Cost of capital structure and international budgeting

Download as PPTX, PDF0 likes39 views

Cost of capital structures and International Budgeting Standards and Multinational Financial Management

1 of 18

Download to read offline

Recommended

Cost of capital, international financial management

Cost of capital, international financial managementAshutosh136471

╠²

User

in short

ChatGPT

Capital budgeting is about choosing the right long-term investments, while cost of capital is the expense associated with financing those investments.Ch 5 international capital structure and cost of capital latest

Ch 5 international capital structure and cost of capital latestShadina Shah

╠²

This document discusses international capital structures and costs of capital. It covers several topics: (1) how the cost of capital is estimated using weighted average cost of capital and CAPM models; (2) how segmented vs integrated capital markets impact cost of capital calculations; (3) evidence that costs of capital differ among countries; (4) benefits and costs of cross-border stock listings for reducing costs; and (5) how foreign ownership restrictions can increase costs through pricing-to-market effects. The chapter aims to explain how multinational firms can reduce their costs of capital through international diversification and accessing different capital markets.Multinational cost and capital structure

Multinational cost and capital structureNits Kedia

╠²

The document discusses how multinational corporations determine their cost of capital and establish optimal capital structures. It explains that an MNC's cost of capital may differ from domestic firms due to their size, access to international markets, diversification across countries, and exposure to exchange rate and country risks. The cost of capital also varies by country based on interest rates, risk premiums, and tax laws. An MNC considers these corporate and country characteristics when deciding how much debt and equity to use in different subsidiaries to minimize its overall cost of capital.Multinational cost and capital structure

Multinational cost and capital structureStudsPlanet.com

╠²

The document discusses how multinational corporations determine their cost of capital and establish optimal capital structures. It explains that an MNC's cost of capital may differ from domestic firms due to their size, access to international markets, diversification across countries, and exposure to exchange rate and country risks. The cost of capital also varies by country based on interest rates, risk premiums, and tax laws. An MNC considers these corporate and country characteristics when deciding how much debt and equity to use in different subsidiaries to minimize its overall cost of capital.

Internationalcostofcapital 110216232906-phpapp01

Internationalcostofcapital 110216232906-phpapp01Barkha Goyal

╠²

This document discusses the cost of capital from an international perspective. It defines key terms like weighted average cost of capital and explains how cost of capital is determined. It also discusses how segmented versus integrated capital markets can impact a firm's cost of capital calculation. The document notes that international diversification can lower a firm's cost of capital. Cross-border stock listings are also discussed as a way for firms to potentially achieve a lower cost of capital.International financing options

International financing optionssharmahitanshu

╠²

The document discusses various international financing options for companies, including equity capital and debt capital. It describes equity capital options such as depository receipts (DRs), which allow foreign companies to list shares on a domestic exchange. It distinguishes between sponsored DRs, which companies actively participate in, and unsponsored DRs, issued without company agreement. Debt capital options discussed include eurobonds, bonds denominated in non-domestic currency, and foreign bonds, bonds issued by foreign companies denominated in the local currency.MKI-Basic15-Jeff Madura

MKI-Basic15-Jeff MaduraYoyo Sudaryo

╠²

The document discusses various forms of multinational restructuring by multinational corporations (MNCs), including international acquisitions, divestitures, and alliances. It explains how MNCs value foreign target firms for acquisition using net present value analysis and outlines factors that can cause valuations to vary between MNCs, such as different cash flow estimates, exchange rate effects, and required rates of return. It also discusses other methods of multinational restructuring like partial acquisitions and privatized business acquisitions.Basic15

Basic15Abraish Georgeous

╠²

This chapter discusses various forms of multinational restructuring that multinational corporations undertake, including international acquisitions, divestitures, alliances, and shifting production among subsidiaries. It explains how MNCs evaluate and value potential foreign acquisition targets, which can vary depending on estimated cash flows, exchange rates, and required rates of return. The chapter also covers other methods of multinational restructuring such as partial acquisitions and privatized businesses, and treats restructuring decisions as real options problems.CHAPTER 18 Multinational Capital Budgeting and Cross-Border Acquis.docx

CHAPTER 18 Multinational Capital Budgeting and Cross-Border Acquis.docxcravennichole326

╠²

CHAPTER 18 Multinational Capital Budgeting and Cross-Border Acquisitions

When it comes to finances, remember that there are no withholding taxes on the wages of sin.

ŌĆöMae West (1892ŌĆō1980), Mae West on Sex, Health and ESP, 1975.

LEARNING OBJECTIVES

Ō¢ĀExtend the domestic capital budgeting analysis to evaluate a greenfield foreign project

Ō¢ĀDistinguish between the project viewpoint and the parent viewpoint of a potential foreign investment

Ō¢ĀAdjust the capital budgeting analysis of a foreign project for risk

Ō¢ĀExamine the use of project finance to fund and evaluate large global projects

Ō¢ĀIntroduce the principles of cross-border mergers and acquisitions

This chapter describes in detail the issues and principles related to the investment in real productive assets in foreign countries, generally referred to as multinational capital budgeting. The chapter first describes the complexities of budgeting for a foreign project. Second, we describe the insights gained by valuing a project from both the projectŌĆÖs viewpoint and the parentŌĆÖs viewpoint using an illustrative case involving an investment by Cemex of Mexico in Indonesia. This illustrative case also explores real option analysis. Next, the use of project financing today is discussed, and the final section describes the stages involved in affecting cross-border acquisitions. The chapter concludes with the Mini-Case, Elan and Royalty Pharma, about a hostile takeover (acquisition) attempt that played out in the summer of 2013.

Although the original decision to undertake an investment in a particular foreign country may be determined by a mix of strategic, behavioral, and economic factors, the specific project should be justifiedŌĆöas should all reinvestment decisionsŌĆöby traditional financial analysis. For example, a production efficiency opportunity may exist for a U.S. firm to invest abroad, but the type of plant, mix of labor and capital, kinds of equipment, method of financing, and other project variables must be analyzed with traditional discounted cash flow analysis. The firm must also consider the impact of the proposed foreign project on consolidated earnings, cash flows from subsidiaries in other countries, and on the market value of the parent firm.

Multinational capital budgeting for a foreign project uses the same theoretical framework as domestic capital budgetingŌĆöwith a few very important differences. The basic steps are as follows:

Ō¢ĀIdentify the initial capital invested or put at risk.

Ō¢ĀEstimate cash flows to be derived from the project over time, including an estimate of the terminal or salvage value of the investment.

Ō¢ĀIdentify the appropriate discount rate for determining the present value of the expected cash flows.

Ō¢ĀUse traditional capital budgeting methods, such as net present value (NPV) and internal rate of return (IRR), to assess and rank potential projects.

Complexities of Budgeting for a Foreign Project

Capital budgeting for a foreign project is considerably more complex than the ...Foreigninvestment

ForeigninvestmentStudsPlanet.com

╠²

Japanese firms rely more heavily on bank financing and internal cash flows, while U.S. firms rely more on external financing through public debt and equity markets. This difference stems from Japan's main bank system where long-term relationships between firms and banks facilitate internal financing, compared to the U.S. where arm's-length capital markets play a larger role in corporate financing. As financial systems globalize, the differences in financing practices between countries have narrowed to some degree.International BusinessPresentation(By;Zaman).pptx

International BusinessPresentation(By;Zaman).pptxzaman raza

╠²

This document discusses risks in international business and factors that influence capital structure decisions for multinational corporations. It begins by outlining various risks like political, regulatory, economic, currency, and cultural risks that companies face when doing business abroad. It then examines methods for valuing capital projects, including payback period, internal rate of return, and net present value. Finally, it analyzes how company characteristics like cash flow stability and credit risk as well as country characteristics like tax laws and currency values influence an MNC's capital structure decisions.Mn cs cost of capital

Mn cs cost of capitalWalid Saafan

╠²

The document discusses the capital structure decisions of multinational firms (MNCs). It explains that MNCs consider both corporate characteristics, such as cash flow stability and access to retained earnings, and country characteristics, such as interest rates and tax laws, when determining the capital structure of their subsidiaries. The overall capital structure of an MNC combines the structures of the parent company and its subsidiaries. A subsidiary's debt financing decisions can impact the level of internal funds available to the parent company.Foreign Direct Investment

Foreign Direct Investmentnauman mustafa

╠²

This document provides an overview of foreign direct investment (FDI). It defines FDI as when a firm directly invests in facilities in a foreign country to produce or market goods, making the firm multinational. FDI can take the form of building new facilities or acquiring existing companies. The document discusses theories and strategic motivations for FDI, including accessing resources, serving new markets, improving efficiency, and strategic asset seeking. FDI is described as providing benefits like exploiting location and ownership advantages, improving performance through structural differences between countries, and enabling organizational learning.Answers concept questions_14-32

Answers concept questions_14-32mudey001

╠²

- The document contains concept questions and answers related to corporate finance topics like capital structure, dividend policy, and market efficiency.

- It discusses key concepts such as the efficient market hypothesis, agency costs, bankruptcy costs, and the tradeoff between debt and equity financing.

- The questions assess understanding of valuation models like APV and WACC, as well as theories including MM propositions, pecking order theory, and the irrelevance of dividends under perfect market conditions.97044413 international-financial-management-11

97044413 international-financial-management-11Tinku Kumar

╠²

This document discusses considerations for multinational capital budgeting. It compares capital budgeting analyses from the perspective of a parent company versus a subsidiary and identifies factors that create differences in their cash flows, such as taxes, regulations on transferring funds, and exchange rate movements. The document also outlines inputs needed for multinational capital budgeting analyses and methods for assessing risk.Eun_9e_International_Financial_Management_PPT_CH13.pptx

Eun_9e_International_Financial_Management_PPT_CH13.pptxPujaChakraborty27

╠²

The document discusses international equity markets. It provides statistics on market capitalization, liquidity, and concentration of major stock exchanges in 2018. It describes how secondary markets allow for trading of shares and outlines different market structures. It discusses factors that drove greater global integration of capital markets in the 1980s and describes cross-listing of shares, Yankee stock offerings, and American Depository Receipts. It also summarizes empirical findings on cross-listings and provides an overview of international equity market benchmarks and iShares MSCI funds. In closing, it outlines macroeconomic factors, exchange rates, and industrial structure that can influence international equity returns.Details on cost of capital method cost of capital method.ppt

Details on cost of capital method cost of capital method.pptKhalid Eldabbagh

╠²

cost of capital methodForeigninvestment

ForeigninvestmentStudsPlanet.com

╠²

This document discusses various methods for analyzing foreign direct investment and determining the appropriate discount rates for foreign projects. It addresses calculating net present value from both the subsidiary and parent company's perspectives. Additionally, it covers incorporating political and economic risks, using three stage approaches, and estimating costs of capital and betas for foreign investments using domestic proxy firms and accounting for country-specific risk. Key considerations discussed include sources of higher returns from foreign direct investment, factors influencing locations of multinational investment, and challenges in estimating cash flows, cannibalization, and intangible benefits.Foreigninvestment

ForeigninvestmentNits Kedia

╠²

The document discusses several topics related to foreign investment analysis and capital budgeting for multinational corporations. It covers two methods of international capital budgeting, the significance of segmented capital markets, and issues related to the cost of capital for foreign investments. It also addresses difficulties in estimating cash flows for foreign projects, political and economic risk analysis, and three approaches to analyzing foreign investments.basic01 International Financial Managemant.ppt

basic01 International Financial Managemant.pptMuhammadUsmanYusuf1

╠²

This document summarizes chapter 1 of the textbook "International Financial Management" by Jeff Madura. The chapter discusses the goal of multinational corporations to maximize shareholder wealth and conflicts against this goal. It also outlines theories justifying international business and common methods used, such as international trade, licensing, and establishing foreign subsidiaries. The chapter reviews opportunities and risks of international operations and how multinational corporations can manage their value through financial decisions.

IFE.pptx

IFE.pptxAhutiMishra3

╠²

This document discusses the goals and operations of multinational corporations (MNCs). It begins by stating the main goal of MNCs is to maximize shareholder wealth, but there can be conflicts with foreign managers having different goals. It then covers some key theories for international business expansion, including comparative advantage and product life cycles. Different methods for conducting international business are also outlined, such as exporting, licensing, franchising, joint ventures, acquisitions, and foreign direct investment through new subsidiaries. The document closes by discussing how MNCs manage risks associated with international operations like exchange rate fluctuations and exposure to foreign economic and political conditions.MKI_Basic13

MKI_Basic13Yoyo Sudaryo

╠²

The document discusses direct foreign investment (DFI) by multinational corporations. It outlines common motives for DFI such as accessing new markets, using cheaper foreign factors of production, and diversifying internationally. The benefits of international diversification for firms are presented, including lower risk from reduced correlations between foreign projects. Governments may provide incentives for desired DFI and impose barriers on less desired forms through regulations and policies.Writing a 15 pages final paper, will be discussed in our 1st╠²meeti.docx

Writing a 15 pages final paper, will be discussed in our 1st╠²meeti.docxambersalomon88660

╠²

Writing a 15 pages final paper, will be discussed in our 1st╠²meeting.

The final Paper and PowerPoint Presentation: Topic AnalysisŌĆō 15 to 20 pages in APA format

Choose a topic in IT Project Management for your topic analysis. Email to your instructor a proposal of the topic area you intend to use for your topic analysis. Prepare a summary that identifies the major research threads in your topic. A reference list should be included in the summary. The topic should be relevant to your course material.

The professor will approve the topic of the project during the time when the class meets. E-mail the professor by week 2 with the topic for your final project. Email the professor a draft reference list by week 5. The Final Project will be a research report relevant to the selected topic. Your report will include an evolution of the chosen topic, the problems resolved or will be resolved, and future trends.╠²The paper should have 5-7 academic references for each of these areas (published articles and/or textbook.╠²The paper should be 15 to 20 pages in length and must be presented in the APA style, and is due during the last week of classes.

CHAPTER 14 Raising Equity and Debt Globally

Do what you will, the capital is at hazard. All that can be required of a trustee to invest, is, that he shall conduct himself faithfully and exercise a sound discretion. He is to observe how men of prudence, discretion, and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent disposition of their funds, considering the probable income, as well as the probable safety of the capital to be invested.

ŌĆöPrudent Man Rule, Justice Samuel Putnam, 1830.

LEARNING OBJECTIVES

Ō¢ĀDesign a strategy to source capital equity globally

Ō¢ĀExamine the potential differences in the optimal financial structure of the multinational firm compared to that of the domestic firm

Ō¢ĀDescribe the various financial instruments that can be used to source equity in the global equity markets

Ō¢ĀUnderstand the different forms of foreign listingsŌĆödepositary receiptsŌĆöin U.S. markets

Ō¢ĀAnalyze the unique role private placement enjoys in raising global capital

Ō¢ĀEvaluate the different goals and considerations relevant to a firm pursuing foreign equity listing and issuance

Ō¢ĀExplore the different structures that can be used to source debt globally

Chapter 13 analyzed why gaining access to global capital markets should lower a firmŌĆÖs cost of capital, increase its access to capital, and improve the liquidity of its shares by overcoming market segmentation. A firm pursuing this lofty goal, particularly a firm from a segmented or emerging market, must first design a financial strategy that will attract international investors. This involves choosing among alternative paths to access global capital markets.

This chapter focuses on firms that reside in less liquid, segmented, or emerging markets. They are the ones that need to tap liquid and unsegmented markets in order to attain.Ifm6

Ifm6StudsPlanet.com

╠²

This chapter discusses the cost of capital and capital structure for multinational corporations (MNCs). It explains that an MNC's cost of capital may differ from domestic firms due to its size, access to international capital markets, diversification across countries, and exposure to exchange rate and country risks. The capital asset pricing model is used to assess how required rates of return differ between MNCs and domestic firms. Additionally, both corporate characteristics and country characteristics influence an MNC's optimal capital structure decision.International Financial management Chapter 2 for MBM.pptx

International Financial management Chapter 2 for MBM.pptxbibornomohin1987

╠²

║▌║▌▀ŻShare a Scribd company logo

Search

Submit Search

7. International Arbitrage And Interest Rate Parity.pptx

Upload a presentation to download

7. International Arbitrage And Interest Rate Parity.pptx

Add more information to your upload

Better titles and descriptions lead to more readers

International Financial management Chapter 2 for MBM.pptx

Uploading 0.29Mb of 0.29Mb

International Financial management Chapter 2 for MBM.pptx

*Minimum 40 characters required

57/40

*Required

0/3000

Select a category

*Required

Add up to 20 keywords to increase discoverability by 30%

Show Advanced Settings

Discoverability Score

Your score increases as you pick a category, fill out a long description and add more tags.

Upload another presentation

or drag & drop here

or upload from the cloud:

Upload presentationNo file chosen

About

Support

Terms

Privacy

Copyright

Cookie Preferences

FAI-lT .1 Financing the Global FirmCost of Capital (d.docx

FAI-lT .1 Financing the Global FirmCost of Capital (d.docxmydrynan

╠²

FAI-lT .1 Financing the Global Firm

Cost of Capital ('/d

30

28

26

24

20

1B

16

14

12

10

B

6

4

2

The Cost of Capital and Financial Structure

ke = cost of equity

k'vncc = weighted

average after-tax

cost of capital

ka r x) = after-iax

cost of debt

Total Debt (D)

Debt Ratio (o/"\ =

-

Total Assets (V)

Partly offsetting the favorable effect of more debt is an increase in the cost of equity (k"),

because investors perceive greater financial risk. Nevertheless, the overall lveighted average

after-tax cost of capital (kwacc) continues to decline as the debt ratio increases, until finan-

cial risk becomes so serious that investors and management alike pierceive a real danger of

insoivency. This result causes a sharp increase in the cost of new debt and equity, thus increas-

ing the weighted average cost of capital. The lou,point on the resulting U-shaped cost of cap-

ital curve. which is at 14"/" in Exhibit 13.2. defines the debt ratio range in which the cost of

capital is minimized.

Most theorists believe that the low point is actually a rather broad flat area encompass-

ing a wide range of debt ratios, 30% to 60% In Exhibit 13.2, rvhere little difference exists in

the cost of capital. They also believe that, at least in the United States, the range of the flat

area and the location of a particular firm's debt ratio rvithin that range are determined by

such variables as 1) the industry in which it competes;2) volatility of its sales and operating

income; and 3) the collateral value of its assets.

*ptirt:;:l Finasreial Strer*t*r* and the MfdH

The domestic theory of optimal financial structures needs to be modified by four more vari-

ables in order to accommodate the case of the MNE. These variables, in order of appearance,

are 1) availability of capital; 2) diversification of cash flows; 3) foreign exchange risk; and

4) expectations of international portfoiio investors.

Availability of Capital. Chapter 12 demonstrated that access to capital in global markets allows

an MNE to lower its cost of equity and debt compared rvith most domestic firms. It also per-

mits an MNE to maintain its desired debt ratio, even when significant amounts of new funds

must be raised. In other wordq a multinational firm's marginal cost of capital is constant for

considerable ranges of its capital budget. This statement is not true for most small domestic

k").

1ge

an-

'of

ras-

ap-

.of

firms because they do not have access to the national

equity or debt markets' They must either

rely on internally generated funds or borrow for

the short and medium terms from commel-

cial banks. : r ^^-:+-r *^.lzatc are

Multinational firms domiciled in countries that have illiquid

capital markets ale rn

almost the same ,it,ruiion u, small domesri" tlt*t uniess they have

gained a global cost and

availability of capital. They must rely on l"t"t"u!V generated

funds and bank borrowing' If

they need to raise significant u*o,rrrt. of new iunO--t

to finance gr ...BPR: Decode, Segment, and Excel Beyond Success

BPR: Decode, Segment, and Excel Beyond SuccessVipin Srivastava

╠²

In the fast-paced and ever-evolving world of business, staying ahead of the curve requires more than just incremental improvements. Companies must rethink and fundamentally transform their processes to achieve substantial gains in performance. This is where Business Process Reengineering (BPR) comes into play. BPR is a strategic approach that involves the radical redesign of core business processes to achieve dramatic improvements in productivity, efficiency, and quality. By challenging traditional assumptions and eliminating inefficiencies, redundancies, and bottlenecks, BPR enables organizations to streamline operations, reduce costs, and enhance profitability.

For non-performing organizations, BPR serves as a powerful weapon for reinvigoration. By crafting a compelling narrative around the need for change, leaders can inspire and galvanize their teams to embrace the transformation journey. BPR fosters a culture of continuous improvement, innovation, and agility, allowing companies to align their processes with strategic goals and respond swiftly to market trends and customer needs.

Ultimately, BPR leads to substantial performance improvements across various metrics, driving organizations towards renewed purpose and success. Whether it's faster turnaround times, higher-quality outputs, or increased customer satisfaction, the measurable and impactful results of BPR provide a blueprint for sustainable growth and competitive advantage. In a world where change is the only constant, BPR stands as a transformative approach to achieving business excellence.

More Related Content

Similar to Cost of capital structure and international budgeting (20)

Basic15

Basic15Abraish Georgeous

╠²

This chapter discusses various forms of multinational restructuring that multinational corporations undertake, including international acquisitions, divestitures, alliances, and shifting production among subsidiaries. It explains how MNCs evaluate and value potential foreign acquisition targets, which can vary depending on estimated cash flows, exchange rates, and required rates of return. The chapter also covers other methods of multinational restructuring such as partial acquisitions and privatized businesses, and treats restructuring decisions as real options problems.CHAPTER 18 Multinational Capital Budgeting and Cross-Border Acquis.docx

CHAPTER 18 Multinational Capital Budgeting and Cross-Border Acquis.docxcravennichole326

╠²

CHAPTER 18 Multinational Capital Budgeting and Cross-Border Acquisitions

When it comes to finances, remember that there are no withholding taxes on the wages of sin.

ŌĆöMae West (1892ŌĆō1980), Mae West on Sex, Health and ESP, 1975.

LEARNING OBJECTIVES

Ō¢ĀExtend the domestic capital budgeting analysis to evaluate a greenfield foreign project

Ō¢ĀDistinguish between the project viewpoint and the parent viewpoint of a potential foreign investment

Ō¢ĀAdjust the capital budgeting analysis of a foreign project for risk

Ō¢ĀExamine the use of project finance to fund and evaluate large global projects

Ō¢ĀIntroduce the principles of cross-border mergers and acquisitions

This chapter describes in detail the issues and principles related to the investment in real productive assets in foreign countries, generally referred to as multinational capital budgeting. The chapter first describes the complexities of budgeting for a foreign project. Second, we describe the insights gained by valuing a project from both the projectŌĆÖs viewpoint and the parentŌĆÖs viewpoint using an illustrative case involving an investment by Cemex of Mexico in Indonesia. This illustrative case also explores real option analysis. Next, the use of project financing today is discussed, and the final section describes the stages involved in affecting cross-border acquisitions. The chapter concludes with the Mini-Case, Elan and Royalty Pharma, about a hostile takeover (acquisition) attempt that played out in the summer of 2013.

Although the original decision to undertake an investment in a particular foreign country may be determined by a mix of strategic, behavioral, and economic factors, the specific project should be justifiedŌĆöas should all reinvestment decisionsŌĆöby traditional financial analysis. For example, a production efficiency opportunity may exist for a U.S. firm to invest abroad, but the type of plant, mix of labor and capital, kinds of equipment, method of financing, and other project variables must be analyzed with traditional discounted cash flow analysis. The firm must also consider the impact of the proposed foreign project on consolidated earnings, cash flows from subsidiaries in other countries, and on the market value of the parent firm.

Multinational capital budgeting for a foreign project uses the same theoretical framework as domestic capital budgetingŌĆöwith a few very important differences. The basic steps are as follows:

Ō¢ĀIdentify the initial capital invested or put at risk.

Ō¢ĀEstimate cash flows to be derived from the project over time, including an estimate of the terminal or salvage value of the investment.

Ō¢ĀIdentify the appropriate discount rate for determining the present value of the expected cash flows.

Ō¢ĀUse traditional capital budgeting methods, such as net present value (NPV) and internal rate of return (IRR), to assess and rank potential projects.

Complexities of Budgeting for a Foreign Project

Capital budgeting for a foreign project is considerably more complex than the ...Foreigninvestment

ForeigninvestmentStudsPlanet.com

╠²

Japanese firms rely more heavily on bank financing and internal cash flows, while U.S. firms rely more on external financing through public debt and equity markets. This difference stems from Japan's main bank system where long-term relationships between firms and banks facilitate internal financing, compared to the U.S. where arm's-length capital markets play a larger role in corporate financing. As financial systems globalize, the differences in financing practices between countries have narrowed to some degree.International BusinessPresentation(By;Zaman).pptx

International BusinessPresentation(By;Zaman).pptxzaman raza

╠²

This document discusses risks in international business and factors that influence capital structure decisions for multinational corporations. It begins by outlining various risks like political, regulatory, economic, currency, and cultural risks that companies face when doing business abroad. It then examines methods for valuing capital projects, including payback period, internal rate of return, and net present value. Finally, it analyzes how company characteristics like cash flow stability and credit risk as well as country characteristics like tax laws and currency values influence an MNC's capital structure decisions.Mn cs cost of capital

Mn cs cost of capitalWalid Saafan

╠²

The document discusses the capital structure decisions of multinational firms (MNCs). It explains that MNCs consider both corporate characteristics, such as cash flow stability and access to retained earnings, and country characteristics, such as interest rates and tax laws, when determining the capital structure of their subsidiaries. The overall capital structure of an MNC combines the structures of the parent company and its subsidiaries. A subsidiary's debt financing decisions can impact the level of internal funds available to the parent company.Foreign Direct Investment

Foreign Direct Investmentnauman mustafa

╠²

This document provides an overview of foreign direct investment (FDI). It defines FDI as when a firm directly invests in facilities in a foreign country to produce or market goods, making the firm multinational. FDI can take the form of building new facilities or acquiring existing companies. The document discusses theories and strategic motivations for FDI, including accessing resources, serving new markets, improving efficiency, and strategic asset seeking. FDI is described as providing benefits like exploiting location and ownership advantages, improving performance through structural differences between countries, and enabling organizational learning.Answers concept questions_14-32

Answers concept questions_14-32mudey001

╠²

- The document contains concept questions and answers related to corporate finance topics like capital structure, dividend policy, and market efficiency.

- It discusses key concepts such as the efficient market hypothesis, agency costs, bankruptcy costs, and the tradeoff between debt and equity financing.

- The questions assess understanding of valuation models like APV and WACC, as well as theories including MM propositions, pecking order theory, and the irrelevance of dividends under perfect market conditions.97044413 international-financial-management-11

97044413 international-financial-management-11Tinku Kumar

╠²

This document discusses considerations for multinational capital budgeting. It compares capital budgeting analyses from the perspective of a parent company versus a subsidiary and identifies factors that create differences in their cash flows, such as taxes, regulations on transferring funds, and exchange rate movements. The document also outlines inputs needed for multinational capital budgeting analyses and methods for assessing risk.Eun_9e_International_Financial_Management_PPT_CH13.pptx

Eun_9e_International_Financial_Management_PPT_CH13.pptxPujaChakraborty27

╠²

The document discusses international equity markets. It provides statistics on market capitalization, liquidity, and concentration of major stock exchanges in 2018. It describes how secondary markets allow for trading of shares and outlines different market structures. It discusses factors that drove greater global integration of capital markets in the 1980s and describes cross-listing of shares, Yankee stock offerings, and American Depository Receipts. It also summarizes empirical findings on cross-listings and provides an overview of international equity market benchmarks and iShares MSCI funds. In closing, it outlines macroeconomic factors, exchange rates, and industrial structure that can influence international equity returns.Details on cost of capital method cost of capital method.ppt

Details on cost of capital method cost of capital method.pptKhalid Eldabbagh

╠²

cost of capital methodForeigninvestment

ForeigninvestmentStudsPlanet.com

╠²

This document discusses various methods for analyzing foreign direct investment and determining the appropriate discount rates for foreign projects. It addresses calculating net present value from both the subsidiary and parent company's perspectives. Additionally, it covers incorporating political and economic risks, using three stage approaches, and estimating costs of capital and betas for foreign investments using domestic proxy firms and accounting for country-specific risk. Key considerations discussed include sources of higher returns from foreign direct investment, factors influencing locations of multinational investment, and challenges in estimating cash flows, cannibalization, and intangible benefits.Foreigninvestment

ForeigninvestmentNits Kedia

╠²

The document discusses several topics related to foreign investment analysis and capital budgeting for multinational corporations. It covers two methods of international capital budgeting, the significance of segmented capital markets, and issues related to the cost of capital for foreign investments. It also addresses difficulties in estimating cash flows for foreign projects, political and economic risk analysis, and three approaches to analyzing foreign investments.basic01 International Financial Managemant.ppt

basic01 International Financial Managemant.pptMuhammadUsmanYusuf1

╠²

This document summarizes chapter 1 of the textbook "International Financial Management" by Jeff Madura. The chapter discusses the goal of multinational corporations to maximize shareholder wealth and conflicts against this goal. It also outlines theories justifying international business and common methods used, such as international trade, licensing, and establishing foreign subsidiaries. The chapter reviews opportunities and risks of international operations and how multinational corporations can manage their value through financial decisions.IFE.pptx

IFE.pptxAhutiMishra3

╠²

This document discusses the goals and operations of multinational corporations (MNCs). It begins by stating the main goal of MNCs is to maximize shareholder wealth, but there can be conflicts with foreign managers having different goals. It then covers some key theories for international business expansion, including comparative advantage and product life cycles. Different methods for conducting international business are also outlined, such as exporting, licensing, franchising, joint ventures, acquisitions, and foreign direct investment through new subsidiaries. The document closes by discussing how MNCs manage risks associated with international operations like exchange rate fluctuations and exposure to foreign economic and political conditions.MKI_Basic13

MKI_Basic13Yoyo Sudaryo

╠²

The document discusses direct foreign investment (DFI) by multinational corporations. It outlines common motives for DFI such as accessing new markets, using cheaper foreign factors of production, and diversifying internationally. The benefits of international diversification for firms are presented, including lower risk from reduced correlations between foreign projects. Governments may provide incentives for desired DFI and impose barriers on less desired forms through regulations and policies.Writing a 15 pages final paper, will be discussed in our 1st╠²meeti.docx

Writing a 15 pages final paper, will be discussed in our 1st╠²meeti.docxambersalomon88660

╠²

Writing a 15 pages final paper, will be discussed in our 1st╠²meeting.

The final Paper and PowerPoint Presentation: Topic AnalysisŌĆō 15 to 20 pages in APA format

Choose a topic in IT Project Management for your topic analysis. Email to your instructor a proposal of the topic area you intend to use for your topic analysis. Prepare a summary that identifies the major research threads in your topic. A reference list should be included in the summary. The topic should be relevant to your course material.

The professor will approve the topic of the project during the time when the class meets. E-mail the professor by week 2 with the topic for your final project. Email the professor a draft reference list by week 5. The Final Project will be a research report relevant to the selected topic. Your report will include an evolution of the chosen topic, the problems resolved or will be resolved, and future trends.╠²The paper should have 5-7 academic references for each of these areas (published articles and/or textbook.╠²The paper should be 15 to 20 pages in length and must be presented in the APA style, and is due during the last week of classes.

CHAPTER 14 Raising Equity and Debt Globally

Do what you will, the capital is at hazard. All that can be required of a trustee to invest, is, that he shall conduct himself faithfully and exercise a sound discretion. He is to observe how men of prudence, discretion, and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent disposition of their funds, considering the probable income, as well as the probable safety of the capital to be invested.

ŌĆöPrudent Man Rule, Justice Samuel Putnam, 1830.

LEARNING OBJECTIVES

Ō¢ĀDesign a strategy to source capital equity globally

Ō¢ĀExamine the potential differences in the optimal financial structure of the multinational firm compared to that of the domestic firm

Ō¢ĀDescribe the various financial instruments that can be used to source equity in the global equity markets

Ō¢ĀUnderstand the different forms of foreign listingsŌĆödepositary receiptsŌĆöin U.S. markets

Ō¢ĀAnalyze the unique role private placement enjoys in raising global capital

Ō¢ĀEvaluate the different goals and considerations relevant to a firm pursuing foreign equity listing and issuance

Ō¢ĀExplore the different structures that can be used to source debt globally

Chapter 13 analyzed why gaining access to global capital markets should lower a firmŌĆÖs cost of capital, increase its access to capital, and improve the liquidity of its shares by overcoming market segmentation. A firm pursuing this lofty goal, particularly a firm from a segmented or emerging market, must first design a financial strategy that will attract international investors. This involves choosing among alternative paths to access global capital markets.

This chapter focuses on firms that reside in less liquid, segmented, or emerging markets. They are the ones that need to tap liquid and unsegmented markets in order to attain.Ifm6

Ifm6StudsPlanet.com

╠²

This chapter discusses the cost of capital and capital structure for multinational corporations (MNCs). It explains that an MNC's cost of capital may differ from domestic firms due to its size, access to international capital markets, diversification across countries, and exposure to exchange rate and country risks. The capital asset pricing model is used to assess how required rates of return differ between MNCs and domestic firms. Additionally, both corporate characteristics and country characteristics influence an MNC's optimal capital structure decision.International Financial management Chapter 2 for MBM.pptx

International Financial management Chapter 2 for MBM.pptxbibornomohin1987

╠²

║▌║▌▀ŻShare a Scribd company logo

Search

Submit Search

7. International Arbitrage And Interest Rate Parity.pptx

Upload a presentation to download

7. International Arbitrage And Interest Rate Parity.pptx

Add more information to your upload

Better titles and descriptions lead to more readers

International Financial management Chapter 2 for MBM.pptx

Uploading 0.29Mb of 0.29Mb

International Financial management Chapter 2 for MBM.pptx

*Minimum 40 characters required

57/40

*Required

0/3000

Select a category

*Required

Add up to 20 keywords to increase discoverability by 30%

Show Advanced Settings

Discoverability Score

Your score increases as you pick a category, fill out a long description and add more tags.

Upload another presentation

or drag & drop here

or upload from the cloud:

Upload presentationNo file chosen

About

Support

Terms

Privacy

Copyright

Cookie Preferences

FAI-lT .1 Financing the Global FirmCost of Capital (d.docx

FAI-lT .1 Financing the Global FirmCost of Capital (d.docxmydrynan

╠²

FAI-lT .1 Financing the Global Firm

Cost of Capital ('/d

30

28

26

24

20

1B

16

14

12

10

B

6

4

2

The Cost of Capital and Financial Structure

ke = cost of equity

k'vncc = weighted

average after-tax

cost of capital

ka r x) = after-iax

cost of debt

Total Debt (D)

Debt Ratio (o/"\ =

-

Total Assets (V)

Partly offsetting the favorable effect of more debt is an increase in the cost of equity (k"),

because investors perceive greater financial risk. Nevertheless, the overall lveighted average

after-tax cost of capital (kwacc) continues to decline as the debt ratio increases, until finan-

cial risk becomes so serious that investors and management alike pierceive a real danger of

insoivency. This result causes a sharp increase in the cost of new debt and equity, thus increas-

ing the weighted average cost of capital. The lou,point on the resulting U-shaped cost of cap-

ital curve. which is at 14"/" in Exhibit 13.2. defines the debt ratio range in which the cost of

capital is minimized.

Most theorists believe that the low point is actually a rather broad flat area encompass-

ing a wide range of debt ratios, 30% to 60% In Exhibit 13.2, rvhere little difference exists in

the cost of capital. They also believe that, at least in the United States, the range of the flat

area and the location of a particular firm's debt ratio rvithin that range are determined by

such variables as 1) the industry in which it competes;2) volatility of its sales and operating

income; and 3) the collateral value of its assets.

*ptirt:;:l Finasreial Strer*t*r* and the MfdH

The domestic theory of optimal financial structures needs to be modified by four more vari-

ables in order to accommodate the case of the MNE. These variables, in order of appearance,

are 1) availability of capital; 2) diversification of cash flows; 3) foreign exchange risk; and

4) expectations of international portfoiio investors.

Availability of Capital. Chapter 12 demonstrated that access to capital in global markets allows

an MNE to lower its cost of equity and debt compared rvith most domestic firms. It also per-

mits an MNE to maintain its desired debt ratio, even when significant amounts of new funds

must be raised. In other wordq a multinational firm's marginal cost of capital is constant for

considerable ranges of its capital budget. This statement is not true for most small domestic

k").

1ge

an-

'of

ras-

ap-

.of

firms because they do not have access to the national

equity or debt markets' They must either

rely on internally generated funds or borrow for

the short and medium terms from commel-

cial banks. : r ^^-:+-r *^.lzatc are

Multinational firms domiciled in countries that have illiquid

capital markets ale rn

almost the same ,it,ruiion u, small domesri" tlt*t uniess they have

gained a global cost and

availability of capital. They must rely on l"t"t"u!V generated

funds and bank borrowing' If

they need to raise significant u*o,rrrt. of new iunO--t

to finance gr ...Recently uploaded (20)

BPR: Decode, Segment, and Excel Beyond Success

BPR: Decode, Segment, and Excel Beyond SuccessVipin Srivastava

╠²

In the fast-paced and ever-evolving world of business, staying ahead of the curve requires more than just incremental improvements. Companies must rethink and fundamentally transform their processes to achieve substantial gains in performance. This is where Business Process Reengineering (BPR) comes into play. BPR is a strategic approach that involves the radical redesign of core business processes to achieve dramatic improvements in productivity, efficiency, and quality. By challenging traditional assumptions and eliminating inefficiencies, redundancies, and bottlenecks, BPR enables organizations to streamline operations, reduce costs, and enhance profitability.

For non-performing organizations, BPR serves as a powerful weapon for reinvigoration. By crafting a compelling narrative around the need for change, leaders can inspire and galvanize their teams to embrace the transformation journey. BPR fosters a culture of continuous improvement, innovation, and agility, allowing companies to align their processes with strategic goals and respond swiftly to market trends and customer needs.

Ultimately, BPR leads to substantial performance improvements across various metrics, driving organizations towards renewed purpose and success. Whether it's faster turnaround times, higher-quality outputs, or increased customer satisfaction, the measurable and impactful results of BPR provide a blueprint for sustainable growth and competitive advantage. In a world where change is the only constant, BPR stands as a transformative approach to achieving business excellence.

Transfer API | Transfer Booking Engine | Transfer API Integration

Transfer API | Transfer Booking Engine | Transfer API Integrationchethanaraj81

╠²

FlightsLogic is a leading╠²travel technology company╠²offering╠²Transfer API╠²and other services to the travel market. By integrating your travel website with our transfer API, you can take benefit of various international transfer services from airports, hotels, resorts, cars, etc. Our Transfer API comes with full documentation with technical support and it supports both B2C and B2B solutions. With the transfer API solution developed by FlightsLogic, the user can easily book their transport from the airport to the travel place. For more details, pls visit our website: https://www.flightslogic.com/transfer-api.php

Holden Melia - An Accomplished Executive

Holden Melia - An Accomplished ExecutiveHolden Melia

╠²

Holden Melia is an accomplished executive with over 15 years of experience in leadership, business growth, and strategic innovation. He holds a BachelorŌĆÖs degree in Accounting and Finance from the University of Nebraska-Lincoln and has excelled in driving results, team development, and operational efficiency.Ross Chayka: AI in Business: Quo Vadis? (UA)

Ross Chayka: AI in Business: Quo Vadis? (UA)Lviv Startup Club

╠²

Ross Chayka: AI in Business: Quo Vadis? (UA)

Kyiv AI & BigData Day 2025

Website ŌĆō https://aiconf.com.ua/kyiv

Youtube ŌĆō https://www.youtube.com/startuplviv

FB ŌĆō https://www.facebook.com/aiconfSiddhartha Bank Navigating_Nepals_Financial_Challenges.pptx

Siddhartha Bank Navigating_Nepals_Financial_Challenges.pptxSiddhartha Bank

╠²

This PowerPoint presentation provides an overview of NepalŌĆÖs current financial challenges and highlights how Siddhartha Bank supports individuals and businesses. It covers key issues such as inflation and limited credit access while showcasing the bankŌĆÖs solutions, including loan options, savings plans, digital banking services, and customer support. The slides are designed with concise points for clear and effective communication.BusinessGPT - Privacy first AI Platform.pptx

BusinessGPT - Privacy first AI Platform.pptxAGATSoftware

╠²

Empower users with responsible and secure AI for generating insights from your companyŌĆÖs data.ŌĆŗ Usage control and data protection concerns limit companies from leveraging Generative AI.ŌĆŗ For customers that donŌĆÖt want to take any risk of using Public AI services.ŌĆŗ For customers that are willing to use Public AI services but want to manage the risks.ŌĆŗNorman Cooling - Founder And President Of N.L

Norman Cooling - Founder And President Of N.LNorman Cooling

╠²

Norman Cooling founded N.L. Cooling Strategic Consulting LLC where he serves as President. A man of faith and usher for Wesley Memorial Methodist Church, he lives with his wife, Beth, in High Point, North Carolina. Norm is an active volunteer, serving as a Group Leader for Enduring Gratitude since 2019 and volunteering with the Semper Fi Fund.Top Social Media Marketing Trends in 2025

Top Social Media Marketing Trends in 2025bulbulkanwar7070

╠²

Social media marketing trends is now being very crucial.QUALIFIED USDT & BITCOIN RECOVERY EXPERT VIA CRANIX ETHICAL SOLUTIONS HAVEN

QUALIFIED USDT & BITCOIN RECOVERY EXPERT VIA CRANIX ETHICAL SOLUTIONS HAVENpm4066644

╠²

In 2024, I found myself a victim of a cryptocurrency scam, losing $345,000. The sense of loss and frustration was overwhelming, and I was told by many experts that it was highly unlikely to recover such a significant amount. With cryptocurrencyŌĆÖs irreversible transactions and anonymity, I felt like my chances were slim. However, after hearing about CRANIX ETHICAL SOLUTIONS HAVEN from a trusted contact, I decided to give it a try, and IŌĆÖm so glad I did. I'll admit, I was initially cautious. The internet is filled with horror stories of recovery services that end up being scams themselves, so I did my due diligence. After speaking with the team at CRANIX ETHICAL SOLUTIONS HAVEN, I was impressed by their transparency and professionalism. They assured me that, while recovery was difficult, it was not impossible. They explained their approach clearly, detailing how they use advanced tracking tools and legal channels to attempt recovery, and I felt confident moving forward. From the start, the process was smooth. The team kept me updated regularly, explaining each step they were taking. They were upfront about the challenges of recovering cryptocurrency, but never made any unrealistic promises. They set proper expectations from the beginning while assuring me they would do everything possible to recover my assets. Their honest and patient approach gave me the trust I needed. After several months of diligent work on their part, I started seeing results. They managed to trace some of the funds to specific wallets and identified potential points of contact that were crucial in the recovery process. While the process was slow, their persistence paid off, and eventually, a significant portion of my funds was recovered. I can say with confidence that CRANIX ETHICAL SOLUTIONS HAVEN delivered on their promise. While they could not guarantee success at the outset, they showed a level of commitment and expertise that made me believe recovery was possible. Their customer support was top-notch, always available to answer questions and provide updates. There were no unexpected charges beyond the initial fee, and they remained transparent throughout the process. While recovering cryptocurrency is not easy, it is absolutely possible with the right team. If youŌĆÖve found yourself in a similar situation, I highly recommend CRANIX ETHICAL SOLUTIONS HAVEN. They are a legitimate, reliable service that genuinely works to help you recover lost assets. Just remember that patience and realistic expectations are key, but with their help, recovery is indeed╠²achievable.

TELEGRAM: @ cranixethicalsolutionshaven

EMAIL: cranixethicalsolutionshaven @ post . com ╠²OR ╠²info @ cranixethicalsolutionshaven

WHATSAPP: +44 (7460) (622730)¤ö╣ SWOT Analysis: Boutique Consulting Firms in 2025 ¤ö╣

¤ö╣ SWOT Analysis: Boutique Consulting Firms in 2025 ¤ö╣Alexander Simon

╠²

In an era defined by Consulting 5.0, boutique consulting firmsŌĆöpositioned in the Blue OceanŌĆöface both unprecedented opportunities and critical challenges.

Their strengths lie in specialization, agility, and client-centricity, making them key players in delivering high-value, tailored insights. However, limited scale, regulatory constraints, and rising AI-driven competition present significant barriers to growth.

This SWOT analysis explores the internal and external forces shaping the future of boutique consultancies. Unlike Black Ocean firms, which grapple with the innovatorŌĆÖs dilemma, boutiques have the advantage of flexibility and speedŌĆöbut to fully harness Consulting 5.0, they must form strategic alliances with tech firms, PE-backed networks, and expert collectives.

Key Insights:

Ō£ģ Strengths: Agility, deep expertise, and productized offerings

ŌÜĀ’ĖÅ Weaknesses: Brand visibility, reliance on key personnel

¤ÜĆ Opportunities: AI, Web3, and strategic partnerships

Ōøö Threats: Automation, price competition, regulatory challenges

Strategic Imperatives for Boutique Firms:

¤ōī Leverage AI & emerging tech to augment consulting services

¤ōī Build strategic alliances to access resources & scale solutions

¤ōī Strengthen regulatory & compliance expertise to compete in high-value markets

¤ōī Shift from transactional to long-term partnerships for client retention

As Consulting 5.0 reshapes the industry, boutique consultancies must act now to differentiate themselves and secure their future in a rapidly evolving landscape.

¤ÆĪ What do you think? Can boutique firms unlock Consulting 5.0 before Black Ocean giants do?Get Lifetime Access to Premium AI Models with AI IntelliKit's One-Time Purchase

Get Lifetime Access to Premium AI Models with AI IntelliKit's One-Time PurchaseSOFTTECHHUB

╠²

Imagine a tool that brings all the top AI models such as ChatGPT 4.0, Claude, Gemini Pro, LLaMA, Midjourney, and many more under one roof. ThatŌĆÖs exactly what AI IntelliKit does. Designed to replace expensive subscriptions, this toolbox lets you access premium AI tools from a single, user-friendly dashboard. You no longer need to juggle between multiple platforms or pay recurring fees.

Digital Marketing Roadmap - PPT Template and Guide

Digital Marketing Roadmap - PPT Template and GuideAurelien Domont, MBA

╠²

In the ever-evolving landscape of digital marketing, having a well-structured roadmap is essential for achieving success. HereŌĆÖs a comprehensive digital marketing roadmap that outlines key strategies and steps to take your marketing efforts to the next level. It includes 6 components:

1. Branding Guidelines Strategy

2. Website Design and Development

3. Search Engine Optimization (SEO)

4. Pay-Per-Click (PPC) Strategy

5. Social Media Strategy

6. Emailing Strategy

This PowerPoint presentation is only a small preview of our content. For more details, visit www.domontconsulting.com

The Ultimate Startup Guide for First-Time Entrepreneurs by Experienced Entrep...

The Ultimate Startup Guide for First-Time Entrepreneurs by Experienced Entrep...Yasmin Bashirova

╠²

This guide offers practical insights and actionable steps to help new entrepreneurs launch and grow their businesses successfully.Illuminati brotherhood in Uganda call +256789951901/0701593598

Illuminati brotherhood in Uganda call +256789951901/0701593598removed_43fc2846aef7ee8f2a43e6bb3648f7c3

╠²

Illuminati brotherhood in Uganda call +256789951901/0701593598Jatin Mansata - A Leader In Finance And Philanthropy

Jatin Mansata - A Leader In Finance And PhilanthropyJatin Mansata

╠²

Jatin Mansata is a financial markets leader and teacher with a deep commitment to social change. As the CEO and Director of JM Global Equities, heŌĆÖs recognized for his acumen for derivatives and equities. Beyond his professional achievements, Jatin mentors 500 students, empowering them with financial knowledge.REACH OUT TO SALVAGE ASSET RECOVERY TO RECOVER SCAM OR STOLEN CRYPTOCURRENCY

REACH OUT TO SALVAGE ASSET RECOVERY TO RECOVER SCAM OR STOLEN CRYPTOCURRENCYleooscar735

╠²

WEBSITE.......https://salvageassetrecovery.com

TELEGRAM---@Salvageasset

Email...Salvageassetrecovery@alumni.com

WhatsApp+ 1 8 4 7 6 5 4 7 0 9 6

I Thought IŌĆÖd Lost Everything, My Crops, My Savings, My Future! I'm a third-generation farmer, and like most of my family, I have weathered storms, both the literal and economic varieties. Nothing, though, could have prepared me for the flood that swept through my farm and nearly drowned my future. Over the past five years, I had amassed a $120,000 Bitcoin buffer in silence as a hedge against unstable crop prices. It was my shield against poor harvests and market crashes.

And then the flood came. It wasn't rain, it was the wrath of nature. Water flooded into my office, turning documents into pulp and sending my computers floating around like lumber. My hardware wallet, the sole bulwark between me and that $120,000, was submerged in muddy water. When the skies finally cleared, I held the waterlogged device in my hand, praying fervently that it would still work. It didn't.

Panic ensued. The soybeans were ruined, the barn needed to be repaired, and now my electronic savings, the one thing I thought was sacrosanct was gone. I couldn't tell my wife; she had already been up to her knees helping shovel sludge out of our home.

Desperate, I had put it on an agriculture technology site. I had cried and written, praying that someone somewhere would know what to do. A user responded with a username that turned out to be my savior, Salvage Asset Recovery.

I called them the next day, preparing for robot voice or a bait-and-switch sales pitch. But to my surprise, I spoke with human compassion, patience, and understanding. I unloaded my story, and they listened like neighbors calling after a tornado. They worked immediately, using fancy data reconstruction tools I couldn't even understand.

Every day, they updated me in simple terms. I was anxious, but their professionalism calmed me down. On the ninth day, I got the call. They had recovered my wallet. All the Bitcoins were intact. I was so relieved that I nearly kissed my filthy boots.

When they heard about the flooding damage, they even discounted part of their fee. That touched me more than the rain. Salvage Asset Recovery didn't just restore my savings, they restored my trust in people. They are heroes in my book, and thanks to them, my family's future is once again set on stable ground.CRED presentation in entrepreneurship management

CRED presentation in entrepreneurship managementkumarka087

╠²

CRED is an Indian fintech platform that primarily rewards users for making timely credit card payments.Human-Motivation-Theory PPT

Human-Motivation-Theory PPTAddisuAynayehu1

╠²

Outline of Human Motivation

1. Introduction to Human Motivation

Definition of motivation

Importance of understanding motivation

Overview of motivational theories

2. Theories of Motivation

A. Intrinsic vs. Extrinsic Motivation

Definitions and differences

Examples of each type

B. Maslow's Hierarchy of Needs

Overview of the five levels of needs

Application of the theory in real-life scenarios

C. Self-Determination Theory (SDT)

Overview of intrinsic motivation and its three basic psychological needs: autonomy, competence, and relatedness

The impact of SDT on personal growth and well-being

D. Expectancy Theory

Explanation of how expectations influence motivation

Components: expectancy, instrumentality, and valence

E. Goal-Setting Theory

Importance of setting specific and challenging goals

The SMART criteria (Specific, Measurable, Achievable, Relevant, Time-bound)

3. Factors Influencing Motivation

A. Biological Factors

Role of genetics and neurochemistry in motivation

Impact of physical health and well-being

B. Psychological Factors

Personality traits and their influence on motivation

The role of mindset (fixed vs. growth mindset)

C. Social and Environmental Factors

Influence of culture, family, peers, and society on motivation

The impact of the workplace environment and leadership styles

4. Motivation in Different Contexts

A. Education

How motivation affects learning and academic performance

Strategies to enhance student motivation

B. Workplace

Importance of employee motivation for productivity and job satisfaction

Techniques for fostering motivation in the workplace

C. Personal Development

Motivation for self-improvement and personal goals

The role of habits and routines in maintaining motivation

5. Challenges to Motivation

Common obstacles to motivation (e.g., procrastination, fear of failure)

Strategies to overcome motivational challenges

6. Conclusion

Summary of key points

The significance of understanding motivation for personal and societal growth

7. References

A list of academic sources and literature on motivationIlluminati brotherhood in Uganda call +256789951901/0701593598

Illuminati brotherhood in Uganda call +256789951901/0701593598removed_43fc2846aef7ee8f2a43e6bb3648f7c3

╠²

Cost of capital structure and international budgeting

- 2. Fifth Edition International Capital Structure and the Cost of Capital 17-1 KEY TAKEAWAYS ŌĆóCapital structure is how a company funds its overall operations and growth. ŌĆóDebt consists of borrowed money that is due back to the lender, commonly with interest expense. ŌĆóEquity consists of ownership rights in the company, without the need to pay back any investment. ŌĆóThe debt-to-equity (D/E) ratio is useful in determining the riskiness of a company's borrowing practices.

- 3. WHAT IS CAPITAL STRUCTURE? ŌĆó Capital structure is the particular combination of debt and equity used by a company to finance its overall operations and growth. ŌĆó Equity capital arises from ownership shares in a company and claims to its future cash flows and profits. Debt comes in the form of bond issues or loans, while equity may come in the form of common stock, preferred stock, or retained earnings. Short-term debt is also considered to be part of the capital structure.

- 4. COST OF CAPITAL ŌĆó The cost of capital is the minimum rate of return an investment project must generate in order to pay its financing costs. ŌĆó For a levered firm, the financing costs can be represented by the weighted average cost of capital: K = (1 ŌĆō ’ü¼)Kl + ’ü¼(1 ŌĆō t)i 17-3

- 5. WEIGHTED AVERAGE COST OF CAPITAL Where K = weighted average cost of capital Kl = cost of equity capital for a levered firm i = pretax cost of debt ’ü¼ = debt to total market value ratio t = marginal corporate income tax rate K = (1 ŌĆō ’ü¼)Kl + ’ü¼(1 ŌĆō t)i 17-4

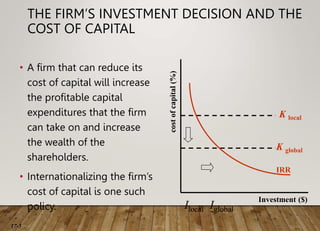

- 6. THE FIRMŌĆÖS INVESTMENT DECISION AND THE COST OF CAPITAL ŌĆó A firm that can reduce its cost of capital will increase the profitable capital expenditures that the firm can take on and increase the wealth of the shareholders. ŌĆó Internationalizing the firmŌĆÖs cost of capital is one such policy. Investment ($) K global K local Ilocal Iglobal IRR 17-5

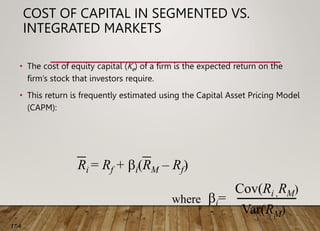

- 7. COST OF CAPITAL IN SEGMENTED VS. INTEGRATED MARKETS ŌĆó The cost of equity capital (Ke) of a firm is the expected return on the firmŌĆÖs stock that investors require. ŌĆó This return is frequently estimated using the Capital Asset Pricing Model (CAPM): where bi= Cov(Ri ,RM) Var(RM) Ri = Rf + bi(RM ŌĆō Rf) 17-6

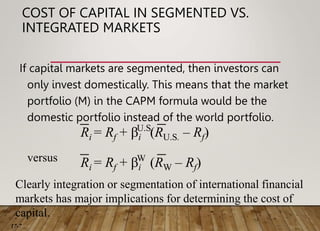

- 8. COST OF CAPITAL IN SEGMENTED VS. INTEGRATED MARKETS If capital markets are segmented, then investors can only invest domestically. This means that the market portfolio (M) in the CAPM formula would be the domestic portfolio instead of the world portfolio. versus Clearly integration or segmentation of international financial markets has major implications for determining the cost of capital. Ri = Rf + bi (RU.S. ŌĆō Rf) U.S. Ri = Rf + bi (RW ŌĆō Rf) W 17-7

- 9. DOES THE COST OF CAPITAL DIFFER AMONG COUNTRIES? ŌĆó There do appear to be differences in the cost of capital in different countries. ŌĆó When markets are imperfect, international financing can lower the firmŌĆÖs cost of capital. ŌĆó One way to achieve this is to internationalize the firmŌĆÖs ownership structure. 17-8

- 10. CROSS-BORDER LISTINGS OF STOCKS ŌĆó Cross-border listings of stocks have become quite popular among major corporations. ŌĆó The largest contingent of foreign stocks are listed on the London Stock Exchange. ŌĆó U.S. exchanges attracted the next largest contingent of foreign stocks. 17-9

- 11. CROSS-BORDER LISTINGS OF STOCKS Cross-border listings of stocks benefit a company in the following ways. 1. The company can expand its potential investor base, which will lead to a higher stock price and lower cost of capital. 2. Cross-listing creates a secondary market for the companyŌĆÖs shares, which facilitates raising new capital in foreign markets. 3. Cross-listing can enhance the liquidity of the companyŌĆÖs stock. 4. Cross-listing enhances the visibility of the companyŌĆÖs name and its products in foreign marketplaces. 17-10

- 12. CROSS-BORDER LISTINGS OF STOCKS Cross-border listings of stocks do carry costs. 1. It can be costly to meet the disclosure and listing requirements imposed by the foreign exchange and regulatory authorities. 2. Once a companyŌĆÖs stock is traded in overseas markets, there can be volatility spillover from these markets. 3. Once a companyŌĆÖs stock is make available to foreigners, they might acquire a controlling interest and challenge the domestic control of the company. 17-11

- 13. CROSS-BORDER LISTINGS OF STOCKS On average, cross-border listings of stocks appears to be a profitable decision. The benefits outweigh the costs. 17-12

- 14. THE EFFECT OF FOREIGN EQUITY OWNERSH RESTRICTIONS ŌĆó While companies have incentives to internationalize their ownership structure to lower the cost of capital and increase market share, they may be concerned with the possible loss of corporate control to foreigners. ŌĆó In some countries, there are legal restrictions on the percentage of a firm that foreigners can own. ŌĆó These restrictions are imposed as a means of ensuring domestic control of local firms. 17-13

- 15. PRICING-TO-MARKET PHENOMENON ŌĆó Suppose foreigners, if allowed, would like to buy 30 percent of a Korean firm. ŌĆó But they are constrained by ownership constraints imposed on foreigners to purchase at most 20 percent. ŌĆó Because this constraint is effective in limiting desired foreign ownership, foreign and domestic investors many face different market share prices. ŌĆó This dual pricing is the pricing-to-market phenomenon. 17-14

- 16. ASSET PRICING UNDER FOREIGN OWNERSHIP RESTRICTIONS ŌĆó An interesting outcome is that the firmŌĆÖs cost of capital depends on which investors, domestic or foreign, supply capital. ŌĆó The implication is that a firm can reduce its cost of capital by internationalizing its ownership structure. 17-15

- 17. THE FINANCIAL STRUCTURE OF SUBSIDIARIES. ŌĆó There are three different approaches to determining the subsidiaryŌĆÖs financial structure. 1. Conform to the parent company's norm. 2. Conform to the local norm of the country where the subsidiary operates. 3. Vary judiciously to capitalize on opportunities to lower taxes, reduce financing costs and risk, and take advantage of various market imperfections. 17-16

- 18. THE FINANCIAL STRUCTURE OF SUBSIDIARIES. ŌĆó In addition to taxes, political risk should be given due consideration in the choice of a subsidiaryŌĆÖs financial structure. 17-17