Cape Town Tourism Industry Forums

ŌĆó

1 likeŌĆó529 views

The document discusses a marketing presentation for the Cape Town tourism industry. It outlines issues facing the industry, including declining market share and job losses since the global financial crisis. A proposed intervention plan aims to resolve these issues by changing Cape Town's marketing mix, promoting it as an ideal short break destination, and building sustainable demand from core international markets through various initiatives. Feedback on the plan is sought from attendees.

Cape Town Tourism Industry Forums

- 1. WELCOME Cape Town Tourism Industry Presentation: The marketing of Cape Town August 2011

- 3. AGENDA AIMS THE SITUATION AND LEARNINGS THE PROPOSED PLAN DISCUSSION

- 4. AGENDA An open forum discussion of a proposed intervention strategy to resolve some of the issues affecting the industry We hope to: receive feedback obtain views

- 5. BACKGROUND

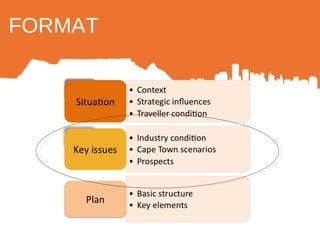

- 6. FORMAT

- 7. THE WORLD CONDITION WTO SAYS OECD SAYSŌĆ” International Tourism: First results of 2011 confirm consolidation of growth

- 9. THE WORLD CONDITION The urbanisation and the rise of the urban tourist

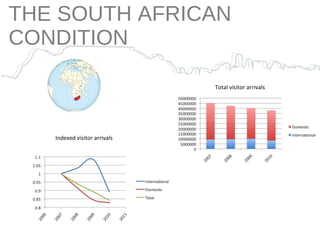

- 10. THE SOUTH AFRICAN CONDITION Total visitor arrivals Indexed visitor arrivals

- 11. THE SOUTH AFRICAN CONDITION

- 12. LEARNINGS FROM AROUND THE WORLD

- 13. LEARNINGS FROM AROUND THE WORLD

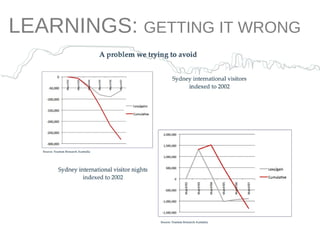

- 14. LEARNINGS: GETTING IT WRONG

- 15. THE CONSUMER: What the hell just happened? Global Financial crisis

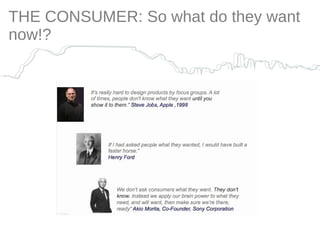

- 16. THE CONSUMER: So what do they want now!?

- 17. THE CONSUMER: So what do they want now!? Value (?) Simplicity (?) Experiences (?) More to see and do at no cost !

- 18. THE CONSUMER: So what do they want now!?

- 19. THE CONSUMER: how they see cities

- 20. FORMAT

- 21. THE CAPE TOWN VISITOR INDUSTRY Global Financial Crisis (GFC) Reduced demand (?) Changed consumer condition Polarisation of consumer sentiment From 2007: -16% decline in market share ( 9.4% - 7.9%) 6 years of 0 or ŌĆō growth zero job creation effective loss of +-18000 job opportunities 118 businesses closed (last 24 months)

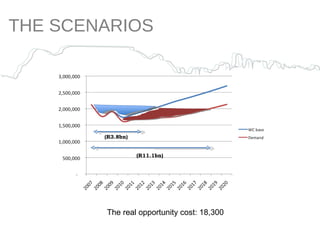

- 22. THE SCENARIOS (R3.8bn) (R11.1bn) The real opportunity cost: 18,300

- 23. OUT OF TURMOIL COMES OPPORTUNITY

- 24. OUR MARKETS

- 25. CAPE TOWNŌĆÖS (International) MARKETS Country Visitors % Contribution To total Rank UK 200067 18% 1 Germany 113524 10% 2 USA 106893 10% 3 Namibia 78582 7% 4 Netherlands 55886 5% 5 France 52247 5% 6 Zimbabwe 45426 4% 7 Australia 37821 3% 8 Italy 26044 2% 9 Mozambique 26005 2% 10 Country Spend % Contribution To total Rank UK R2.2bn 17% 1 USA R1,7bn 14% 2 Germany R1,3bn 10% 3 Netherlands R0,7bn 6% 4 Australia R0,6bn 4% 5 France R0,5bn 4% 6 Namibia R0,5bn 4% 7 China 0,4bn 3% 8 Canada R0,4bn 3% 9 India R0,3bn 2% 10

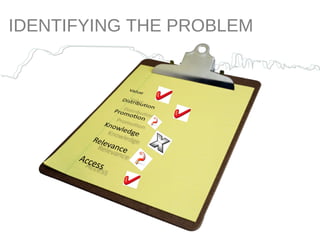

- 27. IDENTIFYING THE PROBLEM The city : in a brand vacuum Extremely competitive environment Proposition overly reliant on beauty Others define us Visitor industry: vulnerable and threatened

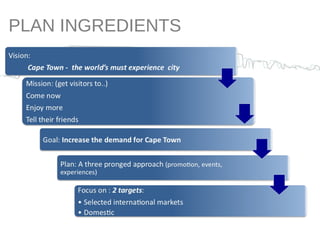

- 29. PLAN INGREDIENTS

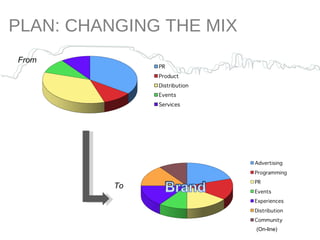

- 30. PLAN: CHANGING THE MIX From To (On-line)

- 31. PLAN: BEFORE WE START The Cape Town brand has existed for over 300 years It will be around for many more! What we deal with is the crafting of its messages to induce more people, who have different needs, to visit

- 32. ^ too In a world demanding simplicityŌĆ” We have much to offer

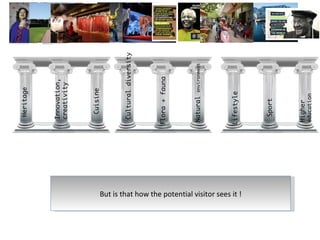

- 33. Heritage Cultural diversity Cuisine Flora + fauna Innovation, creativity Higher education Lifestyle Sport Natural environment But is that how the potential visitor sees it !

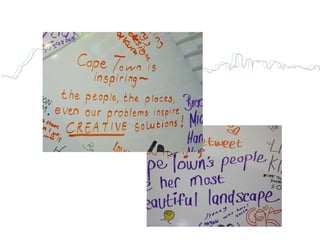

- 34. People do not see -

- 35. ╠²

- 36. PLAN: Ambassador

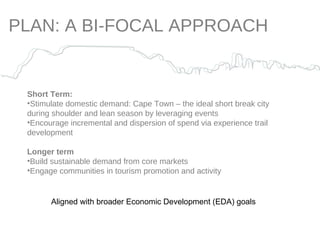

- 37. PLAN: A BI-FOCAL APPROACH Short Term: Stimulate domestic demand: Cape Town ŌĆō the ideal short break city during shoulder and lean season by leveraging events Encourage incremental and dispersion of spend via experience trail development Longer term Build sustainable demand from core markets Engage communities in tourism promotion and activity Aligned with broader Economic Development (EDA) goals

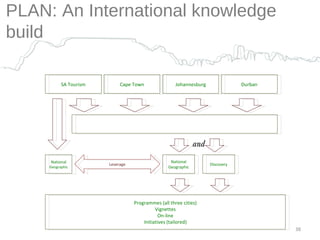

- 38. Cape Town Johannesburg Durban SA Tourism Discovery National Geographic Programmes (all three cities) Vignettes On-line Initiatives (tailored) National Geographic Leverage and PLAN: An International knowledge build

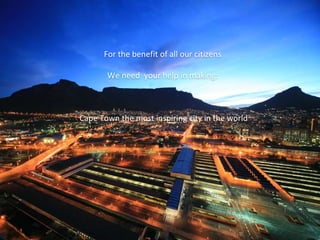

- 39. For the benefit of all our citizens We need your help in making: Cape Town the most inspiring city in the world