INSURANCE AND TYPES OF INSURANCES WITH PRINCIPLES.pptx

ŌĆó

0 likesŌĆó34 views

Insurance, Types of Insurance, Principles of Insurance, Risk and Return

INSURANCE AND TYPES OF INSURANCES WITH PRINCIPLES.pptx

- 1. Dr. Neeraj Sharma BANKING AND INSURANCE

- 2. Insurance may be defined as a form of contract between two parties whereby one party (insurer) agrees to compensate the other party (insured) against a loss (which may or may not arise) against a payment of a consideration (premium). * It is a mean of shifting risk to insurer. * It is an arrangement where the loss feared by a few persons is spread over a large number of persons who are exposed to similar risk. Insurance

- 3. Important terms used in Insurance 1 INSURED 2 INSURER 3 PREMIUM 4 COMPENSATION 5 6 INSURED AMOUNT POLICY COMPENSA TION CONTINGE NCY 9 PERIL 7 RISK 8

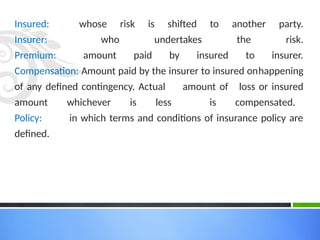

- 4. Insured: whose risk is shifted to another party. Insurer: who undertakes the risk. Premium: amount paid by insured to insurer. Compensation: Amount paid by the insurer to insured onhappening of any defined contingency. Actual amount of loss or insured amount whichever is less is compensated. Policy: in which terms and conditions of insurance policy are defined.

- 5. Insured amount: maximum amount which the insured may get in case of loss. Risk: uncertainty about loss. Contingency: unpredictability. Peril: is an event that has caused a personal or property loss.

- 6. Amount of payment: depends upon value of loss and is to be proved. Insurance is not gambling: because no profit & loss Large number of insured person makes it cheaper Insurance is not Charity: not possible without consideration. Insurable interest: Contract: Always made in writing Consideration: Premium paid to insurer Sharing of financial risk: Co-operative device: Risk evaluation in advance: Good faith: uberrame fidle Contract of indemnity: Nature of Insurance

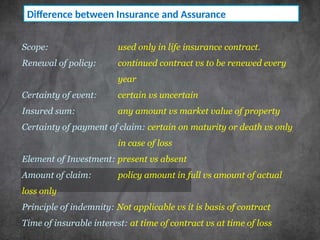

- 7. Scope: used only in life insurance contract. Renewal of policy: continued contract vs to be renewed every year Certainty of event: certain vs uncertain Insured sum: any amount vs market value of property Certainty of payment of claim: certain on maturity or death vs only in case of loss Element of Investment: present vs absent Amount of claim: policy amount in full vs amount of actual loss only Principle of indemnity: Not applicable vs it is basis of contract Time of insurable interest: at time of contract vs at time of loss Difference between Insurance and Assurance

- 8. SECONDARY FUNCTIONS ŌĆó PROVIDES CERTAINITY ŌĆó PROVIDES PROTECTION ŌĆó RISK SHARING ŌĆó PROVIDES SECURITY ŌĆó HELP TO BUSINESS HOUSES PRIMARY FUNCTIONS ŌĆó PREVENTION OF LOSS ŌĆó PROVIDES CAPITAL ŌĆó IMPROVES EFFICIENCY ŌĆó ECONOMIC PROGRESS ŌĆó VIABILITY OF PROJECTS OTHER FUNCTIONS ŌĆó EXPANSION OF FOREIGN TRADE ŌĆó ENCOURAGES SAVINGS ŌĆó CHECK INFLATION ŌĆó SELF CONFIDENCE & GOODWILL ŌĆó SOCIAL SECURITY ŌĆó CREDIT FACILITIES ŌĆó EMPLOYEES COOPERATION FUNCTIONS OF INSURANCE

- 9. PRE-REQUISITES FOR SUCCESS OF INSURANCE LIMITATIONS OF INSURANCE DOUBLE INSURANCE VS RE-INSURANCE DIY TASK

- 10. Double Insurance vs Re-insurance

- 11. THATŌĆÖS IT!!! NEXT: BASIC CONCEPT OF RISK

- 12. ? But waitŌĆ” ThereŌĆÖs More! Insurance and Risk

- 13. WhatŌĆÖs Your Message? CONCEPT OF RISK

- 14. MEANING OF RISK A PROBABILITY OR THREAT OF DAMAGE, INJURY, LIABILITY, LOSS, OR ANY OTHER NEGATIVE OCCURRENCE THAT IS CAUSED BY EXTERNAL OR INTERNAL VULNEREBILITIES, AND THAT MAY BE AVOIDED THROUGH PREEMPTIVE ACTION.

- 15. CHARACTERSTICS OF INSURABLE RISKS ŌĆó INSUREABLE INTEREST ŌĆó PURE AND MAJOR RISK ŌĆó CACULABLE RISKS ŌĆó MONETARY RISKS ŌĆó COMMON RISKS ŌĆó CASUAL RISK ŌĆó LEGAL RISK ŌĆó REAL RISK ŌĆó CATASTROPHIC RISK ŌĆó REASONABLE INSURANCE COST

- 16. CAUSES OF RISK CAUSES OF RISK NATURAL CAUSES SEASONAL CHANGES GEOGRAPHICAL CHANGES NATURAL CALAMITIES UNNATURAL CAUSES HUMAN CAUSES ECONOMIC CAUSES GOVT. POLICIES OTHER CAUSES

- 17. TYPES OF BUSINESS RISK FINANCIAL & NON- FINANCIAL RISKS PURE & SPECULATIVE RISKS DYNAMIC & STATIC RISKS FUNDAMENTAL & PARTICULAR RISKS TYPE OF BUSINESS RISK

- 18. TYPES OF RISKS ŌĆó FINANCIAL & NON-FINANCIAL: RISKS WHOSE OUTCOMES CAN BE MEASURED IN TERMS OF MONEY. ŌĆó PURE & SPECULATIVE: PURE RISK IS A CATEGORY OF HAZARD IN WHICH OUTCOMES ARE LOSS OR NO LOSS. SPECULATIVE RISK HAS THE OPPORTUNIT FOR LOSS OR GAIN. ŌĆó DYNAMIC & STATIC RISKS: DYNAMIC RISKS ARE THE OUTCOME OF THE CHANGES TAKING PLACE IN IN THE SOCIETY. ŌĆó FUNDAMENTAL & PARTICULAR RISKS: THE STRIKING PERCULIARITY OF FUNDAMENTAL RISK IS THAT IS INCIDENCE IS NON-DISCRIMINATORY AND FALLS ON EVERYBODY OR MOST OF THE PEOPLE. PR IS A RISK THAT AFFECTS ONLY AN INDIVIDUAL AND NOT EVERYONE IN THE COMMUNITY.

- 19. PURE RISKS PROPERTY RISK MOVABLE PROPERTY RISK IMMOVABLE PROPERTY RISK INDIRECT LOSS DIRECT LOSS LIABILITY RISK PERSONAL RISK SICKNESS/ DISABILITY UNEMPLOYMENT PREMATURE DEATH OLD AGE

- 20. ŌĆó The identification, analysis and economic control of those risks that can threaten the assets or earning capacity of an enterprise is called risk assessment. ’ā╝ Identifying risk ’ā╝ Controlling it must be economical ’ā╝ Earning capacity ’ā╝ Measurement of risk ’ā╝ Selection of method of risk handling ’ā╝ Implementing the selected method ’ā╝ Evaluation & feedback RISK ASSESSMENT

- 21. RISK TRANSFER: Risk transfer refers to an arrangement under which party exposed to risk transfers whole or part of losses consequential to risk exposure to another party for a consideration. RISK TRANSFER TECHNIQUES: Insurance Non-Insurance transfers Indemnity clause Hedging (price fluctuations) Warranty Incorporation Diversification

- 22. Dr. Neeraj Sharma BASIC PRINCIPLES OF INSURANCE

- 23. In order for the relationship between the insurer and the insured to work, there are certain principles that must be upheld. ŌĆó CAUSA PROXIMA ŌĆó SUBROGATION ŌĆó MITIGATION OF LOSSES ŌĆó CONTRIBUTION ŌĆó INSURABLE INTEREST ŌĆó UTMOST GOOD FAITH ŌĆó INDEMNITY ŌĆó FULL DISCLOSURE

- 24. INSURABLE INTEREST ŌĆó Insurable interest means that the person opting for insurance must have pecuniary interest in the property he is going to get insured and will suffer financial loss on the occurrence of the insured event. ŌĆó This is one of the essential requirements of any insurance contract. ŌĆó Therefore , a person can go for insurance of only those properties where he stands to benefit by the safety of the property, and will suffer loss, damage, injury if any harm takes place to such property.

- 25. ŌĆó If the house you own is damaged by fire, the value of your house has been reduced by the damages sustained in the fire. ŌĆó Whether you pay to have the house rebuilt or you and up selling it at a reduced price. You have to suffered a financial loss resulting from the fire. ŌĆó By contrast, if your neighborŌĆÖs house, which you do not own, is damaged by fire, you may feel sympathy for your neighbor and you may even be emotionally upset, but you have not suffered a financial loss from the fire, but in this example you do not have an insurable interest in your neighborŌĆÖs house. EXAMPLE

- 26. UBERRIMA FIDES Utmost good faith: The insurance contract must be based on good faith. If the insurance contract is obtained by way of fraud or misrepresentation it is void. When an individual apply for life insurance, it is important to answer all questions truthfully and to volunteer any information even if not asked, if in doubt, just disclose it. Failure to disclose material facts could render the entire contract void.

- 27. Example ŌĆóIf a person was suffering from sinusitis but did not disclose it, the entire contract could be cancelled when the insurer discover non- disclosure. ŌĆóCancellation of the entire contract means other non-related illnesses like cancer could no longer be covered. ŌĆóSome financial advisors who in their enthusiasm in closing the sale advice their clients not to disclose their pre-existing conditions for fear that the underwriter would reject the case. ŌĆó Therefore it is important to engage an ethical financial advisor. To avoid any conflict of interest, ensure you pay a fee for consultation.

- 28. FULL DISCLOSURE In the insurance contract, the proposer is required to disclose to the insurer all the material facts in respect of the proposed insurance. This duty of disclosing the material facts not only applies to the material facts which are known to him but also extends to material facts which he is supposed to know.

- 29. Examples ŌĆó Acquisition of new companies and/or mergers ŌĆó Changes to your business description. ŌĆó Additional product lines and/or new services ŌĆó Hazardous trade processes, or storage of hazardous matter, including changes or additions to processes or storage already declared ŌĆó Incidents not reported to insurers that might otherwise have led to a claim e.g. theft or small fires.

- 30. INDEMNITY ŌĆó The insurance contract should always be a contract of indemnity only and nothing more. ŌĆó Insured canŌĆÖt make any profit from the insurance contract. Insurance contract means for coverage of losses only. ŌĆó Indemnity means a guarantee to put the insured in the position as he was before accident. ŌĆó This principle does not apply to life insurance contracts. ŌĆó The main object of this principle is to ensure that the insured is not able to use this contract for speculation or gambling.

- 31. CONTRIBUTION In case the insured took more than one insurance policy for same subject matter, he/she canŌĆÖt make profit by making claim for same loss more than once. Z has a property worth Rs 5 lakhs. He took insurance from company A worth Rs. 3 lakhs and from company B ŌĆōRs 1 lakh. ŌĆó In case of accident, he incured a loss of Rs. 3 lakhs to the property. Raj can claim Rs 3 lakhs from company A but after then he canŌĆÖt make profit by making a claim from company B. ŌĆó Now company A can make a claim from company B to for proportional loss claim value.

- 32. SUBROGATION The principle is also known as ŌĆśDoctrine of Rights SubstitutionŌĆÖ. It is an extension of principle of indemnity. Subrogation is the transfer of rights and remedies of the insured in the subject matter (property) to the insurer after indemnification. The insurer steps into the shoes of the insured and become entitled to all rights of action against the third party to cover the loss from the responsible person regarding the subject matter of insurance claim of the insured has been fully settled and paid. The principle of subrogation refers to the right of the insurer to stand in the place of the insured after the settlement of claim. The insurer can recover the loss from the third party.

- 33. Example Suppose another driver runs a red light and your car is totaled. You have insurance on your car, so you call your insurance carrier and they pay you for all of your expenses related to the accident. ŌĆó Your insurance company realizing that the other driver had an insurance policy, then seeks reimbursement from the as fault partyŌĆÖs insurance carrier. ŌĆó Your insurer is ŌĆ£subrogatedŌĆØ to the rights of your policy and can ŌĆ£step in your shoesŌĆØ to recover any amount paid out on your behalf.

- 34. MITIGATION OF LOSS This principle states that the insured must take all the necessary steps to minimize the losses to insured assets. For example ŌĆō Ram took insurance policy for his house. In an cylinder blast, his house burnt. He should have called nearest fire station so that the loss could be minimized.

- 35. Word ŌĆ£Causa ProximaŌĆØ means ŌĆ£Nearest LossŌĆØ. An accident may be caused by more than one cause. In case property insured for only one cause. In such case nearest cause of the accident is fount out. Insurer pays the claim money only if the nearest cause is insured. CAUSA PROXIMA

- 36. Dr. Neeraj Sharma TYPES OF INSURANCE

- 37. TYPES OF INSURANCE ŌĆó LIFE INSURANCE ŌĆó FIRE INSURANCE ŌĆó MARINE INSURANCE ŌĆó SOCIAL INSURANCE ŌĆó MOTOR VEHICLE INSURANCE ŌĆó HEALTH INSURANCE ŌĆó LIABILITY INSURANCE ŌĆó MISCELLANEOUS INSURANCE Any risk that can be quantified can potentially be insured. Below are exhaustive lists of the many different types of insurance that exist

- 38. LIFE INSURANCE is a contract in which the insurer agrees to pay to the insured or his nominee the assured sum of money on the happening of a specified event i.e. death or expiry of certain period, in consideration of a certain premium. The life insurance provides protection to the family at the premature death of family head or gives adequate amount at the old age when earning capacities are reduced. Life insurance is not only a protection but is sort of investment because a certain sum is returnable to the insured at the expiry of a specified period. Life insurance is a tax-efficient method of saving as well as investment.

- 39. CHARACTERISTICS OF LIFE INSURANCE ŌĆó OUTCOME OF AN OFFER ŌĆó PAYMENT OF SUM ASSURED ŌĆó PAYMENT OF PREMIUM ŌĆó CONTRACT OF CONTINGENCY ŌĆó INSURABLE INTEREST ŌĆó FINANCIAL HELP ŌĆó ENCOURAGEMENT TO SAVINGS ŌĆó WIDER SCOPE

- 40. PROCEDURE FOR TAKING LIFE INSURANCE POLICY ŌĆó PROPOSAL ŌĆó PROOF OF AGE ŌĆó MEDICAL EXAMINATION ŌĆó CONFIDENTIAL REPORT BY AGENT ŌĆó ACCEPTANCE OF PROPOSAL ŌĆó PAYMENT OF FIRST PREMIUM ŌĆó INSURANCE POLICY

- 41. FIRE INSURANCE: is a contract of indemnity and the insured cannot claim anything more than the value of goods lost or damaged by fire or the amount insured, whichever is less. Characteristics of fire insurance: ŌĆó Contract of Indemnity ŌĆó Offer and acceptance ŌĆó Premium ŌĆó Insurable interest ŌĆó Payment of premium ŌĆó Policy duration ŌĆó Principle of subrogation ŌĆó Claim settlement

- 42. PROCEDURE OF FIRE INSURANCE ’āś Selecting the company ’āś Proposal form ’āś Evidence of Respectability ’āś Survey of properties to be insured ’āś Acceptance of proposal ’āś Cover Note ’āś Issue of Policy

- 43. MARINE INSURANCE: A marine insurance is a contract whereby one party for an agreed consideration, undertakes to indemnify the other against loss arising from certain perils and the risks to which a shipment and other interests in a marine adventure may be exposed during certain voyage or a certain time. Subject matter of marine insurance: ŌĆó Cargo Insurance ŌĆó Ship Insurance ŌĆó Freight Insurance

- 44. PROCEDURE OF MARINE INSURANCE ’āś SELECTION OF INSURANCE COMPANY ’āś MAKING THE OFFER ’āś ACCEPTANCE OF OFFER ’āś PAYMENT OF PREMIUM ’āś COVER NOTE ’āś ISSUE OF MARINE INSURANCE POLICY

- 45. SOCIAL INSURANCE is developed to provide economic security to weaker sections of the society who are unable to pay the premium for an adequate insurance. The main of social insurance is to help the community to fight against the risks of disease, old age, industrial accidents, unemployment and above all the evils of poverty. Various forms of social insurance are: ŌĆó Sickness Insurance ŌĆó Accident Insurance ŌĆó Disability Insurance ŌĆó Maternity Insurance ŌĆó Old Age Insurance ŌĆó Unemployment Insurance

- 46. MOTOR VEHICLE INSURANCE: Vehicle insurance (also known as car insurance, motor insurance or auto insurance) is insurance for cars, trucks, motorcycles, and other road vehicles. Its primary use is to provide financial protection against physical damage or bodily injury resulting from traffic collisions and against liability that could also arise from incidents in a vehicle. Vehicle insurance may additionally offer financial protection against theft of the vehicle, and against damage to the vehicle sustained from events other than traffic collisions, such as keying, weather or natural disasters, and damage sustained by colliding with stationary objects. The specific terms of vehicle insurance vary with legal regulations in each region.

- 47. Auto insurance in India deals with the insurance covers for the loss or damage caused to the automobile or its parts due to natural and man-made calamities. It provides accident cover for individual owners of the vehicle while driving and also for passengers and third party legal liability. Auto insurance in India is a compulsory requirement for all new vehicles used whether for commercial or personal use.

- 48. The auto insurance does not include: Consequential loss, depreciation, mechanical and electrical breakdown, failure or breakage When vehicle is used outside the geographical area War or nuclear perils and drunken driving. Types of Insurance Cover Liability only policy (Third party insurance) Package Policy

- 49. Third-party insurance This cover is mandatory in India under the Motor Vehicles Act, 1988. This cover cannot be used for personal damages. This is offered at low premiums and allows for third party claims under ŌĆ£no fault liability. The premium is calculated through the rates provided by the Tariff Advisory Committee. This is branch of the IRDA (Insurance Regulatory and Development Authority of India). It covers bodily injury/accidental death and property damage.

- 50. Health insurance is insurance that covers the whole or a part of the risk of a person incurring medical expenses, spreading the risk over a large number of persons. By estimating the overall risk of health care and health system expenses over the risk pool, an insurer can develop a routine finance structure, such as a monthly premium or payroll tax, to provide the money to pay for the health care benefits specified in the insurance agreement. The benefit is administered by a central organization such as a government agency, private business, or not-for-profit entity.

- 51. Liability insurance is insurance that provides protection against claims & lawsuits resulting from injuries and damage to people and/or property. Liability insurance policies cover both legal costs and any legal payouts for which the insured would be responsible if found legally liable. Intentional damage and contractual liabilities are typically not covered in these types of policies.

- 52. Liability insurance is critical for those who may be held legally liable for the injuries of others, especially medical practitioners and business owners. A product manufacturer may purchase product liability insurance to cover them if a product is faulty and causes damage to the purchasers or any other third party. Business owners may purchase liability insurance that covers them if an employee is injured during business operations.

- 54. MISCELLANEOUS ŌĆó Duty Insurance ŌĆó Erection All Risk Insurance ŌĆó Machinery Breakdown Insurance ŌĆó Cash Insurance ŌĆó Business premises burglary insurance ŌĆó Cattle Insurance ŌĆó Plantation/ horticulture insurance

- 56. REINSURANCE It is the transaction in which one insurer agrees, for a premium, to indemnify another insurer against all or part of the loss that insurer may sustain under its policy or policies of insurance. In the process of reinsurance the real insurer who transfers a portion of the risk is known as ceding insurer and the company selling reinsurance is known as the assuming insurer or reinsure.

- 57. METHODS OF REINSURANCE ŌĆó FACULTATIVE METHOD ŌĆó TREATY METHOD ’ü▒ QUOTA TREATY ’ü▒ SURPLUS TREATY ’ü▒ EXCESS OF LOSS TREATY ’ü▒ EXCESS OF LOSS RATIO TREATY ŌĆó POOLONG METHOD

- 58. DR. NEERAJ SHARMA RISK & RETURN RELATIONSHIP

- 59. RISK: REFERS TO POSSIBILITY OR CHANCE OF MEETING A DANGER OR CHANCE OF EXPOSURE TO ADVERSITY OR DANGER. THE RISK CAN BE THOUGHT OF AS THE DEGREE OF VARIATIONS IN THE POSSIBLE OUTCOME FROM AN UNCERTAIN EVENT, OR AS THE VARAITON IN THE POSSIBLE OUTCOME. RETURN: IT IS THE BENEFIIT FROM THE VENTURE. ONE OF THE PRIME MOTIVES OF THE INVESTMENT IS TO EARM AND MAXIMISE THE RETURN. RETURNS ON INVESTMENT MAY BE DUE TO INCOME, CAPITAL APPRECIATION OR POSITIVE HEDGE AGAINST INFLATION. IT IS THE PRINCIPAL REWARD IN INVESTENT PROCESS.

- 60. CAUSES OF RISK ŌĆó WRONG METHOD OF INVESTMENT ŌĆó WRONG TIMING OF INVESTMENT ŌĆó WRONG QUANTITY OF INVESTMENT ŌĆó NATURE OF INVESTMENT INSTRUMENTS ŌĆó NATURE OF INDUSTRY IN WHICH COMPANY IS OPERATING ŌĆó MATURITY PERIOD OF INVESTMENT ŌĆó TERMS OF LENDING ŌĆó NATIONAL AND INTERNATIONAL FACTORS

- 61. TYPES OF RISK SYSTEMATIC RISK ŌĆó MARKET RISK ŌĆó INTEREST RATE RISK ŌĆó PURCHASING POWER RISK UNSYSTEMATIC RISK ŌĆó BUSINESS RISK ŌĆó FINANCIAL RISK ŌĆó CREDIT OR DEFAULT RISK

Editor's Notes

- #1: This presentation demonstrates the new capabilities of PowerPoint and it is best viewed in ║▌║▌▀Ż Show. These slides are designed to give you great ideas for the presentations youŌĆÖll create in PowerPoint 2010! For more sample templates, click the File tab, and then on the New tab, click Sample Templates.