A cash conversion cycle approach to liquidity analysis final

ŌĆóDownload as PPTX, PDFŌĆó

2 likesŌĆó1,949 views

This document discusses different approaches to liquidity analysis, including traditional static ratios like current and acid-test ratios as well as more dynamic approaches like the cash conversion cycle. It finds that static ratios only provide a limited snapshot of liquidity and fail to account for cash flows over time. In contrast, the cash conversion cycle considers how long it takes for a company to convert resources into cash and can better indicate whether high receivables and inventory are positively or negatively impacting liquidity. The cash conversion cycle thus provides a more comprehensive view of a company's liquidity position and management implications.

A cash conversion cycle approach to liquidity analysis final

- 1. A Cash Conversion Cycle Approach To Liquidity Analysis Group D Akriti Bajracharya Ayusha Bajracharya Bimash Sharma Nancy Shrestha Nischal Gautam Umesh Maharjan

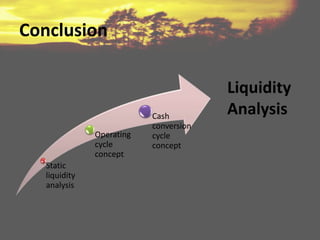

- 2. Outline of the presentation 1.Brief introduction 2.Objective of the article 3.Methodology used 4.Findings of the article 5.Conclusion

- 3. Introduction ŌĆó Verlyn D Richards (Professor of Finance) and Eugene J. Laughlin (Professor of Accounting).

- 4. Objective ŌĆó Focus on the different approaches, such as traditional approach and the operating cycle concept for the liquidity analysis of the firm, as well as their drawbacks ŌĆó Comparison between traditional balance sheet ratios and comprehensive approach to analysis ŌĆó To clear out the misinterpretation made by the static liquidity analysis

- 6. Findings ŌĆó Current ratio and acid-test ratio Static Liquidity Analysis

- 7. ŌĆó Current Ratio ŌĆó Ignores the qualitative differences in liquidity attributes of current assets. ŌĆó Responded to the problem by introduction of more restrictive acid test ratio. ŌĆó Both static liquidity indicators is limited by their failure to provide adequate information about cash flow attributes of the transformation process within a firmŌĆÖs working capital position. ŌĆó Emphasize essentially liquidation, rather than a going concern approach to liquidity analysis. Misinterpretation of liquidity position Current ratio Acid ŌĆōtest ratio

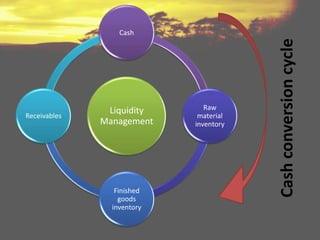

- 9. ŌĆó High receivable & longer collection period longer operating cycle deteriorating liquidity. ŌĆó High receivable high current and acid-test ratio improving liquidity. ŌĆó Similar in case of inventory. ŌĆó Drawback do not consider the liquidity requirement imposed by current liabilities. Incorrect analysis of liquidity position

- 11. ŌĆó Different from operating cycle concept ’ā╝Considers cash outflow requirement in an analysis ŌĆó Cash conversion cycle interpretation of liquidity position ’ā╝ Impact of longer operating cycle ’ā╝ Impact of longer payable deferral period ŌĆó Interpretation opposite to static liquidity analysis.

- 12. Financial management implication ŌĆó Spontaneous and non-spontaneous financing Spontaneous Non-spontaneous Working Capital Investment The need for cash conversion cycle approach

- 13. ŌĆó Length of cash conversion cycle has impact on ’ā╝ Financial structure ’ā╝ Investment structure Length of cash conversion cycle Borrowing capacity In case of economic uncertainty

- 15. THANK YOU

- 16. Any Questions ??