More Related Content

Similar to ATm Machine Presentaion of Progaramming Fundamentals (20)

Recently uploaded (20)

ATm Machine Presentaion of Progaramming Fundamentals

- 1. Hanzla 021 Haseeb 015 Anas 030 Talha 009 Uzair 020 Role of ATM machine in modern Banking Programming Fundamentals Lab

- 2. ATM Machines: A Vital Part of Modern Banking An ATM (Automated Teller Machine) is a self-service electronic device that allows users to perform a variety of banking transactions smoothly. It enables account holders to check their balances, withdraw or deposit cash, transfer money between accounts, and perform other banking services securely. ATMs are widely accessible and are designed to provide 24/7 access to banking services, offering convenience and efficiency for managing personal finances.

- 3. History of ATM Technology 1 Early Days The first ATM was introduced in London in 1967. It was developed by Barclays Bank and called the "Automatic Teller Machine." 2 Expansion and Innovation ATMs spread rapidly throughout the world in the 1970s and 1980s. New features such as card reader technology and PINs emerged. 3 Digital Transformation The rise of mobile banking and online payments has led to advancements in ATM technology, with enhanced security and interactive features.

- 4. Key Components of an ATM Card Reader Reads your debit or credit card and verifies your identity. Cash Dispenser Dispensers money from the vault through a secure mechanism. Keyboard and Screen Allows you to interact with the machine to make transactions. Communication Network Connects the ATM to the bank's computer system.

- 5. ATM Security Measures PIN Protection A personal identification number (PIN) protects your account from unauthorized access. Anti-Skimming Devices Skimming is a common method of stealing card information. Devices are deployed to prevent skimming. Surveillance Cameras Cameras deter criminals and aid in investigations if a crime occurs. Encryption Technology Data transmitted between the ATM and the bank is encrypted to protect against interception.

- 6. Transactions Facilitated by ATMs New User Registry New customers register by providing personal details and setting a PIN. Login Users can deposit cash into their account by entering amount to be deposited. Balance Inquiry Displays the current balance of the userŌĆÖs bank account after login. Deposit Users can transfer funds to another account by entering the recipientŌĆÖs account username. Users enter their credentials to access the system. Withdraw Send Money Users can withdraw cash from their account by entering the desired amount. Exit Logs the user out of the session securely

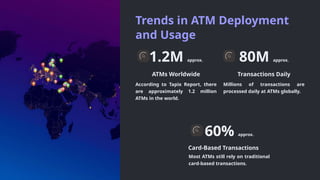

- 7. Trends in ATM Deployment and Usage 1.2M approx. ATMs Worldwide According to Tapix Report, there are approximately 1.2 million ATMs in the world. 80M approx. Transactions Daily Millions of transactions are processed daily at ATMs globally. 60% approx. Card-Based Transactions Most ATMs still rely on traditional card-based transactions.

- 8. Regulatory Landscape for ATMs 1 Consumer Protection Regulations ensure fair and transparent ATM fees. 2 Security Standards Regulations require ATMs to meet security standards to protect user data and money. 3 Accessibility Regulations promote accessibility for people with disabilities.

- 9. Challenges Facing the ATM Industry Rising Operational Costs Maintaining and securing ATMs is becoming increasingly expensive. Declining ATM Usage The rise of mobile and online banking is decreasing the reliance on ATMs. Fraud and Security Threats The ATM industry is constantly battling against new forms of fraud and security threats.

- 10. Conclusion ATM machines have revolutionized banking, offering a wide range of essential functions for convenient and secure financial transactions. Their user-friendly interface and advanced security measures make them indispensable tools for managing personal finances.