Essentials Of Internal Control

•

3 likes•1,471 views

Material used by my mentor/friend - Cheung Hon Wan in 2005 Internal Control Forum in Shanghai. I am glad for preparing this ppt for his speech

Essentials Of Internal Control

- 1. Essentials of Internal Control Speaker: Cheung Hon Wan Edited by : Dick Lam

- 2. What financial reports tell summary of past performance how much a company have for evaluation of past for future decision

- 3. Do the reports right? SURE Management Auditor

- 4. Do the reports tell the truth? 1998 World Cup final France beat Brazil 3:0 ?

- 5. Working toward company objectives

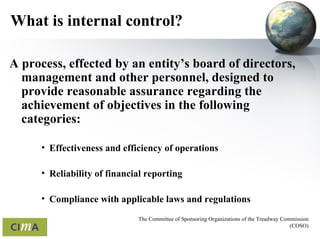

- 6. What is internal control? A process, effected by an entity’s board of directors, management and other personnel, designed to provide reasonable assurance regarding the achievement of objectives in the following categories: Effectiveness and efficiency of operations Reliability of financial reporting Compliance with applicable laws and regulations The Committee of Sponsoring Organizations of the Treadway Commission (COSO)

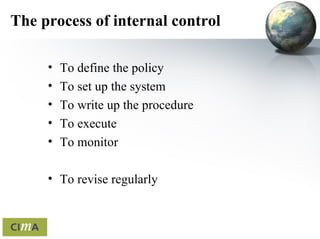

- 7. The process of internal control To define the policy To set up the system To write up the procedure To execute To monitor To revise regularly

- 8. Internal Control – Comment Policy & procedures not enforceable, you do not understand operations Policy is not realistic, procedures just create paper work Wasting precious working time, lowering operation efficiency Requires more staff headcount Environment is ever-changing Internal control only addresses annually & SOX focuses on published account but does not help business operation

- 9. The job only for finance or internal audit Too many NATO during the preparation Blames on internal control as fraud still exists Complaint on blocking the efficiency as the company is running healthy Keep on giving chances to incapable staff Internal Control – Observation Lazy Expression of authority Personal interest

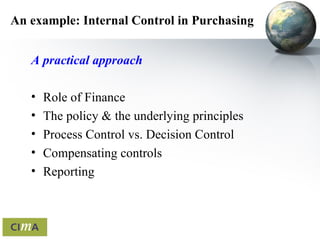

- 10. An example: Internal Control in Purchasing A practical approach Role of Finance The policy & the underlying principles Process Control vs. Decision Control Compensating controls Reporting

- 11. Role of Finance Advantages: Relatively high degree of integrity Conservative & high sensitivity to risk Sensitivity to data Design the policy and set the objectives Review the procedure from Supply Chain Participation in operation Transaction approval

- 12. Structure of a policy Principles Responsible Dept Owner/Monitor Shall do Shall not do Objectives Procedures Internal Audit

- 13. Underlying principles Group Decision High degree of transparency No hiding of information Separation of duties Audit trail of decision making

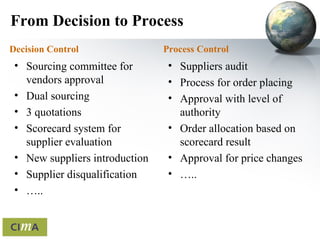

- 14. Decision Control Suppliers audit Process for order placing Approval with level of authority Order allocation based on scorecard result Approval for price changes … .. Sourcing committee for vendors approval Dual sourcing 3 quotations Scorecard system for supplier evaluation New suppliers introduction Supplier disqualification … .. Process Control From Decision to Process

- 15. Reporting Key Risk Indicators Purchasing value & % of single source No. of items with single source Price change effects Reporting of concessionary activities Audit of open book costing Progress of corrective action plan

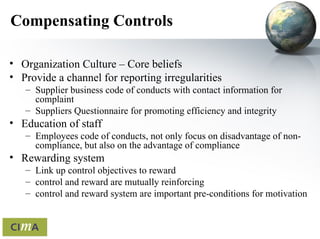

- 16. Compensating Controls Organization Culture – Core beliefs Provide a channel for reporting irregularities Supplier business code of conducts with contact information for complaint Suppliers Questionnaire for promoting efficiency and integrity Education of staff Employees code of conducts, not only focus on disadvantage of non-compliance, but also on the advantage of compliance Rewarding system Link up control objectives to reward control and reward are mutually reinforcing control and reward system are important pre-conditions for motivation

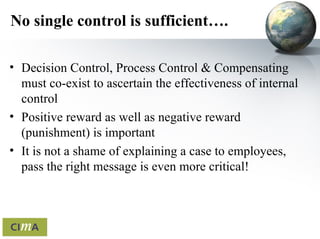

- 17. No single control is sufficient…. Decision Control, Process Control & Compensating must co-exist to ascertain the effectiveness of internal control Positive reward as well as negative reward (punishment) is important It is not a shame of explaining a case to employees, pass the right message is even more critical!

- 18. Be pragmatic….. T I C

- 19. No system is perfect !! The arts of recognizing weaknesses…. As we know we are weak, we get the room to become strong As we know we are imperfect, we get the will to become perfect Continuous review of internal control system is mandatory !!