Can Video Make Money for LTE Networks ?

Download as pptx, pdf0 likes829 views

The document discusses the transformation of video services in the context of LTE networks and the evolving role of handsets as central hubs for content delivery. It highlights challenges like net neutrality, monetization, and the need for innovation in service delivery, while also emphasizing the significant growth in mobile and tablet video viewership. Future models proposed include fully aggregated services, automated content marketplaces, and narrowcast channels targeting specific communities of interest.

Can Video Make Money for LTE Networks ?

- 1. Becoming The Video Hub How LTE services can make the most of video services Iolo Jones CEO, TV Everywhere

- 2. Today ¨C the Network as the hub

- 3. The Network is Commoditised ? Landline Commoditised. ? Mobile Commoditised. ? Broadband Commoditised. ? TV Hmmmmˇ

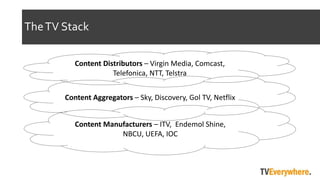

- 4. TheTV Stack Content Distributors ¨C Virgin Media, Comcast, Telefonica, NTT, Telstra Content Aggregators ¨C Sky, Discovery, Gol TV, Netflix Content Manufacturers ¨C ITV, Endemol Shine, NBCU, UEFA, IOC

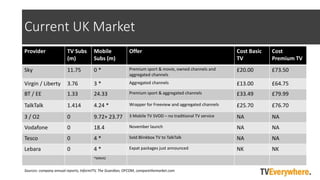

- 5. Provider TV Subs (m) Mobile Subs (m) Offer Cost Basic TV Cost Premium TV Sky 11.75 0 * Premium sport & movie, owned channels and aggregated channels ?20.00 ?73.50 Virgin / Liberty 3.76 3 * Aggregated channels ?13.00 ?64.75 BT / EE 1.33 24.33 Premium sport & aggregated channels ?33.49 ?79.99 TalkTalk 1.414 4.24 * Wrapper for Freeview and aggregated channels ?25.70 ?76.70 3 / O2 0 9.72+ 23.77 3 Mobile TV SVOD ¨C no traditional TV service NA NA Vodafone 0 18.4 November launch NA NA Tesco 0 4 * Sold Blinkbox TV to TalkTalk NA NA Lebara 0 4 * Expat packages just announced NK NK *MNVO Sources: company annual reports, InformITV, The Guardian, OFCOM, comparethemarket.com Current UK Market

- 6. Current Models ? Nothing ? Wrapper ? Aggregation ? Own service

- 7. Video over LTE -The Issues ? Net Neutrality ? Latency ? Differentiation ? Not ˇ®me too TVˇŻ ? Monetization ? Cost of rights ? Cost of delivery ? How to monetize ? Price

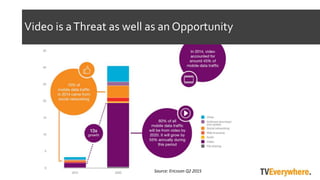

- 8. Source: Ericsson Q2 2015 Video is aThreat as well as an Opportunity

- 9. Changing Demographies Offer Disruption Since 2012, mobile and tablet video viewership is up 532 %. 48 % of people around the globe who viewed mobile videos watched content for 30 minutes or more. Source: Ooyala

- 10. TV everywhere ¨C the handset as the hub

- 11. The Evolution of the Handset into a Hub ? Payment gateway ? Conditional access pass ? UIUX aggregator ? Projector ¨C replacing set top box

- 12. MakingThe HubWork ? Implement payment gateway for content owners ? Provide robust security and delivery infrastructure ¨C push the workload to the content providers ? Develop a world class UI/UX ? Stream to screens - for now, develop an app for Roku, Chromecast, Miracast, Airplay, etc.. (in the future project and stream directly via wireless to any screen) ? Innovate!

- 13. Future Models ? Fully aggregated service ? Automated content marketplaces ? Reverse bidding platforms ? Curated user services ? Narrowcast channels

- 14. Fully Aggregated Service ? Imagine all of your content in one ˇ®meta appˇŻ ? Not twenty individual apps ? Easier said than done..

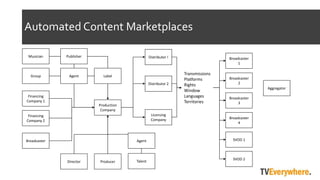

- 15. Automated Content Marketplaces Musician Publisher Group Agent Label Financing Company 1 Financing Company 2 Broadcaster Production Company Director Producer Talent Distributor ! Distributor 2 Licensing Company Broadcaster 1 Broadcaster 2 Broadcaster 3 Broadcaster 4 SVOD 1 SVOD 2 Transmissions Platforms Rights Window Languages Territories Agent Aggregator

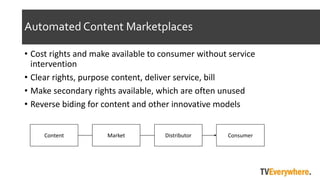

- 16. Automated Content Marketplaces ? Cost rights and make available to consumer without service intervention ? Clear rights, purpose content, deliver service, bill ? Make secondary rights available, which are often unused ? Reverse biding for content and other innovative models Content ConsumerMarket Distributor

- 17. Curated User Content - now everyone is a vidiographer ? Vine ? Meerkat ? Periscope ? Twitter ? Facebook ? YouTube ? Making Digg, BuzzFeed etc.. the new broadcasters

- 18. Narrowcasting - Communities of Interest ? Appealing to aggregated vertical markets ? Based on interests, eg horses, knitting, cycling, sailing, DIY, wine ? Hyperlocal channels ? Expatriate channels

- 19. www.tveverywhere.org www.iptvtimes.net Iolo Jones CEO, TV Everywhere @ioloj

Editor's Notes

- #2: Hi there, IˇŻm Iolo Jones, the CEO of TV Everywhere (my lawyers have asked me to point out thatˇŻs with a capital E!). Our business builds platforms to enable other companies to make money from their video and TV content and services, we work for everyone from the worldˇŻs largest ad agency to local broadcasters, from sports federations to corporations.

- #3: About ten years ago, at a similar event in these halls I did a presentation on the technical challenges of delivering video over mobile networks ¨C at the time we were working on building a transcoding farm with KPN. I think a decade on we can all accept that most of the technical problems with delivering video to mobile devices have been tackled successfully. The challenges now are around the business model.

- #4: The problem is that most quad play services have become commoditised, almost before networks have been rolled out. The one outlier is TV and video. So, can this be a panacea ?

- #5: The trouble with TV and video rights is that they are complex and that there are players in each part of the value chain who want to enter other parts of the value chain as the current flurry of mergers across the globe shows.

- #6: And the UK is a case in point. If we look at the current situation in the UK market you can see that companies that are good at content traditionally havenˇŻt been good at mobile and vice versa. It was a lesson learnt some time ago by Telefonica after they purchased Endemol, of course, so this is nothing new. Still, it hasnˇŻt stopped many of these companies jumping into bed with each other. There are a few names up there worth mentioning. Tesco, the giant retailer used to be the biggest seller of physical videos on DVD in the UK, now they are totally out of the game despite having a pretty successful MVNO model. Ironically itˇŻs TalkTalk who bought their SVOD service, Blinkbox. Lebara is an interesting entrant to the market with their announcement last week that they are going to push expatriate content to their customer base.

- #7: ThatˇŻs a brave approach and IˇŻll return to that later, but the current business models revolve around doing nothing, providing a wrapper for existing services ¨C basically carrying apps, aggregating content, or in rare cases, launching an original service. But even in this final category, the tendency is to emulate not innovate.

- #8: So letˇŻs look more closely what the issues are: first of all the regulatory environment and the upkeep of net neutrality principles means that it is difficult to do any volume based carriage deals. Your only option with Netflix is to promote them and take a very small cut of their subscription fee as they suck the capacity of your LTE network dry. There are still latency issues that preclude models such as added value services in sports arenas, which is something weˇŻre doing some work on with a Premiership team in the UK. Still thousands of people accessing the same content at the same time in the same cell is not going to end well. This is an area where P2P may make a technical comeback. Perhaps the biggest problem, and the one IˇŻm mainly going to address today, is that of differentiation. How do you stop the customer from yawning when you tell them what you have on offer ? Finally, there the $64 million dollar ¨C and the rest ¨C question is how you make money when it costs so much to buy content, especially premium content in a highly price sensitive marketplace.

- #9: But the trouble is, you canˇŻt afford NOT to do anything about it. According to Ericsson, 45% of your network traffic is already video and this is going to rise to 60% by 2020.

- #10: But the good news is that there is a younger generation of viewers who consume video and TV content in a very different way and theyˇŻre watching lots and lots of video on their smartphones and tablets. And not just short form either. In my experience itˇŻs a total myth that the smaller the device the shorter the program should be..

- #11: So, how do we change things ? What do we need to do ? Well, I think that an important first step is to change the paradigm and to stop looking at video as a network service, but to look at it as a handset service. In the era of TV everywhere (with a small e to keep the lawyers happy), the handset is the hub.

- #12: So letˇŻs look further at what this amazing device can do. First of all it can take payment and do this in an easy and unobtrusive way. To pay for premium sports events on Sky you have to dial in and pay. ItˇŻs not so with mobile billing. It beggars belief that operators have allowed so many other companies to steal a march on them in this area. A good billing API would attract content owners. Secondly it can act as a conditional access pass, so that you can protect the delivery of content. Thirdly you can aggregate services into a central view. Unfortunately I currently have twenty or so video apps I have to use to watch everything I want to watch on my mobile. Finally, and the tech for this is still nascent, it can act as a streamer and a projector ¨C why do you need a box or even a dongle if you can simply stream from your mobile wherever you are onto any screen by wireless comms?

- #13: So, in my opinion, these are the things that youˇŻll need to do, in my view, to enable a great video service over LTE.

- #14: And then you can start looking at some innovative services. To finish off, IˇŻve just listed a few here.

- #15: Get rid of all those icons and offer one app that talks to these apps and makes it easy for users. Of course this is easier said than done, but there are services like Zattoo and TV Catchup that have come close to succeeding.

- #16: The trouble with building your own content services is that itˇŻs really, really complicated and expensive. We own a company called rights tracker that tracks the rights for some of the worldˇŻs leading TV properties and this is what one, simple rights position might look like ¨C and there could be thousands of these each difference.

- #17: So weˇŻre working on creating a centralised rights marketplace where anyone can push their rights or acquire those rights. This is especially useful for secondary rights, things like the live coverage of sports matched that you can never see again, or slightly older rights for dramas: this is how Netflix established themselves. There is also the possibility of engendering new business models such as reverse bidding ¨C allowing users to outbid broadcasters for rights

- #18: Then there is the boom in self produced content that is badly curated on places like YouTube and is currently fragmenting onto multiple platforms such as Vine and Facebook. Already services like Digg and Buzzfeed are curating and aggregating a service based on these feeds. These guys are becoming the new broadcasters.

- #19: Finally, back to Lebara and to one of my favourite approaches to building a market. You donˇŻt have to try and get everyone day one - Zuckerberg started with Harvard - you can start with minority interests and aggregate audiences. The costs and the content are far cheaper and viewers are more fanatical.

- #20: Of course, this is only the start of the story and if youˇŻd like to discuss this any more IˇŻd love to hear from you on Twitter, on my blog where IˇŻll be posting this presentation, or on our corporate website. Thank you.