Asset Based=Collateral Based Lending

?Download as PPT, PDF?

1 like?1,591 views

This document compares and contrasts asset-based lending and factoring. It discusses the key differences in collateral considerations, advance rates, fees, requirements, and qualifications for each type of lending. Specifically, it notes that asset-based lending considers inventory, equipment, and other assets as collateral in addition to accounts receivable, while factoring only considers accounts receivable. It also provides details on qualification requirements, reporting needs, and areas of concern for lenders.

Asset Based=Collateral Based Lending

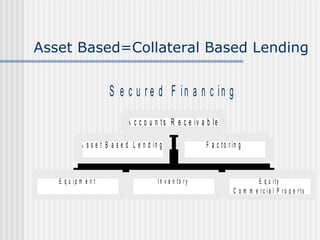

- 1. Asset Based=Collateral Based Lending

- 2. Accounts Receivable Financing ABL ¨Cvs.- Factoring Asset Based Lending Borrowing Certificate Adv Rate 70%-90% Prime + 3 & Up Inventory Considered Equipment Considered Lock Box Required Secondary Collateral Required Factoring Accounts Receivable Only Adv Rate 70-90% 2-5% Discount on Total invoiced amount Notification/Verification Original Invoices stamped by the lender Lock Box Required

- 3. Equipment Asset Based Lenders 50-60% Liquidated Value Manufacturing Fabricating Transportation Yellow Iron No Small Tooling Factors None

- 4. Inventory Asset Based Lenders 40-50% Finished Good Raw Materials Depends on the material Disallowed Outdated Materials WIP Factors None

- 5. Commercial Property Equity Asset Based Lenders Secondary Collateral 3 Million & Up ABL Transactions often include some term financing on property. Factors Secondary Collateral

- 6. How Big is Our Lending Box? Asset Based Lenders Prior Losses Current Losses Quick Ratio 1:1 or Worse Negative Net Worth Factors Prior Losses Current Losses Quick Ratio 1:1 or Worse Negative Net Worth Start-Up Business Delinquent Taxes BankˇŻs Box ABL / Factors Box

- 7. When is it Appropriate? Asset Based Loan Rapid Growth Good Product or service with high leverage Troubled Companies Turn Around Plan Secondary Support Available Factoring Rapid Growth Start-Ups Two-Three Years Old Too Little historical Performance Troubled Companies Turn Around Plan When do you pull the plug? No Secondary Support

- 8. Quick!, ˇ°Who Will Qualify?ˇ± Asset Based Loan Must Have _____? Volume Dependant 250K / Month Minimum No Delinquent Taxes Secondary Collateral Market Share Factoring Must Have _____? Min. 10K Monthly Sales No Maximum Delinquent taxes O.K. with a payment plan No Secondary Support

- 9. Reporting Requirements Asset Based Lines of Credit Borrowing Certificates can be submitted Dailey A/R Aging Summary sent over with Borrowing Cert. Monthly Financials need to be timely Good accounting systems, good job costing Annual Financial Statements-Audited-vs.-Unaudited depends of the lender Collateral Control Account Required Periodic Collateral examines depends on the lender, and collateral used in the formula

- 10. Areas Of Concern Ineligible Accounts Receivable Foreign Receivables Money back Guarantees Contra Accounts Inter-company Invoices 61-90 days, depends on the industry standards Even a factor doesnˇŻt like slow collections Too Many Credit Memos Poor Quality of Product or service Red Flag for Fraud Concentration