TRAVEL TRENDS 2011, presented at USTOA by Forrester

7 likes2,973 views

The document provides insights into the outlook for leisure travel in 2011, emphasizing the need for companies to understand customer behaviors across different generations as they use technology for travel planning. It highlights that despite a majority of travelers booking online, many do not find the process enjoyable or informative, leading to a preference for traditional travel agents. Finally, it notes the growing influence of social media in shaping travel decisions and the importance of appealing to customers' emotional needs alongside rational decision-making.

TRAVEL TRENDS 2011, presented at USTOA by Forrester

- 1. 1 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 2. Prospering In 2011 Henry H. Harteveldt, Vice President, Principal Analyst Twitter: @hharteveldt December 10, 2010 2 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

- 3. We depend on the kindness of strangers but by better understanding our customers and their use of technology, we can be more independent and successful. 3 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited Source: Warner Bros.

- 4. Agenda What is the 2011 outlook for leisure travel? How do different generations of leisure travelers interact with technology to plan and shop for travel online? What affects the decision making of different generations when planning a tripŌĆöand what should you do to succeed? 4 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 5. Agenda What is the 2011 outlook for leisure travel? How do different generations of leisure travelers interact with technology to plan and shop for travel online? What affects the decision making of different generations when planning a tripŌĆöand what should you do to succeed? 5 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 6. Numerous factors can affect economic recovery and consumersŌĆś willingness to travel 6 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited Sources: Google Images

- 7. College grads are twice as likely to be employed as people with only a high-school degree 7 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited Source: Bureau of Labor Statistics

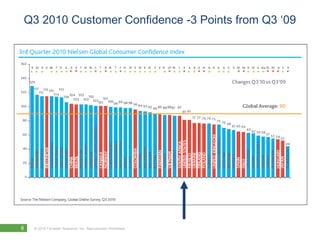

- 8. Q3 2010 Customer Confidence -3 Points from Q3 ŌĆŚ09 8 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

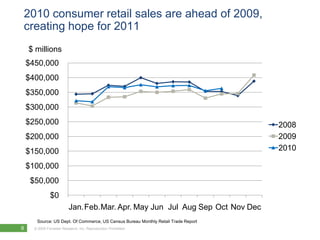

- 9. 2010 consumer retail sales are ahead of 2009, creating hope for 2011 $ millions $450,000 $400,000 $350,000 $300,000 $250,000 2008 $200,000 2009 $150,000 2010 $100,000 $50,000 $0 Jan.Feb.Mar. Apr. May Jun Jul Aug Sep Oct Nov Dec Source: US Dept. Of Commerce, US Census Bureau Monthly Retail Trade Report 9 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

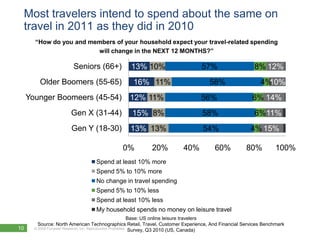

- 10. Most travelers intend to spend about the same on travel in 2011 as they did in 2010 ŌĆ£How do you and members of your household expect your travel-related spending will change in the NEXT 12 MONTHS?ŌĆØ Seniors (66+) 13% 10% 57% 8% 12% Older Boomers (55-65) 16% 11% 58% 4%10% Younger Boomeers (45-54) 12% 11% 56% 6% 14% Gen X (31-44) 15% 8% 58% 6%11% Gen Y (18-30) 13% 13% 54% 4% 15% 0% 20% 40% 60% 80% 100% Spend at least 10% more Spend 5% to 10% more No change in travel spending Spend 5% to 10% less Spend at least 10% less My household spends no money on leisure travel Base: US online leisure travelers Source: North American Technographics Retail, Travel, Customer Experience, And Financial Services Benchmark 10 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited Survey, Q3 2010 (US, Canada) 2010

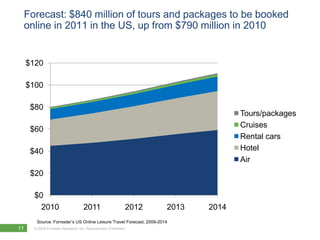

- 11. Forecast: $840 million of tours and packages to be booked online in 2011 in the US, up from $790 million in 2010 $120 $100 $80 Tours/packages Cruises $60 Rental cars $40 Hotel Air $20 $0 2010 2011 2012 2013 2014 Source: ForresterŌĆśs US Online Leisure Travel Forecast, 2009-2014 11 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

- 12. Travelers embrace ŌĆĢneoFrugal ChicŌĆ¢ ’é¦ Saving as a point of pride ’é¦ Every major purchase is heavily researched and considered ’é¦ Travel is a reward, not an entitlement 12 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited Source: Google Images

- 13. Agenda What is the 2011 outlook for leisure travel? How do different generations of leisure travelers interact with technology to plan and shop for travel online? What affects the decision making of different generations when planning a tripŌĆöand what should you do to succeed? 13 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

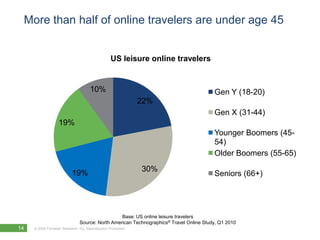

- 14. More than half of online travelers are under age 45 US leisure online travelers 10% Gen Y (18-20) 22% Gen X (31-44) 19% Younger Boomers (45- 54) Older Boomers (55-65) 30% 19% Seniors (66+) Base: US online leisure travelers Source: North American Technographics┬« Travel Online Study, Q1 2010 14 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

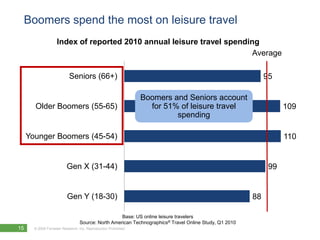

- 15. Boomers spend the most on leisure travel Index of reported 2010 annual leisure travel spending Average Seniors (66+) 95 Boomers and Seniors account Older Boomers (55-65) for 51% of leisure travel 109 spending Younger Boomers (45-54) 110 Gen X (31-44) 99 Gen Y (18-30) 88 Base: US online leisure travelers Source: North American Technographics┬« Travel Online Study, Q1 2010 15 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

- 16. Technology is a means to an end ’é¦ The younger the traveler, the more open they are to technology ’é¦ Travelers may like technology, butŌĆ” ’é¦ Most donŌĆśt see technology as being ŌĆĢimportantŌĆ¢ to them ’é¦ Put customer benefits at the forefront of any technology solution you offer ŌĆō donŌĆśt let technology get in the way 16 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited Source: Google Images

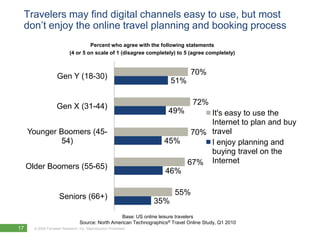

- 17. Travelers may find digital channels easy to use, but most donŌĆśt enjoy the online travel planning and booking process Percent who agree with the following statements (4 or 5 on scale of 1 (disagree completely) to 5 (agree completely) 70% Gen Y (18-30) 51% 72% Gen X (31-44) 49% It's easy to use the Internet to plan and buy Younger Boomers (45- 70% travel 54) 45% I enjoy planning and buying travel on the 67% Internet Older Boomers (55-65) 46% 55% Seniors (66+) 35% Base: US online leisure travelers Source: North American Technographics┬« Travel Online Study, Q1 2010 17 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

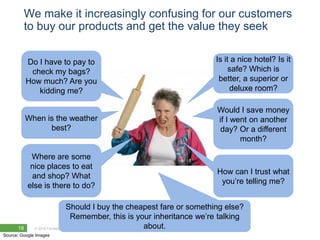

- 18. We make it increasingly confusing for our customers to buy our products and get the value they seek Do I have to pay to Is it a nice hotel? Is it check my bags? safe? Which is How much? Are you better, a superior or kidding me? deluxe room? Would I save money When is the weather if I went on another best? day? Or a different month? Where are some nice places to eat How can I trust what and shop? What youŌĆśre telling me? else is there to do? Should I buy the cheapest fare or something else? Remember, this is your inheritance weŌĆśre talking 18 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited about. Source: Google Images

- 19. Compared to 2008, 22% more US leisure travelers in 2010 would use a travel agent if they could find one Base: US online leisure travelers Source: North American Technographics┬« Travel Online Study, Q1 2010; North American Technographics┬« Travel Online Study, Q1 2008 19 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited Source: Google Images

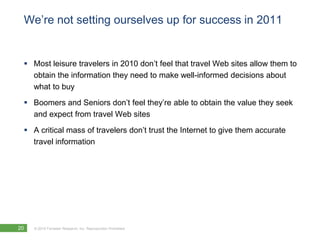

- 20. WeŌĆśre not setting ourselves up for success in 2011 ’é¦ Most leisure travelers in 2010 donŌĆśt feel that travel Web sites allow them to obtain the information they need to make well-informed decisions about what to buy ’é¦ Boomers and Seniors donŌĆśt feel theyŌĆśre able to obtain the value they seek and expect from travel Web sites ’é¦ A critical mass of travelers donŌĆśt trust the Internet to give them accurate travel information 20 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 21. The majority of US online leisure travelers buy at least some portion of their travel online Gen Y (18-30) 70% 14% 16% Gen X (31-44) 75% 14%11% Bookers Younger Boomers (45-54) 73% 14% 13% Lookers Sideliners Older Boomers (55-65) 71% 14% 15% Seniors (66+) 57% 21% 23% Base: US online leisure travelers Source: North American Technographics┬« Travel Online Study, Q1 2010 21 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

- 22. Bookers buy both online and offline, so you need a multichannel selling presence Percent of leisure travel researched and booked online 66% Gen Y (18-30) 72% 71% Gen X (31-44) 76% 71% Book Younger Boomers (45-54) 77% Research 67% Older Boomers (55-65) 73% 65% Seniors (66+) 65% Base: US online leisure Bookers Source: North American Technographics┬« Travel Online Study, Q1 2010 22 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

- 23. No two generations of traveler uses exactly the same mix of channels to research their trips 70% Offline travel agency 60% Call supplier directly 50% Offline travel agency Web site 40% Metasearch site 30% Travel sales & specials site 20% Opaque travel agency site 10% Online travel agency 0% Supplier Web site Gen Y (18- Gen X (31- Younger Older Seniors 30) 44) Boomers Boomers (66+) General search (45-54) (55-65) Base: US online leisure Bookers Source: North American Technographics┬« Travel Online Study, Q1 2010 23 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

- 24. Younger travelers tend to use online intermediaries, older travelers tend to book directly with suppliers 50% 45% 40% Offline travel agency 35% 30% Call supplier directly 25% Offline travel agency Web site 20% Opaque travel agency site 15% 10% Online travel agency 5% Supplier Web site 0% Gen Y (18- Gen X (31- Younger Older Seniors 30) 44) Boomers Boomers (66+) (45-54) (55-65) Base: US online leisure Bookers Source: North American Technographics┬« Travel Online Study, Q1 2010 24 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

- 25. Prepare for new channels and entrants to affect the way you distribute and sell your products 25 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 26. Agenda What is the 2011 outlook for leisure travel? How do different generations of leisure travelers interact with technology to plan and shop for travel online? What affects the decision making of different generations when planning a tripŌĆöand what should you do to succeed? 26 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 27. How we sell When do When do How Where Where you want you want many in are you are you (Etc.) to to your starting? going? leave? return? party? 27 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

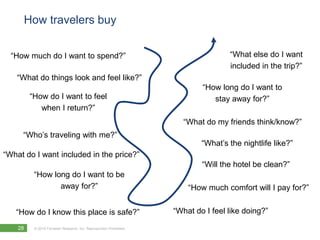

- 28. How travelers buy ŌĆĢHow much do I want to spend?ŌĆ¢ ŌĆĢWhat else do I want included in the trip?ŌĆ¢ ŌĆĢWhat do things look and feel like?ŌĆ¢ ŌĆĢHow long do I want to ŌĆĢHow do I want to feel stay away for?ŌĆ¢ when I return?ŌĆ¢ ŌĆĢWhat do my friends think/know?ŌĆ¢ ŌĆĢWhoŌĆśs traveling with me?ŌĆ¢ ŌĆĢWhatŌĆśs the nightlife like?ŌĆ¢ ŌĆĢWhat do I want included in the price?ŌĆ¢ ŌĆĢWill the hotel be clean?ŌĆ¢ ŌĆĢHow long do I want to be away for?ŌĆ¢ ŌĆĢHow much comfort will I pay for?ŌĆ¢ ŌĆĢHow do I know this place is safe?ŌĆ¢ ŌĆĢWhat do I feel like doing?ŌĆ¢ 28 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 29. WeŌĆśre retailers ŌĆō to prosper, we canŌĆśt push things to our customers, we have to tempt them 29 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited Source: Google Images

- 30. Travelers donŌĆśt always know where they want to go 30 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited Source: Google Images

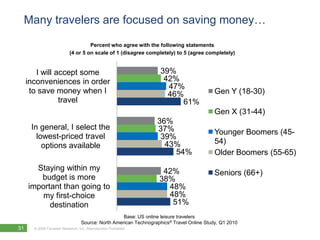

- 31. Many travelers are focused on saving moneyŌĆ” Percent who agree with the following statements (4 or 5 on scale of 1 (disagree completely) to 5 (agree completely) I will accept some 39% inconveniences in order 42% 47% to save money when I 46% Gen Y (18-30) travel 61% Gen X (31-44) 36% In general, I select the 37% Younger Boomers (45- lowest-priced travel 39% 43% 54) options available 54% Older Boomers (55-65) Staying within my 42% Seniors (66+) budget is more 38% important than going to 48% my first-choice 48% destination 51% Base: US online leisure travelers Source: North American Technographics┬« Travel Online Study, Q1 2010 31 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

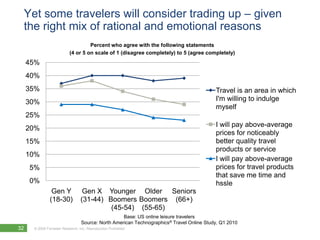

- 32. Yet some travelers will consider trading up ŌĆō given the right mix of rational and emotional reasons Percent who agree with the following statements (4 or 5 on scale of 1 (disagree completely) to 5 (agree completely) 45% 40% 35% Travel is an area in which 30% I'm willing to indulge myself 25% I will pay above-average 20% prices for noticeably 15% better quality travel products or service 10% I will pay above-average 5% prices for travel products that save me time and 0% hssle Gen Y Gen X Younger Older Seniors (18-30) (31-44) Boomers Boomers (66+) (45-54) (55-65) Base: US online leisure travelers Source: North American Technographics┬« Travel Online Study, Q1 2010 32 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

- 33. How to view traveler brand loyalty as we enter 2011 33 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited Source: Google Images

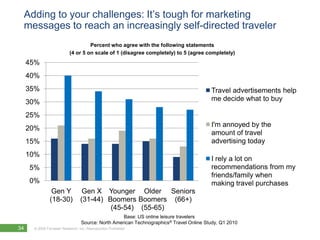

- 34. Adding to your challenges: ItŌĆśs tough for marketing messages to reach an increasingly self-directed traveler Percent who agree with the following statements (4 or 5 on scale of 1 (disagree completely) to 5 (agree completely) 45% 40% 35% Travel advertisements help 30% me decide what to buy 25% I'm annoyed by the 20% amount of travel 15% advertising today 10% I rely a lot on 5% recommendations from my friends/family when 0% making travel purchases Gen Y Gen X Younger Older Seniors (18-30) (31-44) Boomers Boomers (66+) (45-54) (55-65) Base: US online leisure travelers Source: North American Technographics┬« Travel Online Study, Q1 2010 34 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

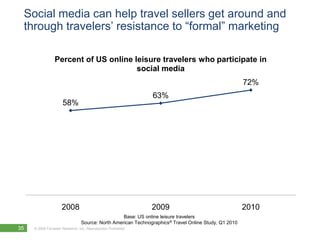

- 35. Social media can help travel sellers get around and through travelersŌĆś resistance to ŌĆĢformalŌĆ¢ marketing Percent of US online leisure travelers who participate in social media 72% 63% 58% 2008 2009 2010 Base: US online leisure travelers Source: North American Technographics┬« Travel Online Study, Q1 2010 35 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

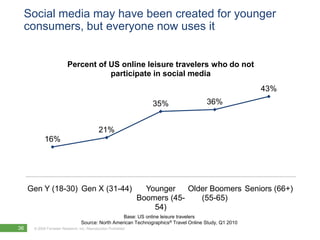

- 36. Social media may have been created for younger consumers, but everyone now uses it Percent of US online leisure travelers who do not participate in social media 43% 35% 36% 21% 16% Gen Y (18-30) Gen X (31-44) Younger Older Boomers Seniors (66+) Boomers (45- (55-65) 54) Base: US online leisure travelers Source: North American Technographics┬« Travel Online Study, Q1 2010 36 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

- 37. 37 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

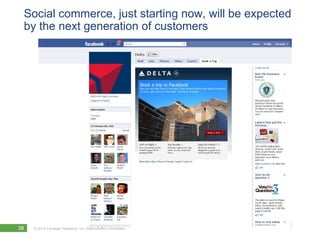

- 38. Social commerce, just starting now, will be expected by the next generation of customers 38 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 39. Video engages travelers of all ages ŌĆō and can lead to more sales Travelers are 3X more likely to watch a brandŌĆśs video than a video posted by another traveler 39 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 40. A typical Smartphone in 2010 has the same amount of computing power as Apollo 11 = 40 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited Source: Google Images

- 41. Devices are evolving ŌĆō itŌĆśs time to rethink mobile 41 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited Source: Google Images

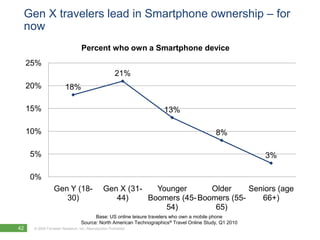

- 42. Gen X travelers lead in Smartphone ownership ŌĆō for now Percent who own a Smartphone device 25% 21% 20% 18% 15% 13% 10% 8% 5% 3% 0% Gen Y (18- Gen X (31- Younger Older Seniors (age 30) 44) Boomers (45- Boomers (55- 66+) 54) 65) Base: US online leisure travelers who own a mobile phone Source: North American Technographics┬« Travel Online Study, Q1 2010 42 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

- 43. Augmented reality overlays on mobile devices will enhance a travelerŌĆÖs journey, and create sponsorship or advertising opportunities for smart travel companies 43 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 44. What should you do to prosper in 2011? 44 ┬® 2009 Forrester Research, Inc. Reproduction Prohibited 2010

- 45. You have multiple opportunities and channels in which to sell ŌĆō create your ŌĆĢstory arcŌĆ¢ Story arc Planning Purchase Departure Trip Return Next Trip 45 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 46. Take steps to make your digital channels as flexible and comprehensive as your offline channels 46 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 47. Create new ways to help travelers find the value you offer 47 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 48. Make it easy for travelers to open their wallets 48 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 49. Make sure you offer the right written and visual content ŌĆō and enable to traveler to configure it to her needs 49 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 50. Let travelers share your content in their social networks 50 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 51. Plan to become mobile-friendly 51 ┬® 2010 Forrester Research, Inc. Reproduction Prohibited

- 52. Thank you Henry H. Harteveldt +1 415.206.0889 hharteveldt@forrester.com Twitter: @hharteveldt www.forrester.com ┬® 2009 Forrester Research, Inc. Reproduction Prohibited