Cost Segregation Presentation

•Download as PPT, PDF•

0 likes•255 views

The document discusses cost segregation, which analyzes construction or renovation costs to identify portions that can be depreciated faster for tax purposes. It provides examples of cost segregation studies performed for a manufacturing facility and office building that reallocated costs from 39-year to 5, 7, and 15-year depreciation schedules, yielding substantial first-year tax savings. The document promotes cost segregation services as an easy to explain, value-added service that provides documented tax benefits for clients.

![Jack Young, GPPA, CPA Experience in: Financial Analysis Income Tax Consulting Machinery and Real Estate Appraisal USPAP appraiser of Machinery and Equipment Certified Public Accountant Formerly with: KPMG Price Kong, CPAs Bar None Auction West Auction Jack Young contact information (530) 219-7900 [email_address] www.norcalvaluation.com](https://image.slidesharecdn.com/gilandjackwtascostsegregationpresentation-12533767036542-phpapp02/85/Cost-Segregation-Presentation-3-320.jpg)

Cost Segregation Presentation

- 1. Cost Segregation – Maximizing Tax Savings Gil Mitchell – Director WTAS LLC 100 First Street, Suite 1600, San Francisco, CA 94105 gil.mitchell@wtas.com (Tel) 415.764.2750, (Fax) 415.764.2770 www.wtas.com

- 2. West Region Leader Gil Mitchell, ASA – San Francisco Has 25 years experience in : Cost Segregation, Property Tax Consulting, Machinery Appraisal and Real Estate Appraisal ASA in Machinery and Equipment Appraisal Certified General Real Estate Appraiser AG005951 Formerly with: Arthur Andersen, Grant Thornton, Moss Adams and Oregon Department of Revenue Gil’s Contact information: gil.mitchell@wtas.com (Tel) 415.764.2750, (Fax) 415.764.2770

- 3. Jack Young, GPPA, CPA Experience in: Financial Analysis Income Tax Consulting Machinery and Real Estate Appraisal USPAP appraiser of Machinery and Equipment Certified Public Accountant Formerly with: KPMG Price Kong, CPAs Bar None Auction West Auction Jack Young contact information (530) 219-7900 [email_address] www.norcalvaluation.com

- 4. Tax Deferral Strategy Analysis of project costs for constructed or purchased buildings & improvements Segregation of costs into “Personal Property” and “Real Property” A Means of Accelerating Depreciation Expense for Building Owner "A nickel isn't worth a dime today." What Is Cost Segregation?

- 5. How Does Cost Segregation Work? Cost Segregation analyzes project costs to identify personal property (an Investment Tax Credit Standard) within and without of the structure.

- 6. The IRS has established asset classes "1250 & 1245" and depreciable lives for constructed properties 27.5 years – Residential 1250 39 years – Commercial/Industrial 1250 Classes with shorter lives 15 years – Site Improvements 1250 7 years – Trade Fixtures 1245 5 years – Trade Fixtures 1245 Depreciation Lives Under Current Tax Law (MACRS)

- 7. New Construction Purchased Facilities Remodels Renovations Expansions Leasehold Improvements Estates (Change in Basis) What Kinds of Projects Benefit?

- 8. Can A Study Be Performed Retroactively? Yes! Depreciation is considered a method of accounting. A study that “looks back” to prior tax years and results in a depreciation adjustment is an IRC 481(a) adjustment and is deducted over one year. Prior returns are not amended. We can go back to 1987.

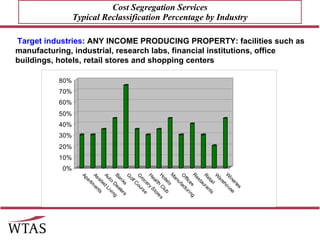

- 9. Cost Segregation Services Typical Reclassification Percentage by Industry Target industries : ANY INCOME PRODUCING PROPERTY: facilities such as manufacturing, industrial, research labs, financial institutions, office buildings, hotels, retail stores and shopping centers

- 10. Increased Cash Flow No Obligation Proposals We Estimate the Benefits in Advance A “Complete Depreciation Solution” for Clients Buying/Developing Real Estate Documentation Minimize property taxes Proceeds can be used for debt repayment, reinvestment, capital repairs, or other acquisitions Benefits to Client

- 11. Manufacturing Facility - Tenant Improvement Analysis Project cost = 1,671,450 Date place in service = 2002 Amount moved out of 39 year life to 5, 7 & 15 year lives = $1,379,000 1st year benefit with 30% bonus depreciation = $215,000

- 12. Office Building - Retroactive study Purchase price = $2,794,000 Date place in service = 1996 Amount moved out of 39 year life to 5, 7 & 15 year lives = $445,000 1st year increased depreciation = $266,200 1st year benefit with change of accounting = $93,170

- 13. Summary A Value-Added Service to Our Clients Easy to Explain - Compelling Benefits Documented Support for Our Client Written Marketing Materials No Obligation Proposals

- 14. Next Step: No Obligation Proposal What we need: Depreciation schedule for purchased property Contractors cost breakdown for new construction Your proposal will include: Documents suitable to take to your tax advisor. Estimated cost allocation of short lived items. Estimated tax savings Appraisal fee proposal

- 15. Brainstorming: What specific clients or properties would benefit from a Cost Segregation Study: Office buildings Wineries Apartments Shopping centers Retail Restaurants Grocery Stores Manufacturing

- 16. Questions? ? ? ?

Editor's Notes

- Projects over 1 million Post 1986 construction

- Why do clients want this done? Increased cash flow. It allows you, your clients to recapture your depreciation deductions sooner which can, in turn, be used elsewhere. Property Taxes: Overtime expenses, Fasttrack Environmental remediation – cleanups, Demoltion

- It has been a real pleasure to be here today to talk with you about the important opportunities that this major new federal deduction has created. I want to thank you for giving me your time and attention and, before we close up, I wanted to open the floor up one last time for questions. Also, please know, if you think of questions after I/we leave here today, you are more than welcome to follow up with us via email or with a telephone call.