Fighting Predatory Lending In Wash

- 1. Fighting Predatory Lending in Washington: State Law Theories Eric Dunn Northwest Justice Project Seattle University School of Law March 18-19, 2008

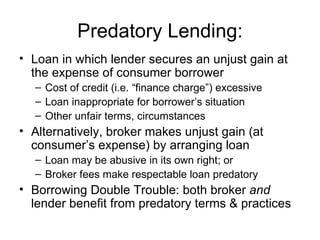

- 2. Predatory Lending: Loan in which lender secures an unjust gain at the expense of consumer borrower Cost of credit (i.e. “finance charge”) excessive Loan inappropriate for borrower’s situation Other unfair terms, circumstances Alternatively, broker makes unjust gain (at consumer’s expense) by arranging loan Loan may be abusive in its own right; or Broker fees make respectable loan predatory Borrowing Double Trouble: both broker and lender benefit from predatory terms & practices

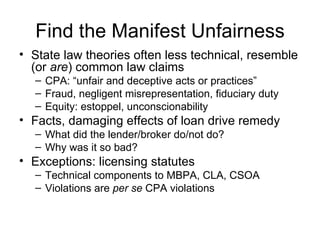

- 3. Find the Manifest Unfairness State law theories often less technical, resemble (or are ) common law claims CPA: “unfair and deceptive acts or practices” Fraud, negligent misrepresentation, fiduciary duty Equity: estoppel, unconscionability Facts, damaging effects of loan drive remedy What did the lender/broker do/not do? Why was it so bad? Exceptions: licensing statutes Technical components to MBPA, CLA, CSOA Violations are per se CPA violations

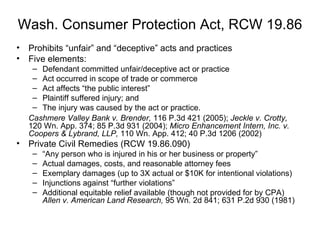

- 4. Wash. Consumer Protection Act, RCW 19.86 Prohibits “unfair” and “deceptive” acts and practices Five elements: Defendant committed unfair/deceptive act or practice Act occurred in scope of trade or commerce Act affects “the public interest” Plaintiff suffered injury; and The injury was caused by the act or practice. Cashmere Valley Bank v. Brender, 116 P.3d 421 (2005); Jeckle v. Crotty, 120 Wn. App. 374; 85 P.3d 931 (2004); Micro Enhancement Intern, Inc. v. Coopers & Lybrand, LLP, 110 Wn. App. 412; 40 P.3d 1206 (2002) Private Civil Remedies (RCW 19.86.090) “ Any person who is injured in his or her business or property” Actual damages, costs, and reasonable attorney fees Exemplary damages (up to 3X actual or $10K for intentional violations) Injunctions against “further violations” Additional equitable relief available (though not provided for by CPA) Allen v. American Land Research, 95 Wn. 2d 841; 631 P.2d 930 (1981)

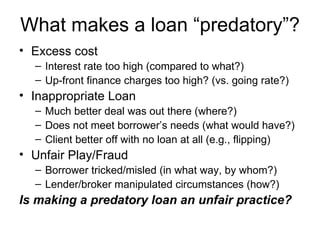

- 5. What makes a loan “predatory”? Excess cost Interest rate too high (compared to what?) Up-front finance charges too high? (vs. going rate?) Inappropriate Loan Much better deal was out there (where?) Does not meet borrower’s needs (what would have?) Client better off with no loan at all (e.g., flipping) Unfair Play/Fraud Borrower tricked/misled (in what way, by whom?) Lender/broker manipulated circumstances (how?) Is making a predatory loan an unfair practice?

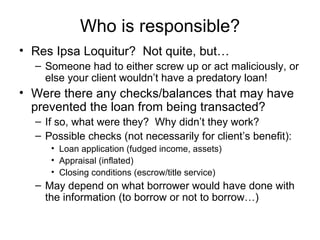

- 6. Who is responsible? Res Ipsa Loquitur? Not quite, but… Someone had to either screw up or act maliciously, or else your client wouldn’t have a predatory loan! Were there any checks/balances that may have prevented the loan from being transacted? If so, what were they? Why didn’t they work? Possible checks (not necessarily for client’s benefit): Loan application (fudged income, assets) Appraisal (inflated) Closing conditions (escrow/title service) May depend on what borrower would have done with the information (to borrow or not to borrow…)

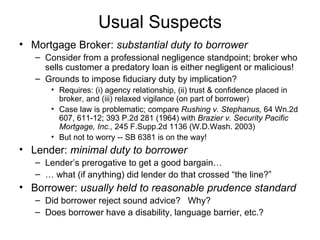

- 7. Usual Suspects Mortgage Broker: substantial duty to borrower Consider from a professional negligence standpoint; broker who sells customer a predatory loan is either negligent or malicious! Grounds to impose fiduciary duty by implication? Requires: (i) agency relationship, (ii) trust & confidence placed in broker, and (iii) relaxed vigilance (on part of borrower) Case law is problematic; compare Rushing v. Stephanus, 64 Wn.2d 607, 611-12; 393 P.2d 281 (1964) with Brazier v. Security Pacific Mortgage, Inc., 245 F.Supp.2d 1136 (W.D.Wash. 2003) But not to worry -- SB 6381 is on the way! Lender: minimal duty to borrower Lender’s prerogative to get a good bargain… … what (if anything) did lender do that crossed “the line?” Borrower: usually held to reasonable prudence standard Did borrower reject sound advice? Why? Does borrower have a disability, language barrier, etc.?

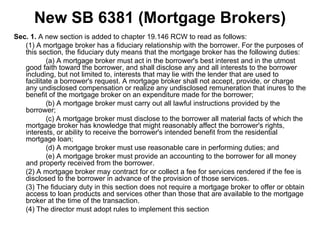

- 8. New SB 6381 (Mortgage Brokers) Sec. 1. A new section is added to chapter 19.146 RCW to read as follows: (1) A mortgage broker has a fiduciary relationship with the borrower. For the purposes of this section, the fiduciary duty means that the mortgage broker has the following duties: (a) A mortgage broker must act in the borrower's best interest and in the utmost good faith toward the borrower, and shall disclose any and all interests to the borrower including, but not limited to, interests that may lie with the lender that are used to facilitate a borrower's request. A mortgage broker shall not accept, provide, or charge any undisclosed compensation or realize any undisclosed remuneration that inures to the benefit of the mortgage broker on an expenditure made for the borrower; (b) A mortgage broker must carry out all lawful instructions provided by the borrower; (c) A mortgage broker must disclose to the borrower all material facts of which the mortgage broker has knowledge that might reasonably affect the borrower's rights, interests, or ability to receive the borrower's intended benefit from the residential mortgage loan; (d) A mortgage broker must use reasonable care in performing duties; and (e) A mortgage broker must provide an accounting to the borrower for all money and property received from the borrower. (2) A mortgage broker may contract for or collect a fee for services rendered if the fee is disclosed to the borrower in advance of the provision of those services. (3) The fiduciary duty in this section does not require a mortgage broker to offer or obtain access to loan products and services other than those that are available to the mortgage broker at the time of the transaction. (4) The director must adopt rules to implement this section

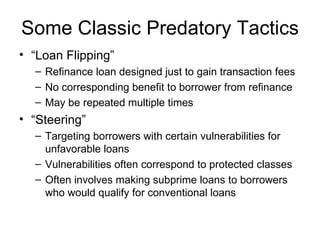

- 9. Some Classic Predatory Tactics “ Loan Flipping” Refinance loan designed just to gain transaction fees No corresponding benefit to borrower from refinance May be repeated multiple times “ Steering” Targeting borrowers with certain vulnerabilities for unfavorable loans Vulnerabilities often correspond to protected classes Often involves making subprime loans to borrowers who would qualify for conventional loans

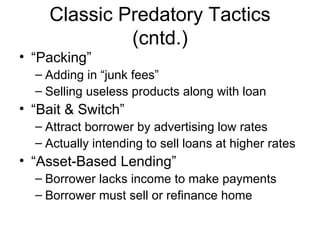

- 10. “Packing” Adding in “junk fees” Selling useless products along with loan “Bait & Switch” Attract borrower by advertising low rates Actually intending to sell loans at higher rates “Asset-Based Lending” Borrower lacks income to make payments Borrower must sell or refinance home Classic Predatory Tactics (cntd.)

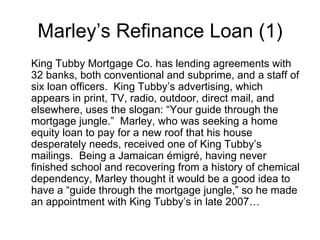

- 11. Marley’s Refinance Loan (1) King Tubby Mortgage Co. has lending agreements with 32 banks, both conventional and subprime, and a staff of six loan officers. King Tubby’s advertising, which appears in print, TV, radio, outdoor, direct mail, and elsewhere, uses the slogan: “Your guide through the mortgage jungle.” Marley, who was seeking a home equity loan to pay for a new roof that his house desperately needs, received one of King Tubby’s mailings. Being a Jamaican émigré, having never finished school and recovering from a history of chemical dependency, Marley thought it would be a good idea to have a “guide through the mortgage jungle,” so he made an appointment with King Tubby’s in late 2007…

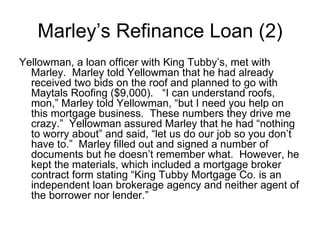

- 12. Yellowman, a loan officer with King Tubby’s, met with Marley. Marley told Yellowman that he had already received two bids on the roof and planned to go with Maytals Roofing ($9,000). “I can understand roofs, mon,” Marley told Yellowman, “but I need you help on this mortgage business. These numbers they drive me crazy.” Yellowman assured Marley that he had “nothing to worry about” and said, “let us do our job so you don’t have to.” Marley filled out and signed a number of documents but he doesn’t remember what. However, he kept the materials, which included a mortgage broker contract form stating “King Tubby Mortgage Co. is an independent loan brokerage agency and neither agent of the borrower nor lender.” Marley’s Refinance Loan (2)

- 13. Marley bought the house in 1992 for $140,000, and thought it was now worth about $200,000 – but three days later, an appraisal by Uhuru estimated the value at $250,000. Marley, who makes $2,500 per month at Wailer Co., has been paying $820/mo. on the same 30-year fixed mortgage since purchase, and the balance on the note (originally $125,000) dipped just under $90,000 by the time of the phone call. Marley has good credit (FICO score is over 700) and no other significant debts besides the mortgage. Marley’s Refinance Loan (3)

- 14. A couple days later, Yellowman informed Marley that he had found “the perfect loan” for Marley, and directed him to appear at a “signing appointment” later that week. “You’ll get your cash for the roof and a new, lower rate,” Yellowman said, “I think you’ll be very happy with it.” Yellowman stated that he would be dropping off some paperwork later that same day, which turned out to be the TILA disclosure statement. Marley thanked Yellowman, and said, “I trust you with this mon. If you say this the best deal I can get, then this the loan I take.” Yellowman did not reply to this remark Marley’s Refinance Loan (4)

- 15. Later that week, Marley signed an adjustable rate note on a $160,000 loan from “Dekker Funding.” The loan has an initial “teaser” rate of 3.6%, so for the two years Marley’s monthly payments would be $727.43. Marley was pleased with these payments, but surprised to receive a check at closing for almost $58,000 in cash. When he returned home, he called Yellowman and asked, “Why so much cash?” Yellowman answered that he thought it was important to take out “a little extra in case the roof wound up costing more.” Marley thought that was a little fishy, so he asked his friend Cliff, who works in a law office, to look over the loan papers. Marley’s heart sank when Cliff explained how, after the initial two year period, Marley’s interest rate would adjust (to LIBOR + 4% margin), which (at present rates) would push Marley’s interest rate over 9%, and monthly payments to over $1,280. “I need a hammer,” Marley said, “to hammer them down.” Marley’s Refinance Loan (5)

Editor's Notes

- #4: Per se CPA violations enforceable under RCW 19.86.090

- #8: Brazier – relied on (i) borrowers signed documents denying that broker was agent and (ii) court found no law requiring broker to get best deal for borrowers (i.e., would not have been a breach if duty existed)

- #11: Single-premium credit insurance used to be the big issue

- #12: What stands out – making Marley a possible target?