India Telecom Subscription Data as on 31st January 2013

ŌĆó

0 likesŌĆó1,744 views

I. Total telephone subscribers in India decreased slightly in January 2013 to 893.15 million from 895.51 million in December 2012. Urban subscription decreased while rural subscription increased, resulting in urban and rural teledensities of 148.46 and 40.07 respectively. II. Total wireless subscribers decreased to 862.62 million in January from 864.72 million in December, with urban subscribers decreasing and rural increasing. Private operators held 87.78% of the wireless market share. III. Wireline subscribers declined to 30.52 million in January from 30.79 million in December. BSNL and MTNL held 79.34% of the wireline market share.

India Telecom Subscription Data as on 31st January 2013

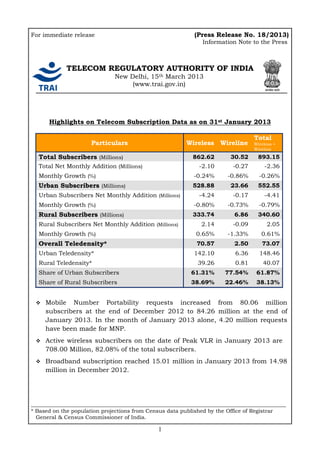

- 1. For immediate release (Press Release No. 18/2013) Information Note to the Press TELECOM REGULATORY AUTHORITY OF INDIA New Delhi, 15th March 2013 (www.trai.gov.in) Highlights on Telecom Subscription Data as on 31st January 2013 Total Particulars Wireless Wireline Wireless + Wireline Total Subscribers (Millions) 862.62 30.52 893.15 Total Net Monthly Addition (Millions) -2.10 -0.27 -2.36 Monthly Growth (%) -0.24% -0.86% -0.26% Urban Subscribers (Millions) 528.88 23.66 552.55 Urban Subscribers Net Monthly Addition (Millions) -4.24 -0.17 -4.41 Monthly Growth (%) -0.80% -0.73% -0.79% Rural Subscribers (Millions) 333.74 6.86 340.60 Rural Subscribers Net Monthly Addition (Millions) 2.14 -0.09 2.05 Monthly Growth (%) 0.65% -1.33% 0.61% Overall Teledensity* 70.57 2.50 73.07 Urban Teledensity* 142.10 6.36 148.46 Rural Teledensity* 39.26 0.81 40.07 Share of Urban Subscribers 61.31% 77.54% 61.87% Share of Rural Subscribers 38.69% 22.46% 38.13% ’üČ Mobile Number Portability requests increased from 80.06 million subscribers at the end of December 2012 to 84.26 million at the end of January 2013. In the month of January 2013 alone, 4.20 million requests have been made for MNP. ’üČ Active wireless subscribers on the date of Peak VLR in January 2013 are 708.00 Million, 82.08% of the total subscribers. ’üČ Broadband subscription reached 15.01 million in January 2013 from 14.98 million in December 2012. _______________________________________________________________________________________________ * Based on the population projections from Census data published by the Office of Registrar General & Census Commissioner of India. 1

- 2. I. Total Telephone Subscribers ’éĘ The number of telephone subscribers in India decreased to 893.15 million at the end of January, 2013 from 895.51 million at the end of December 2012, thereby showing a monthly growth rate of -0.26%. The share of urban subscribers has declined to 61.87% from 62.20% whereas share of rural subscribers has increased to 38.13% in the month of January 2013. With this, the overall Teledensity in India decreased to 73.07 at the end of January, 2013 from 73.34 of the previous month. ’éĘ Subscription in the urban areas decreased from 556.96 million in December, 2012 to 552.55 million at the end of January, 2013. Subscription in rural areas increased from 338.54 million to 340.60 million during the same period. The monthly growth rate of urban and rural subscription is -0.79% and 0.61% respectively. The overall urban Teledensity has decreased from 149.90 to 148.46 and Rural Teledensity increased from 39.85 to 40.07. 2

- 3. Overall Teledensity (Circle Wise) Notes: 1. Population data/Projections are available state wise only. 2. Teledensity figures are derived from the subscriber data provided by the operators and the population projections published by the Office of the Registrar General & Census Commissioner, India. 3. Delhi Service area, apart from the State of Delhi, includes wireless subscribers of the areas served by the local exchanges of Ghaziabad & Noida (in UP) and Gurgaon & Faridabad (in Haryana). West Bengal service area includes Kolkata, Maharashtra includes Mumbai and Tamil Nadu includes Chennai 3

- 4. II. Wireless Segment (GSM, CDMA & FWP) ’éĘ Total wireless subscriber base decreased from 864.72 million in December 2012 to 862.62 million at the end of January 2013, registering a monthly growth of ŌĆō0.24%. This decline is mainly due to large scale disconnections of inactive SIMs by some of the service providers. The share of urban wireless subscribers has decreased from 61.65% to 61.31% where as share of rural wireless subscribers has increased from 38.35% to 38.69%. The overall wireless Teledensity in India has reached 70.57. ŌĆó Wireless subscription in urban areas decreased from 533.12 million in December 2012 to 528.88 million at the end of January 2013. The wireless subscription in rural areas increased from 331.60 million to 333.74 million during the same period. The urban wireless Teledensity has decreased from 143.48 to 142.10 and rural Teledensity has increased from 39.04 to 39.26. Detailed statistics is at Annexure I. 4

- 5. ŌĆó Private operators hold 87.78% of the wireless market share (based on subscriber base) where as BSNL and MTNL, the two PSU operators hold only 12.22% market share. The graphical presentations of market shares and shares in net additions of all the service providers during the month of January, 2013 are given below: A. Service Provider wise Market Share as on 31st January, 2013. B. Service Provider wise net subscriber addition during January 2013 5

- 6. III. VLR Data Out of the total 862.62 million wireless subscribers, 708.00* million were active on the date of Peak VLR for the month of January 2013. The proportion of VLR subscribers is approximately 82.08% of the total wireless subscriber base reported by the service providers. Circle-wise, Maharashtra has the highest proportion of VLR subscribers with 88.15% followed by Madhya Pradesh (87.52%) and Gujarat (85.88%); Tamil Nadu (incl. Chennai) has the lowest proportion with 73.79%. Service Provider wise, Idea leads the tally with 98.55% followed by Vodafone (95.18%). The detailed statistics of proportionate VLR is at Annexure II & methodology used for reporting subscriber base/active subscribers is at Annexure IV. A. Proportion of VLR subscribers (Service Provider wise) B. Service Provider wise growth in total subscribers (Dec.2012 ŌĆō Jan.2013) * The total active VLR number excludes the CDMA VLR figure of M/s BSNL as the service provider has not provided the VLR figures of their total CDMA subscriber base of 2.78 million. 6

- 7. C. Proportion of VLR subscribers (Service Area wise) D. Service Area wise growth in total subscribers (Dec. 2012 ŌĆō Jan. 2013) 7

- 8. IV. Mobile Number Portability As per the data reported by the service providers, by the end of January 2013 about 84.26 million subscribers have submitted their requests to different service providers for porting their mobile number. In MNP Zone-I (Northern & Western India) maximum number of requests have been received in Rajasthan (7.96 million) followed by Gujarat (7.34 million) whereas in MNP Zone-II (Southern & Eastern) maximum number of requests have been received in Karnataka (10.20 million) followed by Andhra Pradesh Service area (7.62 million). In the month of January 2013, total number of subscribers who have submitted their request for MNP is 4.20 million. The status of MNP requests in various service areas is given below: Service Area Wise MNP Status at the end of January 2013 Zone -1 Zone - 2 Number of Number of Service Area Porting Service Area Porting Requests Requests Delhi 2740132 Andhra Pradesh 7622912 Gujarat 7343825 Assam 333500 Himachal Pradesh 316019 Bihar 1654105 Haryana 3027364 Karnataka 10208134 Jammu & Kashmir 14368 Kerala 3552516 Maharashtra 6969298 Kolkata 1915282 Mumbai 2944310 Madhya Pradesh 4941624 Punjab 2713203 North East 149344 Rajasthan 7962868 Orissa 1868317 Uttar Pradesh - East 5068125 Tamil Nadu 4973129 Uttar Pradesh - West 4889155 West Bengal 3057035 Total 43,988,667 Total 40,275,898 Total (Zone-1 + Zone-2) 84,264,565 Net Addition (in January 2013) 4,203,611 8

- 9. V. Wireline Segment Wireline subscriber base declined from 30.79 million at the end of December 2012 to 30.52 Million at the end of January 2013. Net reduction in wireline subscriber base was 0.27 million. The share of urban subscribers has increased from 77.43% to 77.54% where as share of rural subscribers has declined from 22.66% to 22.57%. The overall wireline Teledensity has marginally decreased from 2.52 in December 2012 to 2.50 in January 2013, with urban and rural Teledensity being 6.36 and 0.81 respectively. BSNL and MTNL, the two PSU operators hold 79.34% of the Wireline market share. Detailed statistics is at Annexure-III. The graphical presentation of market share of all service providers as on 31st January 2013 is given below: A. Service Provider wise Market Share as on 31st January 2013 9

- 10. B. Wireline Service Provider wise Net addition during January 2013: 10

- 11. VI. Category wise Growth ’éĘ As can be seen from the following tables, the Circles in Category A show the highest reduction in subscriber base and Circles in Category Metro show highest rate of decline wireless segment. In wireline segment, Circles in Category C show the highest reduction and highest rate of decline in subscriber base from December 2012 to January 2013. Category wise Net Additions and subscriber base Net Additions during the Subscriber Base as on 31st month of January, 2013 January, 2013 Category Wireline Wireless Wireline Wireless Circle A -28301 -975728 12140908 306151879 Circle B -69649 -243725 9597159 341163297 Circle C -173736 -491911 1687730 121528339 Metro 6496 -385036 7095716 93780271 All India -265,190 -2,096,400 30,521,513 862,623,786 Category-wise Growth Rate in Access Service Monthly Rate of Growth Yearly rate of growth (Dec-2012 to Jan-2013) (Jan-2012 to Jan-2013) Category Wireline Wireless Wireline Wireless Circle A -0.23% -0.32% -4.92% -3.79% Circle B -0.72% -0.07% -8.35% -4.52% Circle C -9.33% -0.40% -18.69% -2.06% Metro 0.09% -0.41% 0.29% -9.93% All India -0.86% -0.24% -5.77% -4.55% ’éĘ Metros indicate data for Delhi, Mumbai & Kolkata. Data for Chennai service area has been included in Circle A, as part of TN 11

- 12. VII. Broadband (Ōēź 256 Kbps download) Total Broadband subscriber base has increased from 14.98 million at the end of December 2012 to 15.01 million at the end of January 2013, there by showing a monthly growth of 0.24%. Yearly growth in broadband subscribers is 11.88% during the last one year (January 2012 to January 2013). As on 31st January 2013, there are 159 Internet Service Providers (ISPs) which are providing broadband services in the country. Out of these, 113 ISPs have provided broadband subscription data for the month of January 2013, for the rest of the ISPs data from previous month has been retained (Data from top 10 ISPs, which constitute 93.34% of the total subscriber base, have been received for the month of January 2013). Top five ISPs in terms of market share (based on subscriber base) are: BSNL (9.93 million), Bharti Airtel (1.39 million), MTNL (1.09 million), Hathway (0.37 million) and You Broadband (0.30 million). Contact details in case of any clarification: Manish Sinha, Advisor (F&EA), TRAI Mahanagar Doorsanchar Bhawan Jawahar Lal Nehru Marg, Authorised to issue: New Delhi ŌĆō 110002, Ph: 011-23230752 Fax: 011-23236650 (Manish Sinha) E-mail: adveco@trai.gov.in Advisor (F&EA) Note: Information in this Press Release is based on the data provided by the Service Providers. 12

- 13. Wireless Subscriber Base Annexure-I Page 1 of 2 Group Bharti Reliance Vodafone Tata Idea Aircel BSNL Circle Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Andhra Pradesh 17704841 17884934 6809259 6778745 6080916 5688911 6898277 6659964 10632055 10838496 1871685 1802320 9219802 9257286 Assam 3826231 3851324 3060184 3048336 2188073 2208121 120238 0 368973 382840 3542284 3550416 1228242 1230918 Bihar 18619726 18798853 9215889 9205292 6381278 6381973 3853362 3745212 5459296 5587271 4981643 4767543 6003257 5975541 Delhi 9027895 9105754 7424422 7441989 8449120 8460140 3755144 3756016 4650742 4737090 2951145 2850948 0 0 Gujarat 6810708 6983467 6719447 6723250 15801116 15811116 3018060 2956176 8018178 8226195 338457 294655 4254238 4265027 Haryana 2217759 2260697 2121823 2127552 4437015 4460102 2677383 2667699 3533255 3614670 427498 185758 3043033 3052798 Himachal Pradesh 1904509 1914645 1436357 1466812 475329 476232 196230 190353 447450 448972 714277 699378 1586782 1601048 J&K 2302707 2320283 606558 606341 666009 610925 85035 0 201578 208269 1786423 1808200 1153690 1162539 Karnataka 15896254 16005226 6416357 6422020 6452620 6578801 6309062 6020557 5890723 6070121 1544826 1563895 6998146 7022983 Kerala 3433402 3464751 2885016 2886400 6067506 6099518 1992262 1896682 7778697 7869341 1522927 354883 7621921 7666262 Kolkata 3579518 3662644 4152963 4123621 4084284 4138689 2804426 2885466 1153806 1250623 1858443 1852675 2315303 2295804 Madhya Pradesh 9656948 9796757 11549105 11585308 4101877 3966891 3937441 3896930 14731226 14991810 680866 653287 5030107 5140167 Maharashtra 9835555 9930085 7830723 7731522 12977123 13074351 6519501 6340285 15554910 15840410 1116017 1134782 6687309 6737300 Mumbai 3483357 3559119 5982157 5984368 6160353 6110330 3488432 3432943 2803928 2886271 1391669 1450948 0 0 North East 2573994 2610008 830331 836595 928563 939346 77214 0 257734 267417 2334209 2338464 1736293 1733524 Orissa 6652023 6756065 3813211 3664119 2789575 2875352 2205917 2142853 911343 963793 2791997 2893967 4438237 4470678 Punjab 6800705 6857498 2840719 2847712 4309853 4329581 2493061 2455289 5493576 5565174 973252 972375 4389946 4397239 Rajasthan 14181992 14379504 5379429 5385665 8565366 8637532 3071790 2985998 4515251 4674801 2712870 2792442 5930085 5911845 Tamil Nadu (incl. Chennai) 13318162 13343591 6459310 6541975 11869338 11961249 5746318 5508564 2172759 2228730 21725106 21367505 9439883 9489101 U.P.(E) 14940643 15013282 9648465 9661637 14526236 14491774 4141889 4083136 6978230 6968905 3589906 3774238 10295513 10303309 U.P.(W) 6413401 6532214 6647314 6587565 8999073 9031358 4026419 3931987 10189727 10385262 1509375 1409150 4928465 4903491 West Bengal 8726562 9162866 6699230 6650979 11165667 11367866 2140661 2125904 2203390 2393404 2982409 3053462 3622095 3624033 Total 181906892 184193567 118528269 118307803 147476290 147700158 69558122 67682014 113946827 116399865 63347284 61571291 99922347 100240893 13

- 14. Wireless Subscriber Base Annexure-I Page 2 of 2 Group MTNL Unitech Sistema Loop Videocon Quadrant (HFCL) Total Circle Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Andhra Pradesh 0 0 4029580 4226266 679838 637894 0 0 9763 0 0 0 63936016 63774816 Assam 0 0 779 776 1280 1280 0 0 0 0 0 0 14336284 14274011 Bihar 0 0 5005668 4750129 1481580 1314278 0 0 18598 18596 0 0 61020297 60544688 Delhi 2591964 2590274 0 0 962588 929889 0 0 0 0 0 0 39813020 39872100 Gujarat 0 0 4430904 4650839 231729 224103 0 0 657286 618785 0 0 50280123 50753613 Haryana 0 0 437 405 156659 147716 0 0 913010 794797 0 0 19527872 19312194 Himachal Pradesh 0 0 151 143 71 71 0 0 44555 0 0 0 6805711 6797654 J&K 0 0 319 312 21 21 0 0 0 0 0 0 6802340 6716890 Karnataka 0 0 1061461 686045 2204660 2137127 0 0 8086 0 0 0 52782195 52506775 Kerala 0 0 391794 263745 541973 501620 0 0 9730 0 0 0 32245228 31003202 Kolkata 0 0 1774330 1456841 887156 882258 0 0 12 0 0 0 22610241 22548621 Madhya Pradesh 0 0 1313 1255 3121 3153 0 0 976589 806625 0 0 50668593 50842183 Maharashtra 0 0 5638910 5502934 676571 651414 0 0 8683 0 0 0 66845302 66943083 Mumbai 2709954 2607846 1841764 1868314 459822 447707 2995459 3011704 425151 0 0 0 31742046 31359550 North East 0 0 90 90 151 151 0 0 0 0 0 0 8738579 8725595 Orissa 0 0 703260 701887 803 787 0 0 10673 0 0 0 24317039 24469501 Punjab 0 0 430 411 1147 1146 0 0 0 0 1695919 1588395 28998608 29014820 Rajasthan 0 0 1045 1032 2207814 2188875 0 0 6687 0 0 0 46572329 46957694 Tamil Nadu (incl. Chennai) 0 0 803528 505180 1234562 1227697 0 0 515005 0 0 0 73283971 72173592 U.P.(E) 0 0 7262667 7399456 581226 537198 0 0 14635 14629 0 0 71979410 72247564 U.P.(W) 0 0 5001245 5119624 617722 570069 0 0 5343 3622 0 0 48338084 48474342 West Bengal 0 0 3570869 2983788 1949509 1948996 0 0 16506 0 0 0 43076898 43311298 Total 5301918 5198120 41520544 40119472 14880003 14353450 2995459 3011704 3640312 2257054 1695919 1588395 864720186 862623786 14

- 15. Proportion of VLR on the date of Peak VLR in the month of Jan, 2013 (%) Annexure-II BSNL Circle Aircel Bharti (Except HFCL Idea Loop MTNL Reliance Sistema Tata Unitech Videocon Vodafone Total CDMA) Andhra Pradesh 58.26 97.66 71.45 97.59 79.96 55.73 74.71 55.97 90.21 84.61 Assam 84.92 97.45 71.40 90.92 67.98 85.23 15.46 96.45 85.46 Bihar 56.11 97.44 34.52 100.03 84.29 38.92 56.69 56.22 1.00 98.84 79.31 Delhi 61.01 82.09 97.01 46.91 91.96 41.60 55.94 90.23 80.23 Gujarat 92.58 95.94 60.63 97.81 89.84 38.76 63.83 57.72 59.50 94.35 85.88 Haryana 86.87 97.13 51.27 98.33 92.28 29.74 66.06 8.64 53.28 96.71 82.76 Himachal Pradesh 59.59 95.58 66.60 101.66 84.41 214.08 59.00 12.59 99.57 82.30 J&K 88.68 94.69 66.28 85.93 63.76 57.14 28.53 90.84 84.74 Karnataka 20.26 98.16 54.30 95.72 83.13 58.37 76.22 0.21 91.80 82.96 Kerala 322.83 95.08 64.16 100.04 76.40 55.31 74.74 0.83 91.05 83.41 Kolkata 61.84 93.45 35.14 93.42 95.32 50.10 80.17 50.98 95.56 79.50 Madhya Pradesh 20.56 96.03 52.38 104.12 86.19 37.20 72.23 25.66 54.17 86.00 87.52 Maharashtra 50.25 92.51 70.34 99.39 88.91 54.09 80.62 62.86 99.20 88.15 Mumbai 58.76 96.47 88.92 45.27 32.90 94.47 28.57 64.97 44.87 90.06 74.71 North East 71.91 96.19 52.20 83.88 81.22 207.28 7.78 90.95 78.57 Orissa 52.54 97.10 58.21 83.39 81.14 67.85 72.74 0.37 90.12 76.07 Punjab 47.99 95.57 54.48 52.67 96.21 94.28 22.86 67.94 13.63 93.70 82.78 Rajasthan 79.88 94.35 46.92 107.68 93.64 49.85 65.25 18.31 99.76 85.83 Tamil Nadu (incl. 60.70 93.96 48.97 75.79 86.22 57.70 61.29 0.41 97.71 73.79 Chennai) U.P. (E) 66.52 97.08 43.43 101.32 82.38 32.81 62.63 66.06 0.55 96.37 80.51 U.P. (W) 65.75 87.38 46.29 97.46 84.61 34.58 60.67 62.26 1.08 97.90 80.89 West Bengal 61.64 96.09 48.49 96.50 93.68 60.59 54.97 62.88 97.37 83.76 Total 63.59 95.12 54.21 52.67 98.55 45.27 39.88 86.64 50.09 68.11 56.64 54.45 95.18 82.08 15

- 16. . Wireline Subscriber Base Annexure-III . Group BSNL MTNL Bharti Reliance Tata Quadrant (HFCL) Sistema Vodafone Total Circle Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Dec-12 Jan-13 Andhra Pradesh 1871305 1868092 125670 125749 89665 89788 169544 169472 5340 5,400 2261524 2258501 Assam 193952 193965 2729 0 60 150 196741 194115 Bihar 543899 376232 4978 4978 11154 11179 30 60 560061 392449 Delhi 0 0 1584555 1586226 1082027 1082791 186636 187050 88935 91407 7740 8,580 2949893 2956054 Gujarat 1561561 1564601 55397 55432 101231 100845 68546 69185 240 330 1786975 1790393 Haryana 515927 509,455 23935 23946 5146 5171 26336 27524 571344 566096 Himachal Pradesh 285983 283,597 4462 4492 2225 2267 292670 290356 J&K 198715 197,867 370 0 199085 197867 Karnataka 1705830 1698816 491746 492064 113270 113,671 137184 139448 3090 3,330 2451120 2447329 Kerala 2972537 2963352 55903 55934 54469 54440 11640 11732 3094549 3085458 Kolkata 938584 935168 93906 93972 81350 81465 36569 37357 1260 1,440 1151669 1149402 Madhya Pradesh 834788 835744 241771 241921 28459 28215 15188 15445 60 60 1120266 1121385 Maharashtra 2113234 2097654 70312 70357 102069 101817 246381 246170 2520 2,640 2534516 2518638 Mumbai 0 0 1870948 1869325 331726 331937 235596 236042 542728 546146 6660 6,810 2987658 2990260 North East 217565 216915 238 0 217803 216915 Orissa 384670 385484 3589 3591 6637 6713 210 240 395106 396028 Punjab 1037448 1019448 105918 105979 26754 26543 15966 16466 183817 184716 240 270 1370143 1353422 Rajasthan 963456 928757 39361 39384 24739 24750 6848 6981 49692 50570 240 240 1084336 1050682 Tamil Nadu (incl. Chennai) 2426680 2416073 485845 486146 148146 148268 72903 73760 1500 1800 3135074 3126047 U.P.(E) 954373 950351 50550 50583 40461 40517 13263 13470 420 420 1059067 1055341 U.P.(W) 735439 734046 24308 24322 5520 5546 8363 8539 30 120 773660 772573 West Bengal 585158 583990 2199 2112 6086 6100 593443 592202 Total 21041104 20759607 3455503 3455551 3278375 3280517 1258739 1259301 1489833 1499361 183817 184716 49692 50570 29640 31890 30786703 30521513 16

- 17. Annexure IV VLR Subscribers in the Wireless Segment Home Location Register (HLR) is a central database that contains details of each mobile phone subscriber that is authorized to use the GSM core network. The HLRs store details of every SIM card issued by the mobile phone operator. Each SIM has a unique identifier called an International Mobile Subscriber Identity (IMSI), which is the primary key to each HLR record. The HLR data is stored for as long as a subscriber remains with the mobile phone operator. HLR also manages the mobility of subscribers by means of updating their position in administrative areas. It sends the subscriber data to a Visitor Location Register (VLR). Subscriber numbers reported by the service providers is the difference between the numbers of IMSI registered in service providerŌĆÖs Home Location Register(HLR) and sum of other figures as given below:- 1 Total IMSI's in HLR (A) 2 Less: (B=a + b + c + d + e) a. Test/Service Cards b. Employees Stock in hand/in Distributional Cannels (Active Card) c. Subscriber Retention d. period expired Service suspended pending e. disconnection 3 Subscribers Base (A-B) 17

- 18. Visitor Location Register (VLR) is a temporary database of the subscribers who have roamed into the particular area, which it serves. Each base station in the network is served by exactly one VLR; hence a subscriber cannot be present in more than one VLR at a time. If subscriber is in active stage i.e. he is able to send/receive calls/SMSs he is available both in HLR and VLR. However, it may be possible that the subscriber is registered in HLR but not in VLR due to the reason that he is either switched-off or moved out of coverage area, not reachable etc. In such circumstances he will be available in HLR but not in VLR. This causes difference between subscriber number reported by the service providers and numbers available in VLR. The VLR data calculated here is on the basis of active subscribers in VLR on the date of Peak VLR of the particular month for which the data is being collected. This data is to be taken from the switches having the purge time of not more than 72 hours. --------- 18