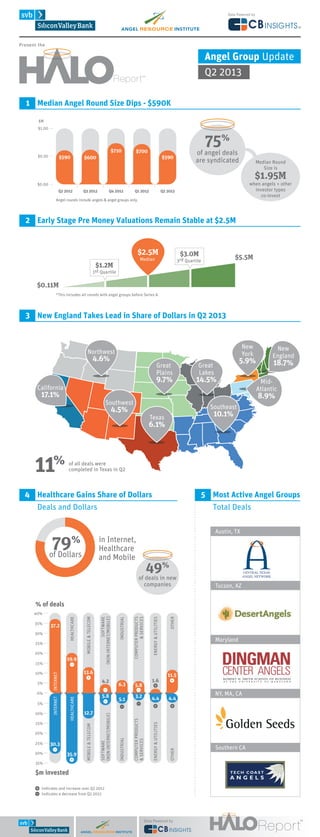

Halo Report Q2 2013 Infographic

The Halo Report is a nationwide survey of Angel Groups' investment activity produced by the Angel Resource Institute, Silicon Valley Bank and CB Insights. The Q2 2013 Halo Report shows angel investment round sizes dipped up to a median of $590K per deal, pre-money valuations remain stable at $2.5 million and 74% of angel group deals are syndicated. When angel groups co-invest with other types of investors, the media round size goes up to $1.95M. US angel investment continues to be dispersed nationwide. For the first time, the report separates Texas, which has 11% of angel group deals in Q2, behind California, New England and the Southeast. New England-based angel groups closed deals worth slightly more than deals in California in Q2. The sectors getting funding remain concentrated in Internet, healthcare and mobile, with 71% of completed Q2 deals and 79% of Q2 dollars in these categories.

Halo Report Q2 2013 Infographic

- 1. Data Powered by Present the Angel Group Update Q2 2013 1 Median Angel Round Size Dips - $590K $M $1.00 $0.50 $590 $710 $600 75% $700 $590 of angel deals are syndicated Median Round Size is $1.95M when angels + other investor types co-invest $0.00 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Angel rounds include angels & angel groups only. 2 Early Stage Pre Money Valuations Remain Stable at $2.5M $2.5M $3.0M Median $1.2M $5.5M 3rd Quartile 1st Quartile $0.11M *This includes all rounds with angel groups before Series A. 3 New England Takes Lead in Share of Dollars in Q2 2013 New York Northwest 4.6% Great Plains 9.7% California 17.1% 14.5% 10.1% Texas of all deals were completed in Texas in Q2 4 Healthcare Gains Share of Dollars Deals and Dollars 79 % 5 Most Active Angel Groups Total Deals Austin, TX in Internet, Healthcare and Mobile of Dollars 49% of deals in new companies Tucson, AZ % of deals 35.9 35% 3.2 4.4 OTHER INDUSTRIAL Maryland 11.5 4.4 OTHER 30.3 5.8 ENERGY & UTILITIES 25% 30% 5.1 1.6 COMPUTER PRODUCTS & SERVICES 20% 12.7 6.3 INDUSTRIAL 15% SOFTWARE (NON-INTERNET/MOBILE) 10% 5.8 MOBILE & TELECOM 5% 4.2 HEALTHCARE 0% INTERNET 5% 13.6 INTERNET 10% ENERGY & UTILITIES 19.9 15% COMPUTER PRODUCTS & SERVICES 25% SOFTWARE (NON-INTERNET/MOBILE) 37.2 30% MOBILE & TELECOM HEALTHCARE 40% 20% MidAtlantic Southeast 6.1% 35% 18.7% 8.9% Southwest 4.5% 11% 5.9% Great Lakes New England $m invested Indicates and increase over Q2 2012 Indicates a decrease from Q2 2012 Data Powered by NY, MA, CA Southern CA