Indian Health-care Industry

- 1. Abhirup Das VGSoM, IIT Kharagpur

- 2. Indian Healthcare Industry : An Overview Constitutes of hospitals and allied services Hospitals: Government & Private Allied Services: Medical diagnostic and pathlabs , Retail pharma, Insurance, Medical tourism An underserved sector with high growth potential According to a Yes Bank report current estimated size - US$ 35 billion (ŌĆś09) expected to touch- US$ 77 billion (ŌĆÖ12-ŌĆÖ13) Growth rate comparable to pharmaceutical and software industry Private sector players achieved 42.4% increase (combined) in net profit in Q1 of ŌĆś09

- 3. Healthcare : Demand & Supply 90 % patients need primary and secondary care Health care industry currently represents more than 5% of GDP

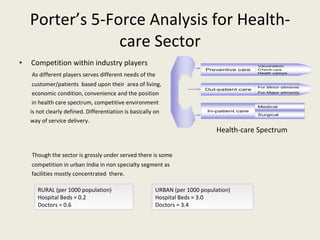

- 4. PorterŌĆÖs 5-Force Analysis for Health-care Sector Competition within industry players As different players serves different needs of the customer/patients based upon their area of living, economic condition, convenience and the position in health care spectrum, competitive environment is not clearly defined. Differentiation is basically on way of service delivery. Though the sector is grossly under served there is some competition in urban India in non specialty segment as facilities mostly concentrated there. Health-care Spectrum RURAL (per 1000 population) Hospital Beds = 0.2 Doctors = 0.6 URBAN (per 1000 population) Hospital Beds = 3.0 Doctors = 3.4

- 5. Major Players Clinics & Nursing Homes Single doctor or family of doctors Good local network and word of mouth clientele Limited range of services and facilities Charitable Trusts Multispecialty hospitals run by religious or social groups Standard of care is driven by individual doctors Subsidized pricing offset by donations Sub-optimal facilities Government Hospitals Ill equipped to provide efficient healthcare Unavailability of appointed doctors and hospital staff Not favoured by semi-urban populations Standard of care is abysmal Organised Sector Very few players in this sector Regional in focus, usually offshoots of tertiary players Most current players are Urban Centric

- 6. PorterŌĆÖs 5-Force Analysis for Health-care Sector (Contd.) Threat of Potential Entrants Each of the industry player has to face competition from new entrants within their own operating environment. In the organized sector, new ventures like Cochlear Ltd (Australia), Reliance Health(ADAG), the Hindujas, Sahara Group, Emami and the Panacea Group are joining existing players like Apollo, Fortis, Columbia-Asia, Piramal Healthcare . Funding is not a problem for these groups , neither the economies of scale, as there is huge untapped market. In urban area, unorganized pharma retail is facing competition from chains like Frank-Ross. Same factor is applicable for pathology centers also. Multinational equipment manufacturer like EES (J&J), Philips, GE are more intensively looking for new markets like India as growth potential is low in already saturated developed nations

- 7. PorterŌĆÖs 5-Force Analysis for Health-care Sector (Contd.) Bargaining power of suppliers Facilitator of health care services are people (doctor, nurses, management stuffs), pharmaceutical companies, equipment manufacturer, insurance provider, government. Bargaining power of these facilitator does not affect every player in same manner. Government regulations are applicable for all, but ŌĆ£cash-less treatmentŌĆØ with collaboration among corporate, insurance firm and hospitals is a competitive advantage for organized player Possibility of supplierŌĆÖs integrating forward is less compared to other industry because most of organization in this sector focuses on their core competency. Threat of Substitutes There no potential threat of substitute product/services for this sector

- 8. PorterŌĆÖs 5-Force Analysis for Health-care Sector (Contd.) Bargaining power of buyers Apart from extreme cases, switching cost for buyer is high in terms of convenience, money comes second. Power of buyers diminishes when he moves from primary care to tertiary care . High quality treatment at a fraction of the cost, in comparison to western countries, makes India an ideal healthcare destination for highly specialized medical care (tertiary care )

- 9. Thank You