Central banks macro_adjustments

ŌĆóDownload as PPTX, PDFŌĆó

0 likesŌĆó319 views

Central banks can pursue three main types of exchange rate regimes: flexible rates, fixed rates, and managed floating rates. Under a flexible rate system, exchange rates are determined by market forces of supply and demand. Under a fixed rate system, a currency is pegged to another currency or commodity at a set price. Managed floating involves a central bank intervening in foreign exchange markets to influence exchange rates but not committing to maintain a specific fixed rate. Short-run macroeconomic equilibrium occurs when goods, money, and foreign exchange markets are all in balance simultaneously based on demand and supply interactions.

![Goods Market Equilibrium:

IS Curve (General form)

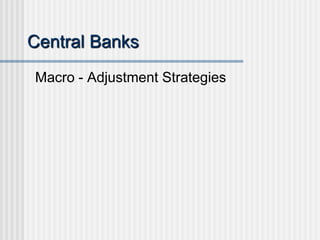

’ü« Goods market equilibrium condition:

AS = AD

Sn ŌĆō I = NX

- A0 + br + sY = NX0 ŌĆō mY

r = (A0 + NX0)/b ŌĆō (s + m)/b*Y

= (A0 + NX0)/b ŌĆō 1/╬▒b*Y where

A0 = C0 + c(R0 ŌĆō T0) + I0 + G0

NX0 = X0 ŌĆō Q0 + (g + j)eP*/P

╬▒ = 1/[1 ŌĆō c(1 ŌĆō t) + m]](https://image.slidesharecdn.com/centralbanksmacroadjustments-110127020305-phpapp02/85/Central-banks-macro_adjustments-12-320.jpg)

![LM Curve

r

M

L k/h

Y

[L0-MS/p]/h](https://image.slidesharecdn.com/centralbanksmacroadjustments-110127020305-phpapp02/85/Central-banks-macro_adjustments-27-320.jpg)

![Foreign Trade Sector Equilibrium:

The BP Curve

’ü« BP = 0 => NX + f (r ŌĆō rW) = 0

’ü« With no capital mobility (f = 0)

’ü« NX = NX0 - mY = 0

’ü« Y = NX0/m

’ü« With perfect capital mobility

’ü« r = rW

’ü« With imperfect capital mobility

’ü«NX0 ŌĆō mY + f (r ŌĆō rW) = 0

=> r = [rW - NX0/f] + m/f * Y](https://image.slidesharecdn.com/centralbanksmacroadjustments-110127020305-phpapp02/85/Central-banks-macro_adjustments-32-320.jpg)

Central banks macro_adjustments

- 1. Central Banks Macro - Adjustment Strategies

- 2. Central Banks & Exchange Rate Regimes ’ü« Flexible ’ü« Fixed ’ü« Managed Floating

- 3. Flexible Exchange Rate ’ü« Exchange rates are freely determined by the demand & supply of currencies.

- 4. Increase in Demand for ┬Ż Under Flexible Exchange Rate e$/┬Ż S┬Ż eŌĆÖ e D┬ŻŌĆÖ D┬Ż Q┬Ż

- 5. Fixed Exchange Rate ’ü« Gold standard (up to 1914) ’ü« Peg currency to gold at a mint parity. ($20.67/ounce of gold, ┬Ż4.25/ounce of gold).

- 6. Fixed Exchange Rate ’ü« Gold standard ’ü« Pegged rate system ’ü« Peg is the central value of exchange rate around which the government maintains narrow limits. (Haitian Gourde = $.20 since 1907 for a long period of time). ’ü« Government intervenes in foreign exchange markets to maintain the exchange rate within prescribed limits.

- 7. Increase in Demand for ┬Ż Under Pegged Rate System e$/┬Ż S┬Ż S┬ŻŌĆÖ ─ō D┬ŻŌĆÖ D┬Ż Q┬Ż

- 8. Fixed Exchange Rate ’ü« Devaluation ’ü« Peg is increased. ŌĆó ┬Ż was devalued in Nov. 1967 from $2.80/┬Ż to $2.40/┬Ż . ’ü« Revaluation ’ü« Peg is decreased.

- 9. Managed Floating ’ü« Government intervenes in the foreign exchange market to influence the exchange rate, but does not commit itself to maintain a certain fixed rate or some narrow limits around it.

- 10. Goods Market Equations ’ü« Y = C + I + G0 + NX (Equim condition) ’ü« C = C0 + cYd (Consn function) ’ü« Yd = Y ŌĆō T + R0 (Disposable income) ’ü« T = T0 + tY (Tax function) ’ü« I = I0 ŌĆō br (Investment function)

- 11. Goods Market Equations Endogenous Variables Parameters ’é¦ Y: National Income ’ü« c: MPC ’é¦ C: Consumption ’ü« t: Personal Tax Rate ’é¦ Yd: Disposable Income ’ü« b: Interest Sensitivity of I ’é¦ T : Personal Tax Revenue ’ü« C0 : Exogenous Component of C ’é¦ I : Investment ’ü« I0 : Exogenous Component of I ’ü« G0 : Government Expenditure ’ü« R0 : Transfer Payments ’ü« T0 : Fixed personal tax revenue

- 12. Goods Market Equilibrium: IS Curve (General form) ’ü« Goods market equilibrium condition: AS = AD Sn ŌĆō I = NX - A0 + br + sY = NX0 ŌĆō mY r = (A0 + NX0)/b ŌĆō (s + m)/b*Y = (A0 + NX0)/b ŌĆō 1/╬▒b*Y where A0 = C0 + c(R0 ŌĆō T0) + I0 + G0 NX0 = X0 ŌĆō Q0 + (g + j)eP*/P ╬▒ = 1/[1 ŌĆō c(1 ŌĆō t) + m]

- 13. Goods Market Equilibrium: IS Curve (Particular form) ’ü« r= A0 = Open economy multiplier 1/(s+m) =

- 14. IS Curve r [A0 + NX0/b I -1/ b S Y

- 15. Assets Markets ’ü« Markets in which money, bonds, stocks, real estate & other forms of wealth or stores of value are exchanged. ’ü« We consider two types of assets ’ü« domestic bonds ’ü« domestic money

- 16. Total Real Wealth in the Economy ’ü« Supply of real wealth ’ü« W/P = M/P + VS where W : Nominal wealth P : General price level VS: Stock of bonds ’ü« Demand for real wealth ’ü« W/P = L + V L: Demand for money V: Demand for bonds ’ü« In equilibrium ’ü« L + V = M/P + VS ’ü« Or (L - M/P) + (V - VS) = 0

- 17. Walras law ’ü« As long as money market is in equilibrium (i.e. L = M/P), bond market will also be in equilibrium.

- 18. Money Market Equations ’ü«L = M/P (Money market equim condition) ’ü« L = L0 + kY ŌĆō hr (Money demand) ’ü« M = uH (Money supply) ’ü« H = IR + CBC0 (High Powered Money) ’ü« IR = IR-1 + BP-1 (Int. Reserves adjustment)

- 19. Money Market Equations Endogenous Variables Exogenous Variables ’ü« L: Liquidity Demand ’ü« k: Income Sensitivity of L ’ü« r: Real interest Rate ’ü« h: Interest Sensitivity of L ’ü« M: Nominal Money Supply ’ü« u: Money Multiplier ’ü« H: High-Powered Money ’ü« L0: Exogenous component of L ’ü« IR: International Reserves ’ü« P: General Price Level ’ü« CBC0: Central Bank Credit

- 20. Demand for Money ’ü« The demand for money can be linearized to: L = L0 + kY ŌĆō hr

- 21. Supply of Money ’ü« MS = Cp + CD Cp: Currency (coin, dollar notes) in the hand of the public CD: Checkable deposits ’ü« M = H where ’ü« : the money multiplier ’ü« H: the high powered money (monetary base)

- 22. Central BankŌĆÖs Balance Sheet ’ü« Assets = IR + CBC ’ü« Liabilities = Cp + RE ’ü« IR + CBC = Cp + RE = H ’ü« H is created when the Central Bank acquires assets in the form of international reserves, IR (foreign exchange & gold), & Central Bank credit, CBC (loans, discounts & government bonds).

- 23. Simplified Central Bank Balance Sheet Assets Claims International Reserves $100b Currency $240 b Central Bank Credit $200b Cash in vaults $20 b Currency in the hand of the public $220b Deposits at the central bank $60 b High Powered Money $300b High Powered Money $300 b

- 24. Effects of Open Market Purchase on Central BankŌĆÖs Balance Sheet ’ü« Central bank purchase of securities (increase in CBC). ’ü« Central bank check is deposited in the commercial bank. ’ü« If the commercial bank decides to convert the check into cash, the currency in vault (RE) increases. ’ü« If commercial bank deposit the check at the central bank, commercial bank deposit (RE) increases.

- 25. Effects of a Drain of International Reserves on Central BankŌĆÖs Balance Sheet ’ü« IR decreases & Commercial bank deposit decreases. A BP deficit (surplus) decreases (increases) H &, therefore, tends to decrease (increase) MS.

- 26. Money Market Equilibrium: The LM Curve ’ü« MS/P = L0 + kY ŌĆō hr ’ü« r = (L0 - MS/P)/h + k/h Y ’ü« Particular: ’ü«r=

- 27. LM Curve r M L k/h Y [L0-MS/p]/h

- 28. Immediate-run Equilibrium ’ü« Immediate-run equilibrium is obtained when both the product & the money markets are in simultaneous equilibrium. ’ü« It occurs for a given level of fixed MS.

- 29. Immediate-run Equilibrium r M I rE L S Y YE

- 30. Foreign Trade Equations ’ü« BP = 0 (Foreign sector equim condition) ’ü« BP = NX + CF (Balance of Payments) ’ü« NX = X ŌĆō Q (Net Export function) ’ü« X = X0 + gePW/P (Export function) ’ü« Q = Q0 + mY ŌĆō jePW/P (Import function) ’ü« e = e-1 ŌĆō qBP (Exchange Rate adjustment) ’ü« CF = f(r ŌĆō rW) (Capital Flow equation)

- 31. Foreign Trade Equations Endogenous Variables Exogenous Variables ’ü« NX : Net Exports (Trade Surplus) ’ü« g : Exchange Rate Sensitivity of X ’ü« X : Value of Exports ’ü« Q : Value of Imports ’ü« m : Marginal Propensity to Imp. ’ü« BP : Balance of Payments ’ü« j : Exch. Rate Sensitivity of Q Surplus ’ü« f : Capital Mobility Coefficient ’ü« CF : Capital Flow (KAB Surplus) ’ü« e : Exchange Rate ’ü« q : Exchange Rate Coefficient (Domestic/Foreign Currency) ’ü« rW : World Interest Rate ’ü« X0 : Exogenous Component of X ’ü« Q0 : Exogenous Component of Q

- 32. Foreign Trade Sector Equilibrium: The BP Curve ’ü« BP = 0 => NX + f (r ŌĆō rW) = 0 ’ü« With no capital mobility (f = 0) ’ü« NX = NX0 - mY = 0 ’ü« Y = NX0/m ’ü« With perfect capital mobility ’ü« r = rW ’ü« With imperfect capital mobility ’ü«NX0 ŌĆō mY + f (r ŌĆō rW) = 0 => r = [rW - NX0/f] + m/f * Y

- 33. BP with No Capital Mobility ’ü« Y = NX0/m ’ü« In particular form: Y=

- 34. BP Curve with No Capital Mobility r BP Y NX0/m

- 35. BP Curve with Perfect Capital Mobility r r = rW BP Y

- 36. BP Curve with Imperfect Capital Mobility r BP Y

- 37. Short-run Equilibrium ’ü« An immediate-run equilibrium sustaining a BP deficit & losses of international reserves leads to a decline in MS & a leftward shift of the LM curve. ’ü« A short-run equilibrium exists when all the three markets are in equilibrium.

- 38. Short-run Equilibrium with No Capital Mobility r BP M I rE L S Y YE

- 39. Short-run Equilibrium with Perfect Capital Mobility r M I rE BP L S Y YE

- 40. Short-run Equilibrium with Imperfect Capital Mobility r M I BP rE L S YE Y

- 41. Sterilization Operations ’ü«Operations carried out by the Central Bank in order to neutralize the effects that its intervention in foreign exchange markets has on H. ’ü« H = IR + CBC = 0 or CBC = - IR