Bacics Of Derivatives

- 1. BASICS OF DERIVATIVES by ERUM

- 2. Risk Goal of risk management : to maximize the value of the firm by reducing the negative potential impact of forces beyond the control of management. four basic approaches to risk management: risk avoidance, risk retention, loss prevention and control, and risk transfer.

- 3. Derivatives- financial instruments whose value depends on/derives from some underlying variable(asset). Used for changing the risk exposure . Hedging When the firm reduces its risk exposure with the use of derivatives, it is said to be hedging.

- 4. Derivatives as a leveraging tool. It’s increased use for speculation. Word of Caution : Barrings Bank, Orange County, P&C, LTCM etc.

- 5. Types of derivatives. Futures Forwards Options Swap

- 6. Forward contract an agreement to buy or sell an asset (of a specified quantity) at a certain future time for a certain price.

- 7. Futures Futures contracts are a variant of the forward contract that take place on financial exchanges.

- 8. Future v/s FORWARD the seller can choose to deliver the commodity on any day during the delivery month futures contracts are traded on an exchange whereas forward contracts are generally traded off an exchange. the prices of futures contracts are marked to the market on a daily basis.

- 10. OPTIONS Options are special contractual arrangements giving the owner the right to buy or sell an asset at a fixed price anytime on or before a given date. they give the buyer the right, but not the obligation to exercise the contract.

- 11. Two types of options contract Call option Put option

- 12. CALL OPTIONS A call option gives the owner the right to buy an asset at a fixed price during a particular time period The Value of a Call Option at Expiration If the stock price is greater than the exercise price, we say that the call is in the money The payoff of a call option at expiration is 1.If Stock Price Is Greater Than Strike price Call-option value=Stock price-Strike price

- 13. If Stock Price Is Lesser Than Strike Price Call-option value=0

- 14. Put Options a put gives the holder the right to sell the stock for a fixed exercise price. The Value of a Put Option at Expiration

- 15. SELLING OPTIONS An investor who sells (or writes) a call on common stock promises to deliver shares of the common stock if required to do so by the call-option holder the seller loses money if the stock price ends up above the exercise price and he merely avoids losing money if the stock price ends up below the exercise price Why would the seller of a call place himself in such a precarious position?

- 16. sell-a-call

- 17. sell-a-put

- 18. VALUING OPTIONS determine the value of options when you buy them well before expiration. Bounding the Value of a Call Arbitrage profit Upper bound: It turns out that the upper boundary is the price of the underlying stock.

- 19. Upper and Lower Boundaries of Call-Option Values

- 20. The Factors Determining Call-Option Values 1)Exercise Price 2)Expiration Date 3)Stock Price 4)The Key Factor: The Variability of the Underlying Asset

- 21. Ěý

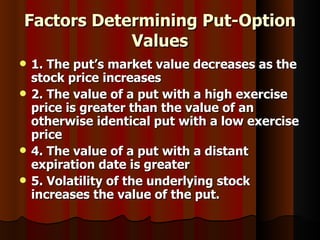

- 22. Factors Determining Put-Option Values 1. The put’s market value decreases as the stock price increases 2. The value of a put with a high exercise price is greater than the value of an otherwise identical put with a low exercise price 4. The value of a put with a distant expiration date is greater 5. Volatility of the underlying stock increases the value of the put.

- 23. SWAPS CONTRACTS Swaps are arrangements between two counterparts to exchange cash flows over time two basic types are interest-rate swaps currency swaps .

- 24. Currency swaps Currency swaps are swaps of obligations to pay cash flows in one currency for obligations to pay in another currency