2012 protecting your business

Download as PPTX, PDF1 like201 views

This document discusses protecting businesses from fraud through various prevention methods. It notes that the typical organization loses 5% of its revenues to fraud each year, totaling over $3.5 trillion globally. Occupational fraud cases have a median loss of $140,000, with 1/5 causing over $1 million in losses. Red flags for potential perpetrators include living beyond means, financial difficulties, and behavioral issues. The document recommends physical controls like background checks, access restrictions, audits and monitoring to prevent fraud, as well as cultivating an ethical corporate culture.

More Related Content

What's hot (20)

Similar to 2012 protecting your business (20)

2012 protecting your business

- 1. Protecting Your Business: WhoŌĆÖs Profit is it Anyway? Fraud Prevention for Business Owners ŌĆ£Providing businesses the prescription for enhanced profitŌĆØ

- 2. Alan Greggo CPP, CFE ŌĆó Consultant ŌĆó Author ŌĆó Senior Loss Prevention Leadership

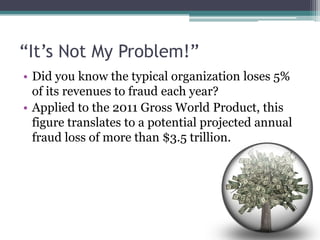

- 4. ŌĆ£ItŌĆÖs Not My Problem!ŌĆØ ŌĆó Did you know the typical organization loses 5% of its revenues to fraud each year? ŌĆó Applied to the 2011 Gross World Product, this figure translates to a potential projected annual fraud loss of more than $3.5 trillion.

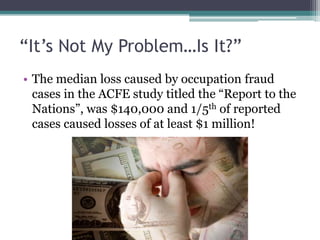

- 5. ŌĆ£ItŌĆÖs Not My ProblemŌĆ”Is It?ŌĆØ ŌĆó The median loss caused by occupation fraud cases in the ACFE study titled the ŌĆ£Report to the NationsŌĆØ, was $140,000 and 1/5th of reported cases caused losses of at least $1 million!

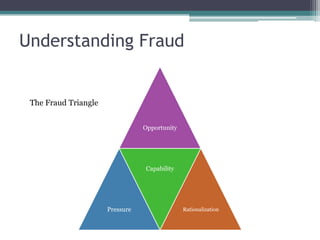

- 6. Understanding Fraud The Fraud Triangle Opportunity Capability Pressure Rationalization

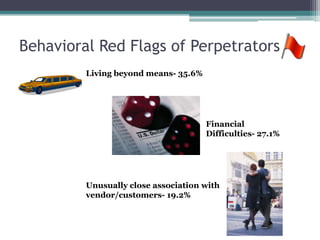

- 7. Behavioral Red Flags of Perpetrators Living beyond means- 35.6% Financial Difficulties- 27.1% Unusually close association with vendor/customers- 19.2%

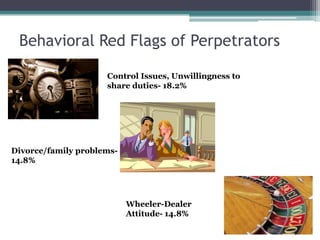

- 8. Behavioral Red Flags of Perpetrators Control Issues, Unwillingness to share duties- 18.2% Divorce/family problems- 14.8% Wheeler-Dealer Attitude- 14.8%

- 9. Behavioral Red Flags of Perpetrators Irritability, suspiciousness or defensiveness- 12.6% Addiction problems- 8.4% Past Employment- related problems- 8.1%

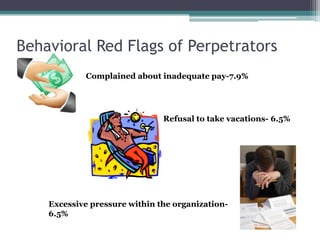

- 10. Behavioral Red Flags of Perpetrators Complained about inadequate pay-7.9% Refusal to take vacations- 6.5% Excessive pressure within the organization- 6.5%

- 11. Oh-My!! IŌĆÖve seen these! ŌĆó Red flags by themselves donŌĆÖt mean an employee is making a bad choice about your business. ŌĆó When you start to see patterns forming or multiple red flags, ensure your fraud controls are being adhered to and watch for unusual behavior. ŌĆó DonŌĆÖt confront an employee head on without evidence of wrong doing; get help from an expert investigator.

- 12. Most employees want to do well ŌĆó Be aware of Goal Incongruence ŌĆó Which is: Management setting lofty targets and goals and expect the employee to achieve them at all cost. The employee feels their future, their job is on the line. ŌĆó Employees want to succeed and please their manager and the company. ŌĆó If the outcome looks hopeless, the employee starts to rationalize (see fraud triangle).

- 13. CFE/ Investigator Wisdom: For FREE ŌĆó People only comply with rules they think are fair!

- 14. CFE/ Investigator Wisdom: For FREE ŌĆó Trust is not and internal control! The indictment seeks $53 million and numerous assets, many of which were seized from Crundwell when she was arrested by FBI agents on April 17. Here's a laundry list of what the government wants: Two residences and the horse farm in Dixon A home in Englewood, Fla. A $2.1 million luxury motor home More than a dozen trucks, trailers and other motorized farm vehicles A 2005 Ford Thunderbird convertible A 1967 Chevrolet Corvette roadster A pontoon boat Approximately $224,898 in cash from two bank accounts

- 15. CFE/ Investigator Wisdom: For FREE ŌĆó Anytime you change a system, people will always change their behavior; WhatŌĆÖs possible? ŌĆó If you want people to do the right thing you have to make it personal.

- 16. Protecting Your Business- Physical Controls ŌĆó Pre-employment background checks ŌĆó Policies on dishonest and unethical behavior ŌĆó Supported from top management? ŌĆó Business Abuse Hotline; anonymous way to report suspected violations of the ethics and anti-fraud policies ŌĆó Restricted access to areas containing sensitive documents ŌĆó Maintain a system for providing an audit trail

- 17. Protecting Your Business-Physical Controls ŌĆó Restricted access to computer systems (accounting software, inventory, and payroll) ŌĆó Restrict access to areas with high value assets (shipping, receiving, storerooms, and cash) ŌĆó CCTV and recording equipment to monitor physical building and sensitive areas

- 18. Protecting Your Business-Physical Controls ŌĆó Conduct random, unannounced audits of inventory, cash, expense, purchasing, billing, etc. by internal or external auditors ŌĆó Prompt investigations of reported incidents of fraud ŌĆó Educate employees about the importance of ethics and anti-fraud programs

- 19. Active social networkers ŌĆó As a group, more likely to experience pressure to compromise ethics by 32%. ŌĆó 56% of social networkers experience retaliation versus only 18% of less active or nonŌĆÉactive networkers.

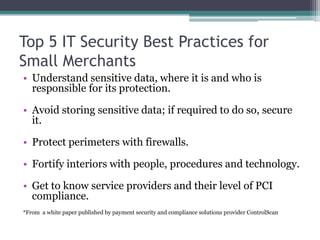

- 20. Top 5 IT Security Best Practices for Small Merchants ŌĆó Understand sensitive data, where it is and who is responsible for its protection. ŌĆó Avoid storing sensitive data; if required to do so, secure it. ŌĆó Protect perimeters with firewalls. ŌĆó Fortify interiors with people, procedures and technology. ŌĆó Get to know service providers and their level of PCI compliance. *From a white paper published by payment security and compliance solutions provider ControlScan

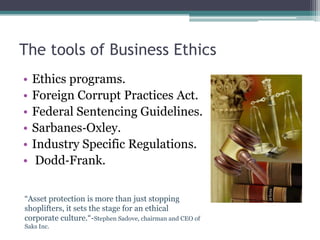

- 21. The tools of Business Ethics ŌĆó Ethics programs. ŌĆó Foreign Corrupt Practices Act. ŌĆó Federal Sentencing Guidelines. ŌĆó SarbanesŌĆÉOxley. ŌĆó Industry Specific Regulations. ŌĆó DoddŌĆÉFrank. ŌĆ£Asset protection is more than just stopping shoplifters, it sets the stage for an ethical corporate culture.ŌĆ£-Stephen Sadove, chairman and CEO of Saks Inc.

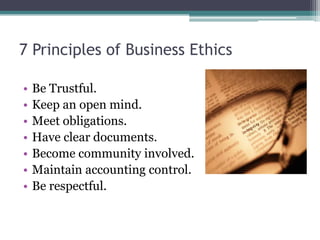

- 22. 7 Principles of Business Ethics ŌĆó Be Trustful. ŌĆó Keep an open mind. ŌĆó Meet obligations. ŌĆó Have clear documents. ŌĆó Become community involved. ŌĆó Maintain accounting control. ŌĆó Be respectful.

- 23. Questions? Alan Greggo Easy Risk Assessment- 11 questions to consider about your business: http://profitrxllc.com/pages/RiskAssessment Phone: (513) 236-2642

Editor's Notes

- #17: Do you conduct pre-employment background checks?Are there policies that address dishonest and unethical behavior?Are they supported by top management?Does the organization provide an anonymous way to report suspected violations of the ethics and anti-fraud policies?Does the organization restrict access to areas containing sensitive documents (such as invoices, receipts, journals, ledgers, and checks) and maintain a system for providing an audit trail of access?