Ias 38 Intangible Assets (1)

- 1. IAS 38INTANGIBLE ASSETS (Part one)Definition & Recognition1/17/20101IAS 38 Intangible Assets Part One

- 2. ObjectiveSpecific criteria for recognition of intangible assetsMeasure carrying amount of intangible assetsSpecific disclosures about intangible assets1/17/20102IAS 38 Intangible Assets Part One

- 3. Scope Intangible assets exceptWithin the scope of another standardFinancial assets IAS 39Exploration and evaluation assets of mineral resources IFRS 6Expenditure on the development and extraction of minerals, oil, natural gas and similar non-regenerative resources1/17/20103IAS 38 Intangible Assets Part One

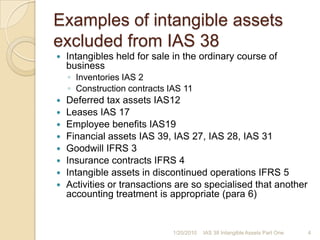

- 4. Examples of intangible assets excluded from IAS 38Intangibles held for sale in the ordinary course of business Inventories IAS 2 Construction contracts IAS 11Deferred tax assets IAS12Leases IAS 17Employee benefits IAS19Financial assets IAS 39, IAS 27, IAS 28, IAS 31Goodwill IFRS 3Insurance contracts IFRS 4Intangible assets in discontinued operations IFRS 5Activities or transactions are so specialised that another accounting treatment is appropriate (para 6)1/17/20104IAS 38 Intangible Assets Part One

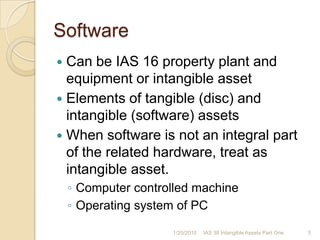

- 5. SoftwareCan be IAS 16 property plant and equipment or intangible assetElements of tangible (disc) and intangible (software) assetsWhen software is not an integral part of the related hardware, treat as intangible asset.Computer controlled machineOperating system of PC1/17/20105IAS 38 Intangible Assets Part One

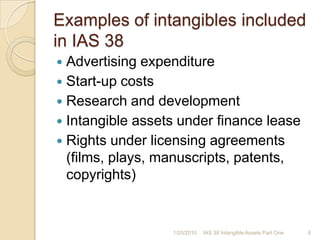

- 6. Examples of intangibles included in IAS 38Advertising expenditureStart-up costsResearch and developmentIntangible assets under finance leaseRights under licensing agreements (films, plays, manuscripts, patents, copyrights)1/17/20106IAS 38 Intangible Assets Part One

- 7. Definitions1/17/20107IAS 38 Intangible Assets Part One

- 8. Definitions1/17/20108IAS 38 Intangible Assets Part One

- 9. Definitions1/17/20109IAS 38 Intangible Assets Part One

- 10. Definitions1/17/201010IAS 38 Intangible Assets Part One

- 11. Definitions1/17/201011IAS 38 Intangible Assets Part One

- 12. Definitions1/17/201012IAS 38 Intangible Assets Part One

- 13. Intangible assets1/17/201013IAS 38 Intangible Assets Part One

- 14. Recognition of intangible assetMust meet definitionIdentifiableControl over a resourceFuture economic benefitsIf it does not meet definitionRecognise expenditure as incurredIf acquired in a business combinationForms part of goodwill at acquisition date1/17/201014IAS 38 Intangible Assets Part One

- 15. Identifiable Intangible AssetSeparableFrom entityCan be sold, transferred, licensed, exchanged, rentedIndividually or related contract, asset & liabilityArises from contractual or legal rightsThe rights do not have to be separableCONTINUED IN PART 2…1/17/201015IAS 38 Intangible Assets Part One