Budgetary control

Download as pptx, pdf0 likes1,085 views

This document provides information and formulas for calculating different types of variances, including material, direct labor, and variable overhead variances. It explains how to calculate price and quantity variances for materials, as well as rate and efficiency variances for direct labor and variable overhead. Formulas are given for each variance, and examples are worked through step-by-step to demonstrate how to calculate variances for different companies and time periods. The document aims to teach the concepts and calculations involved in variance analysis.

Budgetary control

- 1. Budgetary ControlSTANDARD COST All rights reservedAHMAD ROSLANFaculty business management and accountancy

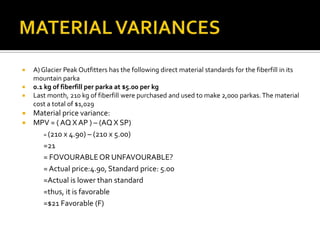

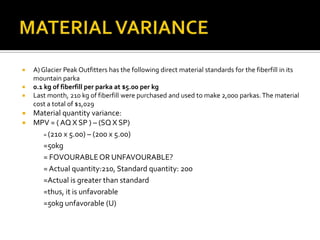

- 2. MATERIAL VARIANCES A) Glacier Peak Outfitters has the following direct material standards for the fiberfill in its mountain parka 0.1 kg of fiberfill per parka at $5.00 per kgLast month, 210 kg of fiberfill were purchased and used to make 2,000 parkas. The material cost a total of $1,029Direct materials price. Quantity, and total spending variancesHow to solve this problem?

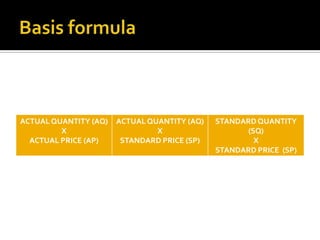

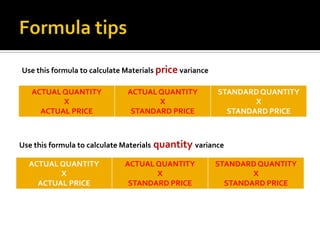

- 4. Formula tipsUse this formula to calculate MaterialspricevarianceUse this formula to calculate Materialsquantityvariance

- 5. MATERIAL VARIANCESA) Glacier Peak Outfitters has the following direct material standards for the fiberfill in its mountain parka 0.1 kg of fiberfill per parka at $5.00 per kgLast month, 210 kg of fiberfill were purchased and used to make 2,000 parkas. The material cost a total of $1,029Material price variance:MPV = ( AQ X AP ) – (AQ X SP) = (210 x 4.90) – (210 x 5.00)=21= FOVOURABLE OR UNFAVOURABLE?= Actual price:4.90, Standard price: 5.00=Actual is lower than standard=thus, it is favorable=$21 Favorable (F)

- 6. MATERIAL VARIANCEA) Glacier Peak Outfitters has the following direct material standards for the fiberfill in its mountain parka 0.1 kg of fiberfill per parka at $5.00 per kgLast month, 210 kg of fiberfill were purchased and used to make 2,000 parkas. The material cost a total of $1,029Material quantity variance:MPV = ( AQ X SP ) – (SQ X SP) = (210 x 5.00) – (200 x 5.00)=50kg= FOVOURABLE OR UNFAVOURABLE? = Actual quantity:210, Standard quantity: 200 =Actual is greater than standard =thus, it is unfavorable=50kg unfavorable (U)

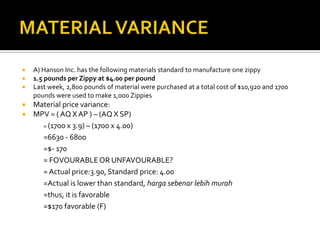

- 7. MATERIAL VARIANCEA) Hanson Inc. has the following materials standard to manufacture one zippy1.5 pounds per Zippy at $4.00 per pound Last week, 2,800 pounds of material were purchased at a total cost of $10,920 and 1700 pounds were used to make 1,000 ZippiesMaterial price variance:MPV = ( AQ X AP ) – (AQ X SP) = (1700 x 3.9) – (1700 x 4.00)=6630 - 6800=$- 170 = FOVOURABLE OR UNFAVOURABLE? = Actual price:3.90, Standard price: 4.00 =Actual is lower than standard, hargasebenarlebihmurah =thus, it is favorable=$170 favorable (F)

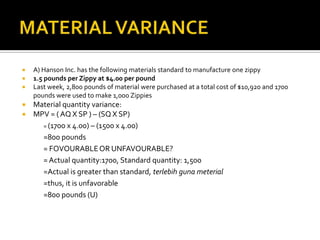

- 8. MATERIAL VARIANCEA) Hanson Inc. has the following materials standard to manufacture one zippy1.5 pounds per Zippy at $4.00 per pound Last week, 2,800 pounds of material were purchased at a total cost of $10,920 and 1700 pounds were used to make 1,000 ZippiesMaterial quantity variance:MPV = ( AQ X SP ) – (SQ X SP) = (1700 x 4.00) – (1500 x 4.00)=800 pounds = FOVOURABLE OR UNFAVOURABLE? = Actual quantity:1700, Standard quantity: 1,500 =Actual is greater than standard, terlebihgunameterial =thus, it is unfavorable=800 pounds (U)

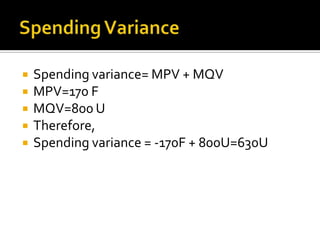

- 9. Spending Variance Spending variance= MPV + MQVMPV=170 FMQV=800 UTherefore, Spending variance = -170F + 800U=630U

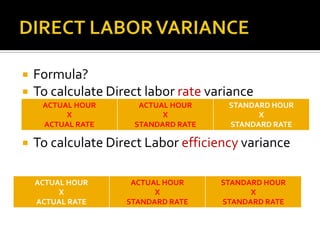

- 10. DIRECT LABOR VARIANCEFormula?To calculate Direct labor rate varianceTo calculate Direct Labor efficiency variance

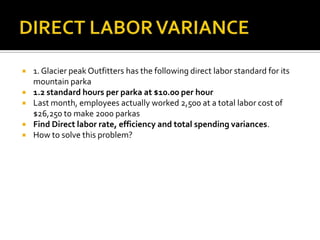

- 11. DIRECT LABOR VARIANCE1. Glacier peak Outfitters has the following direct labor standard for its mountain parka1.2 standard hours per parka at $10.00 per hourLast month, employees actually worked 2,500 at a total labor cost of $26,250 to make 2000 parkasFind Direct labor rate, efficiency and total spending variances.How to solve this problem?

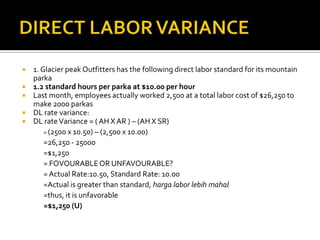

- 12. DIRECT LABOR VARIANCE1. Glacier peak Outfitters has the following direct labor standard for its mountain parka1.2 standard hours per parka at $10.00 per hourLast month, employees actually worked 2,500 at a total labor cost of $26,250 to make 2000 parkasDL rate variance:DL rate Variance = ( AH X AR ) – (AH X SR) = (2500 x 10.50) – (2,500 x 10.00)=26,250 - 25000=$1,250 = FOVOURABLE OR UNFAVOURABLE? = Actual Rate:10.50, Standard Rate: 10.00 =Actual is greater than standard, harga labor lebihmahal =thus, it is unfavorable=$1,250 (U)

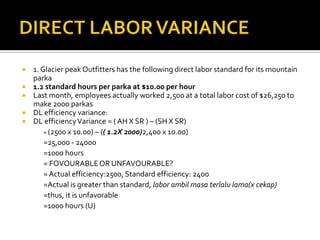

- 13. DIRECT LABOR VARIANCE1. Glacier peak Outfitters has the following direct labor standard for its mountain parka1.2 standard hours per parka at $10.00 per hourLast month, employees actually worked 2,500 at a total labor cost of $26,250 to make 2000 parkasDL efficiency variance:DL efficiency Variance = ( AH X SR ) – (SH X SR) = (2500 x 10.00) – (( 1.2X 2000)2,400 x 10.00) =25,000 - 24000=1000 hours = FOVOURABLE OR UNFAVOURABLE? = Actual efficiency:2500, Standard efficiency: 2400 =Actual is greater than standard, labor ambilmasaterlalu lama(x cekap) =thus, it is unfavorable=1000 hours (U)

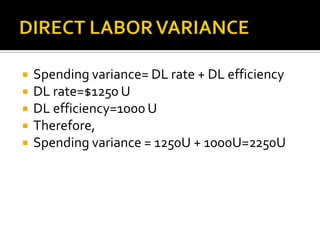

- 14. DIRECT LABOR VARIANCESpending variance= DL rate + DL efficiency DL rate=$1250 UDL efficiency=1000 UTherefore, Spending variance = 1250U + 1000U=2250U

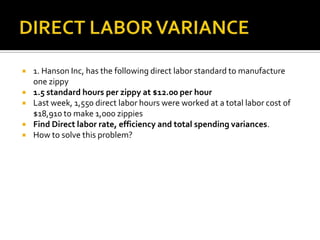

- 15. DIRECT LABOR VARIANCE1. Hanson Inc, has the following direct labor standard to manufacture one zippy1.5 standard hours per zippy at $12.00 per hourLast week, 1,550 direct labor hours were worked at a total labor cost of $18,910 to make 1,000 zippiesFind Direct labor rate, efficiency and total spending variances.How to solve this problem?

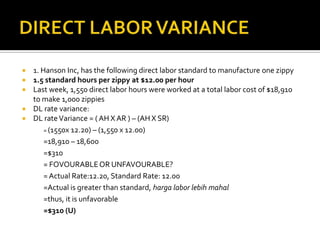

- 16. DIRECT LABOR VARIANCE1. Hanson Inc, has the following direct labor standard to manufacture one zippy1.5 standard hours per zippy at $12.00 per hourLast week, 1,550 direct labor hours were worked at a total labor cost of $18,910 to make 1,000 zippiesDL rate variance:DL rate Variance = ( AH X AR ) – (AH X SR) = (1550x 12.20) – (1,550 x 12.00)=18,910 – 18,600=$310 = FOVOURABLE OR UNFAVOURABLE? = Actual Rate:12.20, Standard Rate: 12.00 =Actual is greater than standard, harga labor lebihmahal =thus, it is unfavorable=$310 (U)

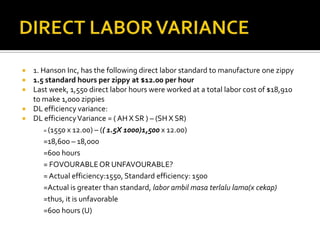

- 17. DIRECT LABOR VARIANCE1. Hanson Inc, has the following direct labor standard to manufacture one zippy1.5 standard hours per zippy at $12.00 per hourLast week, 1,550 direct labor hours were worked at a total labor cost of $18,910 to make 1,000 zippiesDL efficiency variance:DL efficiency Variance = ( AH X SR ) – (SH X SR) = (1550 x 12.00) – (( 1.5X 1000)1,500x 12.00)=18,600 – 18,000=600 hours = FOVOURABLE OR UNFAVOURABLE? = Actual efficiency:1550, Standard efficiency: 1500 =Actual is greater than standard, labor ambilmasaterlalu lama(x cekap) =thus, it is unfavorable=600 hours (U)

- 18. DIRECT LABOR VARIANCESpending variance= DL rate + DL efficiency DL rate=$310 UDL efficiency=600 UTherefore, Spending variance = 310 U + 600 U=910U

- 19. VARIABLE OVERHEAD VARIANCES1. Glacier peak Outfitters has the following direct variable manufacturing overhead labor standard for its mountain parka1.2 standard hours per parka at $4.00 per hourLast month, employees actually worked 2,500 hours to make 2000 parkas. Actual variable manufacturing overhead for the month was $10,500Find VOH rate, efficiency and total spending variances.How to solve this problem?

- 20. VARIABLE OVERHEAD VARIANCES1. Glacier peak Outfitters has the following direct variable manufacturing overhead labor standard for its mountain parka1.2 standard hours per parka at $4.00 per hourLast month, employees actually worked 2,500 hours to make 2000 parkas. Actual variable manufacturing overhead for the month was $10,500VOH rate variance:VOH rate Variance = ( AH X AR ) – (AH X SR) = (2500 x 4.2) – (2,500 x 4.00)=5,115 – 4,650=$465 = FOVOURABLE OR UNFAVOURABLE? = Actual Rate:4.2, Standard Rate: 4.00 =Actual is greater than standard, harga labor lebihmahal =thus, it is unfavorable=$465 (U)

- 21. VARIABLE OVERHEAD VARIANCES1. Glacier peak Outfitters has the following direct variable manufacturing overhead labor standard for its mountain parka1.2 standard hours per parka at $4.00 per hourLast month, employees actually worked 2,500 hours to make 2000 parkas. Actual variable manufacturing overhead for the month was $10,500VOH efficiency variance:VOH efficiency Variance = ( AH X SR ) – (SH X SR) = (2500 x 4.00) – (( 1.2X 2000)2400x 4.00)=10,000 – 9,600=400 hours = FOVOURABLE OR UNFAVOURABLE? = Actual efficiency:2500, Standard efficiency: 2400 =Actual is greater than standard, labor ambilmasaterlalu lama(x cekap) =thus, it is unfavorable=400 hours (U)

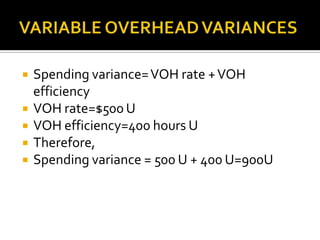

- 22. VARIABLE OVERHEAD VARIANCESSpending variance= VOH rate + VOH efficiency VOH rate=$500 UVOH efficiency=400 hours UTherefore, Spending variance = 500 U + 400 U=900U

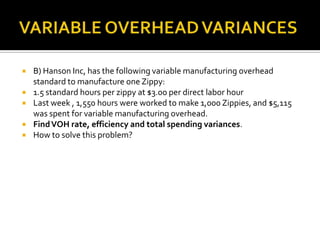

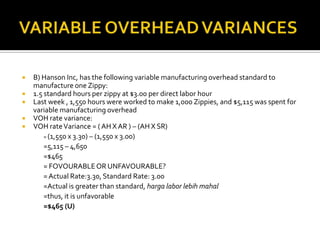

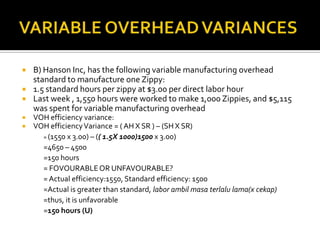

- 23. VARIABLE OVERHEAD VARIANCESB) Hanson Inc, has the following variable manufacturing overhead standard to manufacture one Zippy:1.5 standard hours per zippy at $3.00 per direct labor hourLast week , 1,550 hours were worked to make 1,000 Zippies, and $5,115 was spent for variable manufacturing overhead.Find VOH rate, efficiency and total spending variances.How to solve this problem?

- 24. VARIABLE OVERHEAD VARIANCESB) Hanson Inc, has the following variable manufacturing overhead standard to manufacture one Zippy:1.5 standard hours per zippy at $3.00 per direct labor hourLast week , 1,550 hours were worked to make 1,000 Zippies, and $5,115 was spent for variable manufacturing overhead VOH rate variance:VOH rate Variance = ( AH X AR ) – (AH X SR) = (1,550 x 3.30) – (1,550 x 3.00)=5,115 – 4,650=$465 = FOVOURABLE OR UNFAVOURABLE? = Actual Rate:3.30, Standard Rate: 3.00 =Actual is greater than standard, harga labor lebihmahal =thus, it is unfavorable=$465 (U)

- 25. VARIABLE OVERHEAD VARIANCESB) Hanson Inc, has the following variable manufacturing overhead standard to manufacture one Zippy:1.5 standard hours per zippy at $3.00 per direct labor hourLast week , 1,550 hours were worked to make 1,000 Zippies, and $5,115 was spent for variable manufacturing overhead VOH efficiency variance:VOH efficiency Variance = ( AH X SR ) – (SH X SR) = (1550 x 3.00) – (( 1.5X 1000)1500x 3.00)=4650 – 4500=150 hours = FOVOURABLE OR UNFAVOURABLE? = Actual efficiency:1550, Standard efficiency: 1500 =Actual is greater than standard, labor ambilmasaterlalu lama(x cekap) =thus, it is unfavorable=150 hours (U)

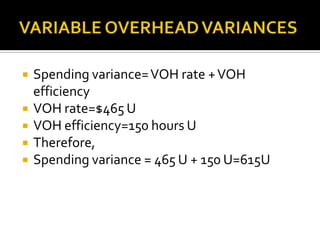

- 26. VARIABLE OVERHEAD VARIANCESSpending variance= VOH rate + VOH efficiency VOH rate=$465 UVOH efficiency=150 hours UTherefore, Spending variance = 465 U + 150 U=615U

- 27. Thank you for using this PPTI wish good luck to you