. Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 5

- 6. Problem Statement - How we should deal withâĶ âĒ Test-market expenses âĒ Erosion of Jell-O contribution margin âĒ Allocation of charges for the use of excess agglomerator capacity âĒ Overhead expenses Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 6

- 7. Test-market expenses âĒ Should only be taken into account if they can be attributed to the particular project âĒ In the Super case these expenses had been made before the Super project had started ï Will not be taken into account in the FCF Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 7

- 8. Erosion of Jell-O contribution margin âĒ Super will displace part of Jell-OÂīs market share ï Erosion of Jell-O contribution margin should be taken into account Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 8

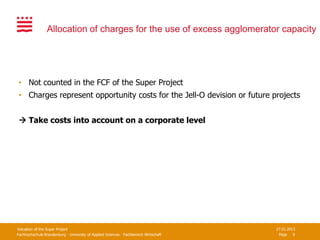

- 9. Allocation of charges for the use of excess agglomerator capacity âĒ Not counted in the FCF of the Super Project âĒ Charges represent opportunity costs for the Jell-O devision or future projects ï Take costs into account on a corporate level Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 9

- 10. Erosion of Jell-O contribution margin âĒ Should be taken into account if they can be attributed to the particular project ï General Foods Corp. already counted theses costs in the CF of Jell-O Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 10

- 11. Overhead Expenses âĒ Should be taken into account if these expenses can be attributed to Super âĒ Overhead expenses for the Super Project are not clearly defined ï Overhead expenses will be taken into account in the FCF Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 11

- 12. Incremental Basis âĒ This evaluation approach uses only directly identified cash flows ï Only incremental approaches has been taken into account ï Jell-O facilities and production capacity are not relevant for Super because they have already been counted in the CF. This execution of Incremental Basis is flawed because it: âĒ Includes sunk costs (the marketing study) âĒ Fails to account for relevant increasing overhead costs. âĒ Fails to take into account income-tax-reducing depreciation. âĒ Utilizes ROFE. Again, ROFE is no good for capital budgeting Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 12

- 13. Facilities-Used Basis âĒ Super will use 1/2 of Jell-Oâs agglomerator âĒ Super will use 2/3 of Jell-Oâs building âĒ Super âpro-rataâ share is $453 K âĒ Charges Super with the facility overhead ($28k p/y). ï This approach âĒ In the capital budgeting process only incremental cash flows are taken into account. âĒ Only shifts costs ($453K in facilities) to Super, which is an accounting maneuver and does not effect the cashflow âĒ Itâs a ânet zeroâ method, it just moves costs ï Useful for accounting, not for capital budgeting Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 13

- 14. Fully Allocated Basis Facilities-Used Basis + overhead expenses âĒ Overhead expenses: âĒ Selling, general and administrative costs ï This approach âĒ Gives the most inclusive analysis of existing cash flow âĒ Adds overhead costs correctly Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 14

- 15. Evaluation of the Super Project GF can do this by: 1. Taking into account incremental cash flows 2. Modifying their income statement to deduct depreciation before calculating tax 3. Ignore sunk costs (marketing test, Jell-O facilities, etc.) 4. Remove depreciation from capital assets for purposes of evaluation 5. Accept overhead from growth/doubling powdered dessert line Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 15

- 16. Recommendations evaluation of the Super Project âĒ $200k for high speed filling/packaging equipment, finish packing room âĒ $360k market test â irrelevant âĒ Opportunity cost for Jell-Oâs facilities and equipment âĒ Not relevant â same opportunity for any project using this building âĒ From corporate POV, hard to sell to move in some business to utilize temporarily excess Jell-O facilities, low feasibility âĒ Capital depreciation â non-cash expense â irrelevant âĒ Capital depreciation expense tax deduction â relevant to operating cash flow âĒ Shift $453k pro-rata share of Jell-O facilities and agglomerator â Incremental test â irrelevant Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 16

- 17. Recommendations Evaluation of the Super Project âĒ $28k avg. yearly depreciation of Jell-O facilities â Incremental test â irrelevant âĒ $19k business expansion capital for distribution system â Incremental test â relevant âĒ Expansion capital depreciation expense tax deduction â relevant to operating cash flow âĒ $90k additional yearly overhead expense for business expansion â Incremental test â relevant Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 17

- 18. Free Cash Flow 400.00 200.00 0.00 Amount -200.00 -400.00 -600.00 -800.00 1 2 3 4 5 6 7 8 9 10 11 FCF Incremental -200 -518 -5.4 5.17 86.1 246. 221. 233. 245. 263. 303. FCF Facility used -453 -518 6.42 16.3 96.7 256. 229. 241. 253. 269. 345. FCF Fully Allocated -672 -518 6.42 16.3 96.7 212. 186. 198. 210. 226. 333. Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 18

- 19. Free Cash Flow Net Sales Net Earnings Discount rate 4,66% 7,69% NPV 447,59 248,64 IRR 13% 13% Net Sales Net Earnings Discount rate 4,66% 7,69% NPV 280,38 67,31 IRR 9% 9% Net Sales Net Earnings Discount rate 4,66% 7,69% NPV -102,79 -286,13 IRR 3% 3% Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 19

- 20. Conclusion - An expansion or broadening of market capture by appealing to somewhat parallel consumer needs - Take advantage of short term availability of Jell-O facilities - in the long term it is not a better project just because it fits a facility that is temporarily unused Main Points: - NPV is in 2 approaches positive - IRR is in 2 approaches higher than discount rate (decision premise) - Payback after the 6th year (shorter than normal payback period) ï Do the investment Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 20

- 21. Fachbereich Wirtschaft Thank you for your attention

- 22. Appendix â Incremental CF Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 22

- 23. Appendix â Facility Used CF Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 23

- 24. Appendix â Fully Allocated CF Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 24

- 25. Appendix â Excel File Excel File Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 25

- 26. Appendix - Depreciation Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 26

- 27. Appendix â Opportunity costs Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 27

- 28. Appendix â Erosion of Jell-O Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 28

- 29. Appendix â Tax rate Valuation of the Super Project 27.01.2013 Fachhochschule Brandenburg · University of Applied Sciences · Fachbereich Wirtschaft Page 29