Accounting entries under gst

Download as DOCX, PDF1 like715 views

Under GST, businesses will need to maintain fewer accounts than currently required for taxes like VAT, excise and service tax. Accounts will need to track input and output central GST, state GST and integrated GST. Accounting entries will involve debiting input tax accounts and crediting output tax accounts, with the difference credited or debited to an electronic cash ledger for payment or refund. This will simplify record keeping while allowing input taxes on more purchases to be set off against output tax liabilities. The changes will streamline tax compliance and potentially reduce operating costs and tax outflows for businesses.

![How to pass accounting entries under GST

Updated on Jun 09, 2017 - 08:41:39 PM

Goods and service tax or GST will be one tax to subsume all taxes. It will bring in ŌĆ£One

nation one taxŌĆØ regime.

While there will be certain initial transition challenges, GST will bring in much clarity in

many areas of business. One of the areas is accounting and bookkeeping. Read on to

find out about accounting entries under GST.

Current scenario:

Separate accounts have to be maintained for excise, VAT, CST and service tax. HereŌĆÖs

a list of the few accounts currently any business has to maintain (apart from accounts

like purchase, sales, stock) ŌĆō

’éĘ Excise payable a/c (for manufacturers)

’éĘ CENVAT credit a/c (for manufacturers)

’éĘ Output VAT a/c

’éĘ Input VAT a/c

’éĘ Input Service tax a/c

’éĘ Output Service tax a/c

For example, a trader Mr. X must maintain the minimum basic accounts ŌĆō

’éĘ Output VAT a/c

’éĘ Input VAT a/c

’éĘ CST A/c (for inter-state sales and purchases)

’éĘ Service tax a/c [He will not be able to claim any service tax input credit as he is a

trader with output VAT. Service tax cannot be setoff against VAT/ CST]

GST Regime

Under GST all these taxes (excise, VAT, service tax) will get subsumed into one

account.

The same trader X has to then maintain the following a/cs (apart from accounts like

purchase, sales, stock) ŌĆō

’éĘ Input CGST a/c

’éĘ Output CGST a/c

’éĘ Input SGST a/c

’éĘ Output SGST a/c

’éĘ Input IGST a/c

’éĘ Output IGST a/c

’éĘ Electronic Cash Ledger (to be maintained on Government GST portal to pay

GST)](https://image.slidesharecdn.com/accountingentriesundergst-180317072319/85/Accounting-entries-under-gst-1-320.jpg)

![Output CGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 2,640

Output SGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 10,640

To Electronic Cash Ledger A/c 13,280

GST impact on financials

Profit & Loss Account

Particulars Rs. Particulars Rs.

Raw material consumption XXX [Decrease] Sales XXX***

Purchases XXX

Depreciation XXX

Other Expenses XXX

Reduction in raw material cost and other expenses

GST will mean seamless input credits for intrastate and interstate purchases of goods.

This will mean reduction in cost of raw materials as input GST can be setoff against the

output GST payable on sales. Also GST paid on many services like legal consultation,

audit fees, engineering consultation etc. can be setoff against output GST. Currently

input credit of service tax paid cannot be adjusted against output excise/VAT.

All this will effectively bring down the expenses.

***Impact on sales may vary depending on the industry and the GST rates.

Balance Sheet

Particulars Rs. Particulars Rs.](https://image.slidesharecdn.com/accountingentriesundergst-180317072319/85/Accounting-entries-under-gst-7-320.jpg)

![Capital XXX Fixed assets XXX [Decrease]

Current liabilities XXX Current assets XXX

Tax payable XXX Credit receivable XXX

Effective cost of fixed assets will come down as input credit will be available on both

capital goods and services related to such goods like installation, inspection etc.

Tax payable and credit receivable will face changes too. There will be only three

accounts under each of them- SGST, CGST, IGST instead of maintaining current excise

payable, CENVAT credit, VAT payable, VAT credit, Service tax accounts.

Accounting principles

GAAP is applicable mandatorily on GST. So, all principles following revenue recognition

etc. will be applicable.

Period of retention of accounts

Every registered taxable person must keep and maintain books of account for five years

from the due date of filing of Annual Return for the relevant year.

Transition to GST will need to address various aspects of financial reporting systems for

proper reporting.

It is important that businesses plan to address changes arising out GST implementation

in the best manner to reduce cost of transition and minimize business disruption.](https://image.slidesharecdn.com/accountingentriesundergst-180317072319/85/Accounting-entries-under-gst-8-320.jpg)

More Related Content

What's hot (20)

Similar to Accounting entries under gst (20)

Recently uploaded (20)

Accounting entries under gst

- 1. How to pass accounting entries under GST Updated on Jun 09, 2017 - 08:41:39 PM Goods and service tax or GST will be one tax to subsume all taxes. It will bring in ŌĆ£One nation one taxŌĆØ regime. While there will be certain initial transition challenges, GST will bring in much clarity in many areas of business. One of the areas is accounting and bookkeeping. Read on to find out about accounting entries under GST. Current scenario: Separate accounts have to be maintained for excise, VAT, CST and service tax. HereŌĆÖs a list of the few accounts currently any business has to maintain (apart from accounts like purchase, sales, stock) ŌĆō ’éĘ Excise payable a/c (for manufacturers) ’éĘ CENVAT credit a/c (for manufacturers) ’éĘ Output VAT a/c ’éĘ Input VAT a/c ’éĘ Input Service tax a/c ’éĘ Output Service tax a/c For example, a trader Mr. X must maintain the minimum basic accounts ŌĆō ’éĘ Output VAT a/c ’éĘ Input VAT a/c ’éĘ CST A/c (for inter-state sales and purchases) ’éĘ Service tax a/c [He will not be able to claim any service tax input credit as he is a trader with output VAT. Service tax cannot be setoff against VAT/ CST] GST Regime Under GST all these taxes (excise, VAT, service tax) will get subsumed into one account. The same trader X has to then maintain the following a/cs (apart from accounts like purchase, sales, stock) ŌĆō ’éĘ Input CGST a/c ’éĘ Output CGST a/c ’éĘ Input SGST a/c ’éĘ Output SGST a/c ’éĘ Input IGST a/c ’éĘ Output IGST a/c ’éĘ Electronic Cash Ledger (to be maintained on Government GST portal to pay GST)

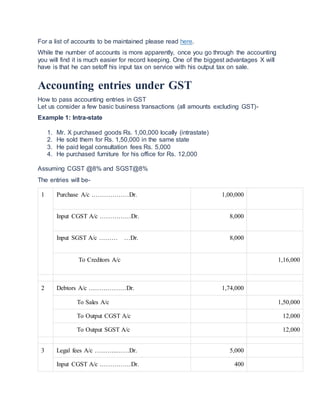

- 2. For a list of accounts to be maintained please read here. While the number of accounts is more apparently, once you go through the accounting you will find it is much easier for record keeping. One of the biggest advantages X will have is that he can setoff his input tax on service with his output tax on sale. Accounting entries under GST How to pass accounting entries in GST Let us consider a few basic business transactions (all amounts excluding GST)- Example 1: Intra-state 1. Mr. X purchased goods Rs. 1,00,000 locally (intrastate) 2. He sold them for Rs. 1,50,000 in the same state 3. He paid legal consultation fees Rs. 5,000 4. He purchased furniture for his office for Rs. 12,000 Assuming CGST @8% and SGST@8% The entries will be- 1 Purchase A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 1,00,000 Input CGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 8,000 Input SGST A/c ŌĆ”ŌĆ”ŌĆ” ŌĆ”Dr. 8,000 To Creditors A/c 1,16,000 2 Debtors A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 1,74,000 To Sales A/c 1,50,000 To Output CGST A/c 12,000 To Output SGST A/c 12,000 3 Legal fees A/c ŌĆ”ŌĆ”ŌĆ”..ŌĆ”ŌĆ”Dr. 5,000 Input CGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 400

- 3. Input SGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 400 To Bank A/c 5,800 4 Furniture A/c ŌĆ”ŌĆ”ŌĆ”..ŌĆ”ŌĆ”Dr. 12,000 Input CGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 960 Input SGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 960 To ABC Furniture Shop A/c 13,920 Have you filed your GSTR-1 yet? File GSTR-1 Now! File now under 15 minutes through ClearTax GST Total Input CGST=8,000+400+960= Rs. 9,360 Total Input SGST=8,000+400+960= Rs. 9,360 Total output CGST=12,000 Total output SGST=12,000 Therefore Net CGST payable=12,000-9,360=2,640 Net SGST payable=12,000-9,360=2,640 5 Output CGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 12,000 Output SGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 12,000 To Input CGST A/c 9,360 To Input SGST A/c 9,360 To Electronic Cash Ledger A/c 5,280 Thus due to input tax credit, tax liability of Rs. 24,000 is reduced to only Rs.5,280. Also, GST on legal fees is also adjusted which was not possible in current tax regime. If there had been any input tax credit left it would have been carried forward to the next year.

- 4. Example 2: Inter-state 1. Mr. X purchased goods Rs. 1,50,000 from outside the State 2. He sold Rs. 1,50,000 locally 3. He sold Rs.1,00,000 outside the state 4. He paid telephone bill Rs. 5,000 5. He purchased an air cooler for his office for Rs. 12,000 (locally) Assuming CGST @8% and SGST@8% 1 Purchase A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 1,50,000 Input IGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 24,000 To Creditors A/c 1,74,000 2 Debtors A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 1,74,000 To Sales A/c 1,50,000 To Output CGST A/c 12,000 To Output SGST A/c 12,000 3 Debtors A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 1,16,000 To Sales A/c 1,00,000 To Output IGST A/c 16,000 4 Telephone Expenses A/c ..ŌĆ”Dr. 5,000

- 5. Input CGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”..Dr. 400 Input SGST A/c ŌĆ”..ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 400 To Bank A/c 5,800 5 Office Equipment A/c.ŌĆ”..Dr. 12,000 Input CGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 960 Input SGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 960 To ABC Furniture Shop A/c 13,920 Total CGST input =400+960=1,360 Total CGST output =12,000 Total SGST input =400+960=1,360 Total SGST output =12,000 Total IGST input =24,000 Total IGST output =16,000 Particulars CGST SGST IGST Output liability 12,000 12,000 16,000 Less: Input tax credit CGST 1,360 SGST 1,360 IGST 8,000 16,000

- 6. Amount payable 2,640 10,640 NIL Any IGST credit will first be applied to set off IGST and then CGST. Balance if any will be applied to setoff SGST. So out of total input IGST of Rs. 24,000, firstly it will be completely setoff against IGST. Then balance Rs.8,000 against CGST. From the total Rs.40,000, only Rs. 13,280 is payable. So the setoff entries will be- Setoff against CGST output 1 Output CGST ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 9,360 To Input CGST A/c 1,360 To Input IGST A/c 8,000 2 Setoff against SGST output Output SGST ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 1,360 To Input SGST A/c 1,360 3 Setoff against IGST output Output IGST ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 16,000 To Input IGST A/c 16,000 4 Final payment

- 7. Output CGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 2,640 Output SGST A/c ŌĆ”ŌĆ”ŌĆ”ŌĆ”ŌĆ”Dr. 10,640 To Electronic Cash Ledger A/c 13,280 GST impact on financials Profit & Loss Account Particulars Rs. Particulars Rs. Raw material consumption XXX [Decrease] Sales XXX*** Purchases XXX Depreciation XXX Other Expenses XXX Reduction in raw material cost and other expenses GST will mean seamless input credits for intrastate and interstate purchases of goods. This will mean reduction in cost of raw materials as input GST can be setoff against the output GST payable on sales. Also GST paid on many services like legal consultation, audit fees, engineering consultation etc. can be setoff against output GST. Currently input credit of service tax paid cannot be adjusted against output excise/VAT. All this will effectively bring down the expenses. ***Impact on sales may vary depending on the industry and the GST rates. Balance Sheet Particulars Rs. Particulars Rs.

- 8. Capital XXX Fixed assets XXX [Decrease] Current liabilities XXX Current assets XXX Tax payable XXX Credit receivable XXX Effective cost of fixed assets will come down as input credit will be available on both capital goods and services related to such goods like installation, inspection etc. Tax payable and credit receivable will face changes too. There will be only three accounts under each of them- SGST, CGST, IGST instead of maintaining current excise payable, CENVAT credit, VAT payable, VAT credit, Service tax accounts. Accounting principles GAAP is applicable mandatorily on GST. So, all principles following revenue recognition etc. will be applicable. Period of retention of accounts Every registered taxable person must keep and maintain books of account for five years from the due date of filing of Annual Return for the relevant year. Transition to GST will need to address various aspects of financial reporting systems for proper reporting. It is important that businesses plan to address changes arising out GST implementation in the best manner to reduce cost of transition and minimize business disruption.