Audit planning

- 1. Planning ISA 300

- 2. Planning SUMMARY Preliminary Audit Audit Review Activities Strategy Plan

- 3. Planning Wider aspects When How Much Preliminaries Depends on: On Completing Last Audit (control de?ciencies / 1) Size and complexity of Evaluating compliance with unadjusted errors) client relevant ethical requirements, including independence. As Audit Progresses - 2) Previous experience with the signi?cant event changing the client, and Establishing an understanding plan of the terms of the 3) Any changes in engagement. circumstance that may occur during the audit.

- 4. Planning Wider aspects When How Much Preliminaries Depends on: On Completing Last Audit (control de?ciencies / 1) Size and complexity of Evaluating compliance with unadjusted errors) client relevant ethical requirements, including independence. As Audit Progresses - 2) Previous experience with the signi?cant event changing the client, and Establishing an understanding plan of the terms of the 3) Any changes in engagement. circumstance that may occur during the audit.

- 5. Planning Wider aspects When How Much Preliminaries Depends on: On Completing Last Audit (control de?ciencies / 1) Size and complexity of Evaluating compliance with unadjusted errors) client relevant ethical requirements, including independence. As Audit Progresses - 2) Previous experience with the signi?cant event changing the client, and Establishing an understanding plan of the terms of the 3) Any changes in engagement. circumstance that may occur during the audit.

- 6. Planning Wider aspects When How Much Preliminaries Depends on: On Completing Last Audit (control de?ciencies / 1) Size and complexity of Evaluating compliance with unadjusted errors) client relevant ethical requirements, including independence. As Audit Progresses - 2) Previous experience with the signi?cant event changing the client, and Establishing an understanding plan of the terms of the 3) Any changes in engagement. circumstance that may occur during the audit.

- 9. Audit Strategy Logistics Managing Resources Planning Results Of the audit

- 10. Audit Strategy Logistics Scope Managing Resources of the audit Planning Results Of the audit

- 11. Audit Strategy Logistics Scope Managing Resources of the audit Planning Results Reporting Of the audit Objectives

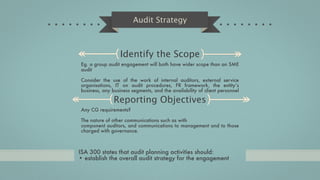

- 12. Audit Strategy Identify the Scope Eg. a group audit engagement will both have wider scope than an SME audit Consider the use of the work of internal auditors, external service organisations, IT on audit procedures, FR framework, the entityˇŻs business, any business segments, and the availability of client personnel Reporting Objectives Any CG requirements? The nature of other communications such as with component auditors, and communications to management and to those charged with governance. ISA 300 states that audit planning activities should: ? establish the overall audit strategy for the engagement

- 13. Audit Strategy Logistics Such as quality control, how resources are managed, directed and supervised, when team brie?ng and debrie?ng meetings are expected to be held, how engagement partner and manager reviews are expected to take place (for example, on-site or off-site), and whether to complete engagement quality control reviews. Planning Results Set initial materiality, any fraud risks, signi?cant events that have occurred since the last audit, and the results of previous audits evaluating internal controls (any de?ciencies and action taken) Any other relevant services, eg reviews of business plans or cash ?ow forecasts. ISA 300 states that audit planning activities should: ? establish the overall audit strategy for the engagement

- 14. Audit Strategy Nature, timing & resources The use of specialists, highly experienced auditors for a potentially high risk audit engagement. If time pressured, then more resources needed ISA 300 states that audit planning activities should: ? establish the overall audit strategy for the engagement

- 15. Planning A detailed programme giving instructions as to how each area of the audit will be conducted

- 16. Planning A detailed programme giving instructions as to how each area of the audit will be conducted 1 Nature, timing and extent of planned risk assessment procedures

- 17. Planning A detailed programme giving instructions as to how each area of the audit will be conducted 1 2 Nature, timing and extent of planned Nature, timing and extent of planned risk assessment procedures further audit procedures at the assertion level

- 18. Planning A detailed programme giving instructions as to how each area of the audit will be conducted 1 2 3 Nature, timing and extent of planned Nature, timing and extent of planned Other planned audit procedures risk assessment procedures further audit procedures at the so that the engagement assertion level complies with ISAs.

- 19. Audit Plan Changes Updated as Necessary Information comes that is different to For example, as a result of unexpected the planned info. events, the auditor may need to modify the planned nature, timing and For example, an event creating doubt extent of further audit procedures, over going concern. based on the revised consideration of assessed risks. Or, amend initial risk assessment / performance materiality, for all, or part, of the audit, after performing planning procedures Audit strategy is not always prepared and completed before the audit plan, in practice it is typical for the two to be developed together

- 20. Documentation

- 21. Documentation Key Decisions 1 So docs are vital

- 22. Documentation Key Decisions 1 Changes Document So docs are vital auditor 2 response

- 23. Documentation Key Decisions 1 Changes Document So docs are vital auditor 2 response Standardised Audit Programmes 3

- 24. Documentation Key Decisions 1 Changes Document So docs are vital auditor 2 response Tailored Standardised Types Audit Programmes 4 3

- 25. Documentation Key Decisions 1 Clear Record Changes all is needed Document So docs are vital auditor 5 2 response Tailored Standardised Types Audit Programmes 4 3

- 27. Direction & Supervision Plan it! The amount of detail included in the audit plan depends on factors such as: How supervision and review should be conducted during the 1) The size and complexity of the entity audit 2) The assessed risk of material misstatement 3) The capabilities of the audit team members. Inadequate supervision and review can lead to errors, eg. selecting inappropriate items for sampling

- 28. For Initial Engagements Client Communicate Engagement with the Procedures predecessor More auditor Planning Needed Planning is a dynamic process that may evolve during the audit, and should always respond to changes in the circumstances of the audited entity

Editor's Notes

- #2: \n

- #3: \n

- #4: \n

- #5: \n

- #6: \n

- #7: \n

- #8: \n

- #9: \n

- #10: \n

- #11: \n

- #12: \n

- #13: \n

- #14: \n

- #15: \n

- #16: \n

- #17: \n

- #18: \n

- #19: \n

- #20: \n

- #21: \n

- #22: \n

- #23: \n

- #24: \n

- #25: \n

- #26: \n

- #27: \n

- #28: \n

- #29: \n

- #30: \n

- #31: \n

- #32: \n

- #33: \n

- #34: \n

- #35: \n

- #36: \n

- #37: \n

- #38: \n

- #39: \n

- #40: \n

- #41: \n

- #42: \n

- #43: \n

- #44: \n

- #45: \n

- #46: \n

- #47: \n

- #48: \n

- #49: \n

- #50: \n

- #51: \n

- #52: \n

- #53: \n

- #54: \n

- #55: \n

- #56: \n

- #57: \n

- #58: \n

- #59: \n

- #60: \n

- #61: \n

- #62: \n

- #63: \n

- #64: \n

- #65: \n