Erich Baier Präsentation Ubo 2011

- 1. The (too) Famous UBO

- 2. This is just a useless blind obedience or in other words a UBO But letÔÇÿs find out where all that nonsense started The (too) Famous UBO /39

- 3. UBO - the concept of beneficial ownership Term is used in the domestic law of a limited number of countries whose legal systems are based on Beneficial owner common law The meaning of this term has been developed by the courts in these countries Significant factors: the right to enjoy the economic benefits of the underlying property control over the disposition of that property The (too) Famous UBO /39

- 4. In fact the beneficial ownership comes from trust law The basic and simplified concept is that a settlor hands over the assets to a trustee who, on behalf and according to the wishes of the settlor, has to manage these assets But Civil Law does not know the concept of trusts! UBO - the concept of beneficial ownership The (too) Famous UBO /39

- 5. The term beneficial ownership can be seen in contrast to legal ownership Legal ownership refers to more formal attributes such as registration contracts accruals etc In Civil Law the term ÔÇ£beneficial ownershipÔÇ£ could rather be explained with the term economic ownership UBO - the concept of beneficial ownership The (too) Famous UBO /39

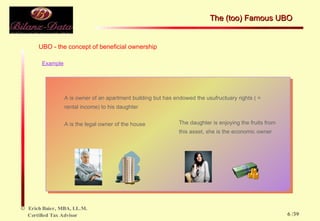

- 6. Example A is owner of an apartment building but has endowed the usufructuary rights ( = rental income) to his daughter A is the legal owner of the house The daughter is enjoying the fruits from this asset, she is the economic owner UBO - the concept of beneficial ownership The (too) Famous UBO /39

- 7. International aspects In an international context the term beneficial ownership is mostly used in connection with tax treaties and of a treaty entitlement in respect of interest dividends royalties The idea behind is clear: anti-avoidance UBO - the concept of beneficial ownership The (too) Famous UBO /39

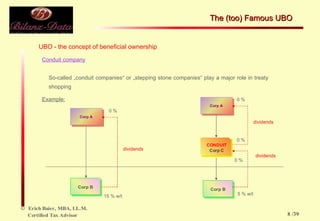

- 8. Conduit company So-called ÔÇ×conduit companiesÔÇ£ or ÔÇ×stepping stone companiesÔÇ£ play a major role in treaty shopping Example: 15 % w/t dividends 0 % dividends 5 % w/t 0 % dividends 0 % 0 % UBO - the concept of beneficial ownership The (too) Famous UBO /39

- 9. Tax treaties now more often contain a limitation on benefits provision which is aiming at the improper use of such a treaty through conduit companies Improper use ? How come ? Is there no one who understood the difference between Common Law and Civil law ? But there is one who understood the difference A judge in Canada UBO - the concept of beneficial ownership The (too) Famous UBO /39

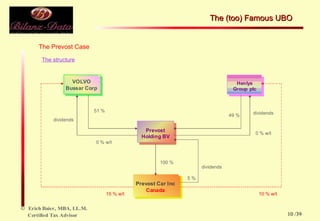

- 10. The Prevost Case The structure 51 % 49 % dividends 0 % w/t 0 % w/t 100 % 15 % w/t dividends dividends 5 % 10 % w/t The (too) Famous UBO /39

- 11. The Prevost Case In 2008 the Tax Court of Canada released the decision in Prevost Car The first case to address the meaning of beneficial ownership for tax purposes in Canada According to the Tax Court of Canada..  a Dutch holding company that received dividends from a Canadian subsidiary was the beneficial owner of the dividends and therefore entitled to the lower rate of withholding tax provided by the Canda  Netherlands tax treaty The (too) Famous UBO /39

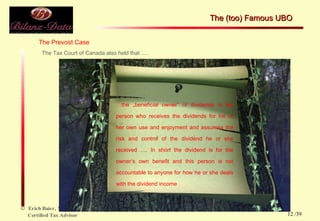

- 12. The Prevost Case The Tax Court of Canada also held that ÔǪ. ÔǪ the ÔÇ×beneficial ownerÔÇ£ of dividends is the person who receives the dividends for his or her own use and enjoyment and assumes the risk and control of the dividend he or she received ÔǪ. In short the dividend is for the ownerÔÇÿs own benefit and this person is not accountable to anyone for how he or she deals with the dividend income The (too) Famous UBO /39

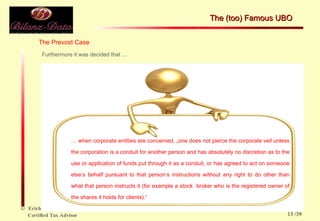

- 13. The Prevost Case Furthermore it was decided that ÔǪ ÔǪ when corporate entities are concerned, ÔÇ×one does not pierce the corporate veil unless the corporation is a conduit for another person and has absolutely no discretion as to the use or application of funds put through it as a conduit, or has agreed to act on someone elseÔÇÿs behalf pursuant to that personÔÇÿs instructions without any right to do other than what that person instructs it (for example a stock broker who is the registered owner of the shares it holds for clients).ÔÇ£ The (too) Famous UBO /39

- 14. The Prevost Case So, excellent news for the taxpayer Time to lean back and relax NO WAY ! The Spanish National Court released a decision in January 2009 which is annoying and confusing The (too) Famous UBO /39

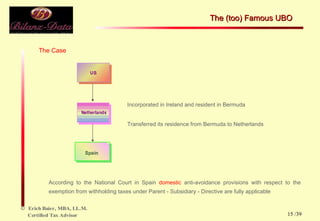

- 15. The Case Incorporated in Ireland and resident in Bermuda Transferred its residence from Bermuda to Netherlands According to the National Court in Spain domestic anti-avoidance provisions with respect to the exemption from withholding taxes under Parent - Subsidiary - Directive are fully applicable The (too) Famous UBO /39

- 16. The Case Because Netherland parent is a mere conduit company. Only very little improvement is added by the NL parent to the R & D activities carried out in the US and Europe Although between 10 and 19 employees worked for the NL parent the National Court disregarded that and considered it irrelevant as the Spanish subsidiaryÔÇÿs accountancy records and management documents were kept in Spain No business purpose could be found for shifting the residence from Bermuda to the NL There was no management support provided by the NL parent to the Spanish subsidiary The (too) Famous UBO /39

- 17. The Case Did I miss something in the development of the EU ? Aren ÔÇÿ t there some basic rules existing ? Does the EU not provide some freedoms ? Among others the freedom of establishment the free movement of capital and payments The (too) Famous UBO /39

- 18. The Case But you are right I should have listened to my teachers The Bermudas do NOT belong to the EU So the Spanish National Court is right, isn ÔÇÿ t it ? Hmm ÔǪ The (too) Famous UBO /39

- 19. The EC Treaty and its impact on taxation Art 56 of the EC treaty includes the principle of free movement of capital and payments Whereas Art 57 ÔÇô 60 set certain limitations on that freedom The (too) Famous UBO /39

- 20. The EC Treaty and its impact on taxation Art 56 of the EC Treaty concerns two relationships the one between two different EU Member States and the one between a EU Member State and a non-Member State The person moving the capital does not need to have the nationality of an EU Member State The (too) Famous UBO /39

- 21. The EC Treaty and its impact on taxation Art 58 of the EC Treaty Art 58 allows, despite of Art 56, a state to implement tax provisions which might restrict the free movement of capital and payments EC Court Measures with the objective of safeguarding the effeciveness of fiscal supervision may be accepted The (too) Famous UBO /39

- 22. The EC Treaty and its impact on taxation Rule of reason There must be a good reason for the provision resulting in indirect discrimination or a restriction on the free movement The free movement of capital may also be restricted if there is an overriding reason in the public interest The (too) Famous UBO /39

- 23. The EC Treaty and its impact on taxation Direct discrimination Always prohibited unless EC Treaty expressly allows it Usually allowed in case of public health public order public security Very seldom relevant in cases concerning direct taxation The (too) Famous UBO /39

- 24. The EC Treaty and its impact on taxation Indirect discrimination Based on EU Court case law on the so-called national tax provisions resulting in rule of reasons principle restrictions on one or more of the basic freedoms may be justified provided such provisions are not applied in a discriminational manner The (too) Famous UBO /39

- 25. The EC Treaty and its impact on taxation Indirect discrimination Such restriction may be justified on the basis of the rule of reasons principle if the restriction has an objective that is in accordance with the EC Treaty and which is justified by an overriding reason in the public interest chewing gum chewing gum chewing gum chewing gum chewing gum chewing gum chewing gum chewing gum The (too) Famous UBO /39

- 26. The EC Treaty and its impact on taxation Indirect discrimination Such tax provisions, nevertheless, are not accepted if there would be a measure available to reach the same objective with a less restrictive manner Accepted reasons safeguarding effectiveness of fiscal supervision anti-avoidance purposes need to prevent a double use of losses (Marks & Spencer) safeguarding fiscal cohesion of the national tax system chewing gum can have different colors ! Chewing gum can have different colors ! chewing gum can have different flavors ! Chewing gum can have different flavors ! The (too) Famous UBO /39

- 27. The EC Treaty and its impact on taxation Indirect discrimination Unaccepted reasons loss of tax revenue (1) non-harmonization of direct taxes EU nationals are free to choose the country for their activities that is the most beneficial from a tax perspective (2) ECJ Cases: (1) C-136/00 Danner and C-422/01 Skandia and Ramstedt (2) C-264/96 ICI, Para. 26, C-364/01 Barbier, C-212/97 Centros, C-167/01 Inspire Art, C-324/00 Lankhorst-Hohorst and C-294/97 Eurowings The (too) Famous UBO /39

- 28. The EC Treaty and its impact on taxation Impact on non-Member States Although Art 56 of the EC Treaty covers both intra-EU situations and situations involving a non- Member State Art 57 of the EC Treaty allows certain restrictions effecting the free movement of capital and payments to and from non - Member States The (too) Famous UBO /39

- 29. The EC Treaty and its impact on taxation Only direct investments This concept of direct investments covers investments of any kind undertaken by natural or legal entitites which serve to establish or maintain lasting and direct links between the person providing the capital and the undertaking to which the capital is made available The (too) Famous UBO /39

- 30. The EC Treaty and its impact on taxation Only direct investments Furthermore it is requested that the shares held by the shareholder enable the shareholder to participate effectively in the management of that company or in its control The (too) Famous UBO /39

- 31. The EC Treaty and its impact on taxation Right to capital in companies Art 294 of the EC Treaty Gives EU nationals the same right to participate in the capital of companies or firms in a Member State as applies to the nationals of that state Relevance Low, Art 56 also entitles to national treatment But  The (too) Famous UBO /39

- 32. The EC Treaty and its impact on taxation Right to capital in companies Art 294 of the EC Treaty applies to all EU nationals Art 294 applies even though the EU national could reside in a non  Member State Therefore  irrespective of their state of residence or of the state of establishment The (too) Famous UBO /39

- 33. The EC Treaty and its impact on taxation Right to capital in companies Art 294 of the EC Treaty the limitations included in Art 57, which are applicable to non ÔÇô Member States cannot be applied to EU nationals residing outside the EU and who have invested capital in companies in the EU Member States The (too) Famous UBO /39

- 34. The EC Treaty and its impact on taxation For a better understanding the following example: Marco, an Italian, lives in Moscow and holds shares in a French corporation Without doubt Art 294 of the EU Treaty applies (EU national, resident outside of the EU, holds shares in a EU corporation) And without doubt the dividends distributed to him by the French corporation are due to a withholding tax at source The rate is 15 % according to the French ÔÇô Russian tax treaty The (too) Famous UBO /39

- 35. During his holidays he falls in love with a beautiful lady from the Czech Republic The EC Treaty and its impact on taxation He follows her to her hometown Prague and establishes his residence in that beautiful city Now the tax treaty between France and the Czech Republic is governing the tax treatment of this dividend income Treaty rate of withholding taxes: 10 % (instead of 15 % as with Russia) The (too) Famous UBO /39

- 36. The EC Treaty and its impact on taxation Can anyone please be so kind to explain to me the difference between the situation Marco, the Italian in love, born in Italy, resident in Moscow and then in Prague, is in and a company incorporated in Ireland, being a legal person with EU nationality, first resident in a third country (Bermudas) and then returning to the EU, taking up its residence in the NL ? The (too) Famous UBO /39

- 37. The EC Treaty and its impact on taxation How can it be that a court in an EU Member State does not apply those regulations which are laid down in the EC Treaty does not recognize that usually a shareholder is not involved in the management and therefore cannot support the management considers it irrelevant that a shareholder obvioulsy has control over the company and can give guidelines to the management in form of a shareholder ÔÇÿ s resolution considers the basic freedom of movement within the EU as treaty-shopping The (too) Famous UBO /39

- 38. THANK YOU FOR YOUR ATTENTION ! The (too) Famous UBO /39

- 39. /39 The (too) Famous UBO