Budget methods

- 1. Budget methods 1

- 2. Main contents âĒ Incremental budgeting vs. Zero-based budgeting âĒ Top down budgeting vs. bottom up budgeting 2

- 3. Incremental budgeting and Zero-based budgeting 3

- 4. Incremental budgeting âĒ Incremental budgeting definition: Prepared based on the current periodâs budget with some added amounts regarding inflation or planned increases in sales and costs (Ann, 2011) âĒ Advantages: âĒ Simple to prepare and understand âĒ Consistent basis âĒ Better co-ordination between budgets âĒ Disadvantages: âĒ Totally ignore the impact of changes âĒ No incentive in development and innovation âĒ Encourages spending up to the budget âĒ This approach is not recommended as it fails to take into 4 account changing circumstances

- 5. Zero-based budgeting âĒ In the mid-20th century, money got tighter and problems associated with incremental budgeting began to give rise to a feeling that changes were needed. âĒ By the 1960, ZBB emerged in the concept. âĒ ZBB definition It starts each budget period from a base of zero, with no reference to the prior period (Anon, 2010). Every department function has to justify the resources used for their relevant activities. Unless the activity is justified, there will be no resource allocation for it. 5

- 6. Zero-based budgeting âĒ Stages of ZBB âĒ Step 1: Activities are identified by the managers. These activities are then described in decision packages. âĒ Step 2: Management will then rank all the packages in the order of decreasing benefits to the organisation âĒ Step 3: Resources in the budget are then allocated on order of priority up to the spending level. 6

- 7. Zero-based budgeting âĒ Advantages âĒ Efficient allocation of resources âĒ Drives managers to find cost reduction methods âĒ Identifies and eliminates wasteful activities âĒ Disadvantages âĒ Very complex ï Time and manpower consuming âĒ Necessary to train employees, especially managers âĒ In a relatively large corporation, the amount of information might be too excessive to go through all. Compressing the information might take out critical details âĒ Can result in internal conflicts between departments over budget allocation. 7

- 8. Consideration âĒ Since all the costs are required to be justified, it seems inappropriate to use ZBB for the whole budgeting process. One way of overcoming this drawback is to use this method selectively. 8

- 9. Bottom-up budgeting and top-down budgeting 9

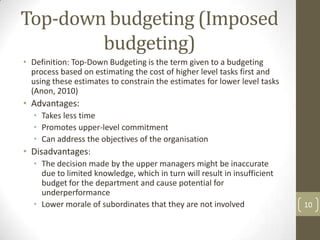

- 10. Top-down budgeting (Imposed budgeting) âĒ Definition: Top-Down Budgeting is the term given to a budgeting process based on estimating the cost of higher level tasks first and using these estimates to constrain the estimates for lower level tasks (Anon, 2010) âĒ Advantages: âĒ Takes less time âĒ Promotes upper-level commitment âĒ Can address the objectives of the organisation âĒ Disadvantages: âĒ The decision made by the upper managers might be inaccurate due to limited knowledge, which in turn will result in insufficient budget for the department and cause potential for underperformance âĒ Lower morale of subordinates that they are not involved 10

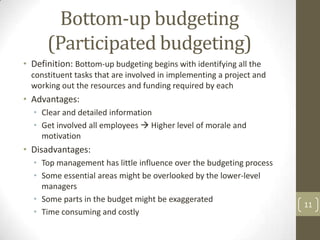

- 11. Bottom-up budgeting (Participated budgeting) âĒ Definition: Bottom-up budgeting begins with identifying all the constituent tasks that are involved in implementing a project and working out the resources and funding required by each âĒ Advantages: âĒ Clear and detailed information âĒ Get involved all employees ï Higher level of morale and motivation âĒ Disadvantages: âĒ Top management has little influence over the budgeting process âĒ Some essential areas might be overlooked by the lower-level managers âĒ Some parts in the budget might be exaggerated 11 âĒ Time consuming and costly

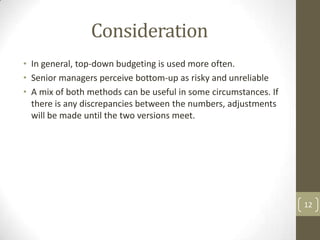

- 12. Consideration âĒ In general, top-down budgeting is used more often. âĒ Senior managers perceive bottom-up as risky and unreliable âĒ A mix of both methods can be useful in some circumstances. If there is any discrepancies between the numbers, adjustments will be made until the two versions meet. 12

- 13. Thank you for listening! 13