G2 bme roads & highways final

ŌĆóDownload as PPTX, PDFŌĆó

1 likeŌĆó245 views

The Indian roads and highways sector is the second largest road network globally. It bears the maximum passenger and freight traffic of any mode of transport in India. Investments in roads have been rising, with greater private sector involvement. National highways make up only 2% of the total road network but carry 40% of road traffic. The government has launched various initiatives like the National Highways Development Project to expand and upgrade the national highway network through public and private partnerships. Growing vehicle sales and economic activity are driving increased demand for transportation and boosting growth in the roads sector.

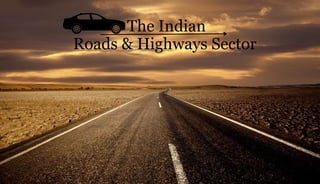

![Sector At A Glance

ŌĆó 2nd largest road network ŌĆō 4.8 million km

ŌĆó Bears maximum passenger (85%) and freight

traffic (60%)

ŌĆó Rising investments

ŌĆó Growing Private Sector Involvement

ŌĆó Rapid growth in NH [100,000 km by 2017]

ŌĆó Overseas Investments

Roads*

Total length : 4.87 Mn km

State Highways National Highways

District and Rural

Roads

ŌĆó 1,46,100 Km

ŌĆó 3.0% of total roads

ŌĆó 97,135 Km

ŌĆó 2.0% of total roads

ŌĆó 46,26,500 Km

ŌĆó 95.0% of total

roads

Source : Ministry of Road Transport and Highways (MoRTH), *As on July 2015

63

3

7

27

Proportion of freight traffic across modes of

transport [2013-14] [In %]

Road

Coastal

Pipeline

Rail

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010-2015 2016-2020

25% 32%

61%

59%

14% 9%

Investments in Roads [In bn]

NH State Rural

4358 8651

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010-2015 2016-2020

35%

56%

65%

44%

Financing of National Highways

Public Private](https://image.slidesharecdn.com/g2bmeroadshighwaysfinal-151116101608-lva1-app6891/85/G2-bme-roads-amp-highways-final-2-320.jpg)

![National Highways

NH ŌĆō 2% of road network, 40% of traffic

NHAI ŌĆō Nodal Agency ŌĆō launched NHDP in

2000

21440 23769

28977

33689

76818 79116

92851

96214

0

20000

40000

60000

80000

100000

120000

Trend in NH Network [km]

1950 1965 1980 1995 2012 2013 2014 2015

NHDP ŌĆōBuilding, Upgradation, rehabilitation &

broadening of existing NH ŌĆō 7 phases

NHDP

Phases

6-laning of

existing NH

NHDP Projects ŌĆō Private Players [EPC Contract /

BOT]

Execution picks up in 2015-16; Nearly 50%

completed

7994 7142 12109 13203

6500

1000

700

48648

7714 6394 6594

1439 2216

- 22

24379

0

10000

20000

30000

40000

50000

60000

Phase I Phase II Phase III Phase IV Phase V Phase VI Phase

VII

Total

Total Length Completed

NHDP ŌĆō Cash contracts ŌĆō Central road fund,

grants, toll revenue

201 234 254 223 185

251

353

516

669

792

NH - Year-wise estimated investment [Rs

Billion]

56%

19%

7%

2%

2% 14%

NHAI Sources of Funds

Cess Toll Premium

External Assistance Budgetary Support Borrowings](https://image.slidesharecdn.com/g2bmeroadshighwaysfinal-151116101608-lva1-app6891/85/G2-bme-roads-amp-highways-final-3-320.jpg)

![State Roads

20% of road network,

40% traffic

SH, MDR, ODR & Rural

Roads

PWD [Cash] & RDC [BOT]

ŌĆō Awards contracts

Central Road Fund ŌĆō By

Central Govt

10%

9%

9%

8%

8%

56%

State-wise budgeted expenditure for the year 2013-14 under CRF

Maharashtra

Rajasthan

Andhra Pradesh

Uttar Pradesh

Madhya Pradesh

Other States

10% [CRF] ŌĆō Devpt of

roads under ISC EI

8%

13%

10%

7%

62%

Total allocations under ISC from 2001-02 to 2011-12

MP Maharashtra Rajasthan Sikkim Other States

7%

7%

7%

7%

10%

7%

55%

Total allocations under EI from 2001-02 to 2011-12

AP Jharkhand Karnataka Nagaland Odisha TN OthersInvestments

380 440

565 623 691

778

879

992

1125

1287

State Roads : Overall Investments [Rs billion]](https://image.slidesharecdn.com/g2bmeroadshighwaysfinal-151116101608-lva1-app6891/85/G2-bme-roads-amp-highways-final-4-320.jpg)

![Top Players Track

21.7 24

9.7

47.1

16.6

4.7

15.1

6

15.8

73

2.4 -2.2 -3.7

12.3

5.7

-5.9

8.6

-18.3

7.5

45

5.7 5.7 6.5

10.5 12.5

2.8

9.5

-1.5

15 15.2

-40

-20

0

20

40

60

80

Ashoka

Buildcon

GMR Hindustan

Construction

Company Ltd

IRB

Infrastrcutre

Developers

Ltd

Larsen &

Toubro

Punj Lloyd

Ltd

Reliance

Infrastructure

Limited

IVRCL

Infrastructre

Projects Ltd

KNR

Constructions

Ltd

Noida Toll

Bridge

Company

Limited

OPM NPM RoCE

Top Companies with exposure to roads sector : Margins & RoCE [In %]](https://image.slidesharecdn.com/g2bmeroadshighwaysfinal-151116101608-lva1-app6891/85/G2-bme-roads-amp-highways-final-6-320.jpg)

![Growth Drivers

1.2 1.3 1.3

1.6

1.8

2.4

3 3.1 3.2 3.1 3.2

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Trends in passenger vehicle sales [In million]

567.6

760.7

929.1

832.6

699 697.1

FY10 FY11 FY12 FY13 FY14 FY15

Trends in commercial vehicle sales [In 000's]

’é¦ Reduce delays

’é¦ Proper Maintenance

’é¦ Transparency

’é¦ Improves investor

confidence

’é¦ Investments to rise

gradually](https://image.slidesharecdn.com/g2bmeroadshighwaysfinal-151116101608-lva1-app6891/85/G2-bme-roads-amp-highways-final-8-320.jpg)

G2 bme roads & highways final

- 1. Roads & Highways Sector The Indian

- 2. Sector At A Glance ŌĆó 2nd largest road network ŌĆō 4.8 million km ŌĆó Bears maximum passenger (85%) and freight traffic (60%) ŌĆó Rising investments ŌĆó Growing Private Sector Involvement ŌĆó Rapid growth in NH [100,000 km by 2017] ŌĆó Overseas Investments Roads* Total length : 4.87 Mn km State Highways National Highways District and Rural Roads ŌĆó 1,46,100 Km ŌĆó 3.0% of total roads ŌĆó 97,135 Km ŌĆó 2.0% of total roads ŌĆó 46,26,500 Km ŌĆó 95.0% of total roads Source : Ministry of Road Transport and Highways (MoRTH), *As on July 2015 63 3 7 27 Proportion of freight traffic across modes of transport [2013-14] [In %] Road Coastal Pipeline Rail 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 2010-2015 2016-2020 25% 32% 61% 59% 14% 9% Investments in Roads [In bn] NH State Rural 4358 8651 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 2010-2015 2016-2020 35% 56% 65% 44% Financing of National Highways Public Private

- 3. National Highways NH ŌĆō 2% of road network, 40% of traffic NHAI ŌĆō Nodal Agency ŌĆō launched NHDP in 2000 21440 23769 28977 33689 76818 79116 92851 96214 0 20000 40000 60000 80000 100000 120000 Trend in NH Network [km] 1950 1965 1980 1995 2012 2013 2014 2015 NHDP ŌĆōBuilding, Upgradation, rehabilitation & broadening of existing NH ŌĆō 7 phases NHDP Phases 6-laning of existing NH NHDP Projects ŌĆō Private Players [EPC Contract / BOT] Execution picks up in 2015-16; Nearly 50% completed 7994 7142 12109 13203 6500 1000 700 48648 7714 6394 6594 1439 2216 - 22 24379 0 10000 20000 30000 40000 50000 60000 Phase I Phase II Phase III Phase IV Phase V Phase VI Phase VII Total Total Length Completed NHDP ŌĆō Cash contracts ŌĆō Central road fund, grants, toll revenue 201 234 254 223 185 251 353 516 669 792 NH - Year-wise estimated investment [Rs Billion] 56% 19% 7% 2% 2% 14% NHAI Sources of Funds Cess Toll Premium External Assistance Budgetary Support Borrowings

- 4. State Roads 20% of road network, 40% traffic SH, MDR, ODR & Rural Roads PWD [Cash] & RDC [BOT] ŌĆō Awards contracts Central Road Fund ŌĆō By Central Govt 10% 9% 9% 8% 8% 56% State-wise budgeted expenditure for the year 2013-14 under CRF Maharashtra Rajasthan Andhra Pradesh Uttar Pradesh Madhya Pradesh Other States 10% [CRF] ŌĆō Devpt of roads under ISC EI 8% 13% 10% 7% 62% Total allocations under ISC from 2001-02 to 2011-12 MP Maharashtra Rajasthan Sikkim Other States 7% 7% 7% 7% 10% 7% 55% Total allocations under EI from 2001-02 to 2011-12 AP Jharkhand Karnataka Nagaland Odisha TN OthersInvestments 380 440 565 623 691 778 879 992 1125 1287 State Roads : Overall Investments [Rs billion]

- 5. Rural Roads 149 109 84 131 121 131 147 159 171 185 Rural Roads : Year-wise Investments (Rs billion)

- 6. Top Players Track 21.7 24 9.7 47.1 16.6 4.7 15.1 6 15.8 73 2.4 -2.2 -3.7 12.3 5.7 -5.9 8.6 -18.3 7.5 45 5.7 5.7 6.5 10.5 12.5 2.8 9.5 -1.5 15 15.2 -40 -20 0 20 40 60 80 Ashoka Buildcon GMR Hindustan Construction Company Ltd IRB Infrastrcutre Developers Ltd Larsen & Toubro Punj Lloyd Ltd Reliance Infrastructure Limited IVRCL Infrastructre Projects Ltd KNR Constructions Ltd Noida Toll Bridge Company Limited OPM NPM RoCE Top Companies with exposure to roads sector : Margins & RoCE [In %]

- 7. Trends in the road sector ’üČ Increasing private sector participation ’üČ Partnerships ŌĆō Indian & Foreign firms ’üČ IndiaŌĆÖs focus on infrastructure ’üČ Infrastructure initiatives

- 8. Growth Drivers 1.2 1.3 1.3 1.6 1.8 2.4 3 3.1 3.2 3.1 3.2 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 Trends in passenger vehicle sales [In million] 567.6 760.7 929.1 832.6 699 697.1 FY10 FY11 FY12 FY13 FY14 FY15 Trends in commercial vehicle sales [In 000's] ’é¦ Reduce delays ’é¦ Proper Maintenance ’é¦ Transparency ’é¦ Improves investor confidence ’é¦ Investments to rise gradually

- 9. Key Catalysts behind increasing demand Higher Road Traffic Better quality roads makes road travel cheaper and safer Higher Individual discretionary spending Growing domestic trade flows Increasing finance on vehicle loans

- 10. Key Issues in the Sector

- 13. Presented By Dhara B Shah Divya Liz George George Jacob Ken Sunny Shankar Ramesh

Editor's Notes

- #4: National highways (NHs) constitute around 2% of the road network but carry about 40% of the total road traffic. The National Highways Authority of India (NHAI), the nodal agency under the Ministry of Road Transport & Highways (MoRTH), is responsible for building, maintaining and upgrading NHs. In order to develop the NH network in the country, NHAI launched the National Highways Development Programme (NHDP) in December 2000. NHDP projects are awarded to private players either on an EPC (cash) contract or on a buildoperatetransfer (BOT) basis. NHDP cash contracts are mainly financed through budgetary allocations from the Central Road Fund, negative grants/ premium received, and toll revenues. Loans and grants are also received from the World Bank and the Asian Development Bank.

- #5: State roads come under the jurisdiction of the respective state governments. However, the Central government may provide financial assistance to state governments through various schemes for development of the road network. The responsibility of awarding of contracts for road development is entrusted with two state government divisions, namely the Public Works Department (PWD) and Road Development Corporation (RDC). Generally, cash contracts are awarded by the state PWD, while BOT Annuity and BOT Toll contracts are typically awarded by the respective state RDC. The CRF is funded from the cess collected on the sale of petrol and high speed diesel (HSD). On every litre of petrol and high speed diesel that is sold, a cess of Rs 2 is collected. The fund provides assistance to states for development and maintenance of state roads, rural roads, national highways, under and over bridges and safety works at unmanned railway crossings. 11 per cent of the cess collected on HSD and 30 per cent of that on petrol is allocated towards maintenance of state roads.

- #6: Rural roads connect rural habitations to each other as well as with state and national highways. Of the total 4.6 million km road network in India, rural roads account for around 3.7 million km (80%). PMGSY was launched in December 2000 with the primary objective of providing good allweather connectivity to plain areas with population above 500 and hilly areas with population above 250 persons. The programme also involves upgradation of the existing rural roads to allweather roads. The PMGSY aims to provide new connectivity to 164,849 habitations. Up to March 2015, 426,629 km of road had been constructed. Further 51,253 habitations have been connected under the scheme up to March 2014. The programme also aims to upgrade about 374,844 km of existing roads. It is implemented only through cash contracts. To expedite its implementation, in 2005, a part of this programme was brought under Bharat Nirman a business plan to build rural infrastructure. PMGSY, which is a 100% centrally sponsored scheme, is funded by budgetary allocations, Central Road Fund (CRF) on high speed diesel (HSD), market committee fees, loan assistance from the National Bank for Agriculture and Rural Development (NABARD), World Bank and the Asian Development Bank. Repayment of the principal amount of the loan taken from NABARD has commenced from 201011. Due to this outflow, investment in PMGSY declined, thereby impacting the progress of the programme. All upgradation projects were suspended in this period.

- #10: Growing domestic trade flows have led to a rise in commercial vehicles and freight movement Increasing financing on vehicleloans RoadŌĆÖs trafficshare of the total traffic* in India has grown from 13.8 percent to 60 percent in freight traffic, and from 32 percent to 85 percent in passenger traffic over 1951ŌĆō2014