Introduction To Risk Aversion

- 1. Introduction to Risk Aversion in Enterprise Risk Management Presented by: John Lehman Managing Director SDG-Galway Energy Strategy Practice 22 March 2011

- 2. There are (at least*) three standards for ERM, and their treatments of risk and risk aversion differ. Casualty Actuarial Society (CAS) ŌĆō ŌĆĢOverview of Enterprise Risk ManagementŌĆØ (2003) ŌĆó Does not define risk. ŌĆó Makes virtually no mention of attitude toward risk. Corporations are implicitly assumed risk neutral. Committee of Sponsoring Organizations (COSO) ŌĆō ŌĆĢEnterprise Risk Management ŌĆō Integrated FrameworkŌĆ¢ (2004) ŌĆó ŌĆ£Risk ŌĆō The possibility that an event will occur and adversely affect the achievement of objectivesŌĆØ. ŌĆó ŌĆ£Risk appetite: The broad-based amount of risk a company or other entity is willing to accept in pursuit of its mission (or vision).ŌĆØ ŌłÆ ŌĆ£Risk appetite, established by management with oversight of the board of directors, is a guidepost in strategy setting.ŌĆØ ŌĆó ŌĆ£Risk tolerances are the acceptable levels of variation relative to the achievement of objectives.ŌĆØ ŌĆó Risk appetite is treated as a prior, fixed limit within which decisions are made. *RIMS had a standard for Risk Management, but appears to have adopted ISO31000. ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 1

- 3. There are three standards for ERM, and their treatments of risk and risk aversion differ. International Standards Organization (ISO) ŌĆō ŌĆ£ISO 31000 Risk Management ŌĆö Principles and GuidelinesŌĆ¢ (2009) ŌĆó Risk ŌĆō ŌĆ£Effect of uncertainty on objectivesŌĆØ. ŌĆó Risk Attitude ŌĆō ŌĆ£OrganizationŌƤs approach to assess and eventually pursue, retain, take or turn away from riskŌĆØ. ŌĆó Risk Appetite ŌĆō ŌĆ£Amount and type of risk that an organization is willing to pursue or retainŌĆØ. ŌĆó Risk Tolerance ŌĆō ŌĆ£Organization's or stakeholder's readiness to bear the risk after risk treatment in order to achieve its objectivesŌĆØ. ŌĆó Risk Aversion ŌĆō ŌĆ£Attitude to turn away from riskŌĆØ. ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 2

- 4. Your textbook adds a few other definitions into the mix. From Chapter 9 ŌĆō ŌĆ£How to Create and Use Corporate Risk ToleranceŌĆØ ŌĆó ŌĆ£Risk is commonly referred to as the chance, possibility, or uncertainty of outcome or consequences.ŌĆØ ŌĆó ŌĆ£ŌĆ”risk exposures are simply the extent to which you are exposed to a riskŌĆ”ŌĆØ ŌĆó ŌĆ£ŌĆ”risk toleranceŌĆ”is the risk exposure an organization determines is appropriate to take or avoid taking.ŌĆØ o ŌĆ£ŌĆ”you need to understand the concept of ŌĆ£appropriateŌĆØ. Determining what is appropriate requires applying judgment.ŌĆØ ŌĆó ŌĆ£Risk attitude is a personŌƤs propensity to take risk.ŌĆØ o ŌĆ£The term ŌĆ×personŌƤ should be read to include an individual, group of individuals, or an organization.ŌĆØ So what are we to believe? ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 3

- 5. If weŌĆÖre going to manage risk, itŌĆÖs a good idea to know what it is! ŌĆ£Risk is uncertainty with the potential for ex post regret.ŌĆØ ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 4

- 6. LetŌĆÖs begin with a brief history of rational decision- making, starting with Blaise Pascal and expected value. ŌĆó Blaise Pascal was instrumental in developing the mathematics of probabilities, particularly as applied to games of chance. ŌĆó In 1654, Pascal tackled the ŌĆ£Problem of PointsŌĆØ, which dealt with the proper way of dividing the stakes of a game that was interrupted prior to completion. ŌĆó From this Pascal developed the mathematical concept of ŌĆ£expected valueŌĆØ and suggested that the standard for rational decision making was expected value maximization. ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 5

- 7. The mathematically rigorous treatment of risk began with Daniel Bernoulli in 1738. ŌĆó Bernoulli attempted to explain the St. Petersburg Paradox which involved observed behavior when people were offered the chance to play a game with an infinite expected value. ŌĆó It was noted that people would only pay small amounts to play the game, showing that they were not acting on expected values. ŌĆó Bernoulli developed ŌĆ£expected utility theoryŌĆØ: ŌłÆ ŌĆ£The determination of the value of an item must not be based on the price, but rather on the utility it yieldsŌĆ”. There is no doubt that a gain of one thousand ducats is more significant to the pauper than to a rich man though both gain the same amount.ŌĆØ ŌĆó Bernoulli referred to mathematical utility functions, even suggesting one, log utility, that would resolve the St. Petersburg Paradox. ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 6

- 8. In 1944 John Von Neumann and Oskar Morgenstern advanced expected utility theory when they defined ŌĆ£rational choiceŌĆØ axiomatically. ŌĆó Von Neumann and Morgenstern asserted four principals or ŌĆ£axiomsŌĆØ of rational choice: transitivity, completeness, independence and continuity. ŌĆó Adherence to these four principals define Von Neumann-Morgenstern rationality, which allows the behavior of a rational agent to be described by reference to a ŌĆ£utility functionŌĆØ. ŌĆó For a rational agent as defined by Von Neumann-Morgenstern, risk aversion is a result of diminishing marginal utility for wealth, as Bernoulli suggested in 1738. ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 7

- 9. If your wealth-impacting decisions follow the von Neuman-Morgenstern axioms, we can define a utility function for you. How do we define ŌĆ£utilityŌĆØ? What is it? Where does it come from? ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 8

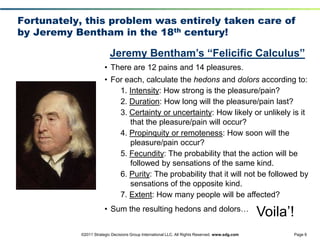

- 10. Fortunately, this problem was entirely taken care of by Jeremy Bentham in the 18th century! Jeremy BenthamŌĆÖs ŌĆ£Felicific CalculusŌĆØ ŌĆó There are 12 pains and 14 pleasures. ŌĆó For each, calculate the hedons and dolors according to: 1. Intensity: How strong is the pleasure/pain? 2. Duration: How long will the pleasure/pain last? 3. Certainty or uncertainty: How likely or unlikely is it that the pleasure/pain will occur? 4. Propinquity or remoteness: How soon will the pleasure/pain occur? 5. Fecundity: The probability that the action will be followed by sensations of the same kind. 6. Purity: The probability that it will not be followed by sensations of the opposite kind. 7. Extent: How many people will be affected? ŌĆó Sum the resulting hedons and dolorsŌĆ” VoilaŌƤ! ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 9

- 11. So, accepting the notion that utility is not directly observable, calculable or comparable, letŌĆÖs keep goingŌĆ”* 0.4 utils 0.8 utils 1.3 utils 2.2 utils 4.1 utils * In the words of Kenneth Arrow, ŌĆ£Now here we have a serious problem that we have to face. LetŌƤs face it. And now, letŌƤs move on.ŌĆØ ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 10

- 12. The utility changes with each wealth increment, giving us the marginal utility of wealth. ŌĆ£WhatŌƤs risk got to do with it?ŌĆØ 4.1 utils 2.2 utils 1.3 utils 0.8 utils ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 11

- 13. Our subject has diminishing marginal utility for wealth, so letŌĆÖs offer her a 50/50 gamble. 6.8 utils ┬Į of total distance ┬Į of total 50%(1) + 50%(6) = 3.5 distance The outcome The outcome if she loses. if she wins. 2.35 3.5 Certain Equivalent ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 12

- 14. Next weŌĆÖll look at a subject with increasing marginal utility for wealth. What happens to people like this? 1.5 utils 3.5 4.35 Certain Equivalent ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 13

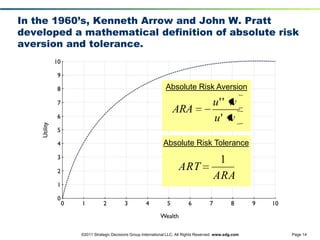

- 15. In the 1960ŌĆÖs, Kenneth Arrow and John W. Pratt developed a mathematical definition of absolute risk aversion and tolerance. Absolute Risk Aversion u' ' w ARA u' w Absolute Risk Tolerance Absolute Risk Tolerance 1 ART ARA ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 14

- 16. ŌĆ£Birds do it, bees do itŌĆ”also apesŌĆØ A Modest Selection of Papers Takahashi, T.; ŌĆ£Biophysics of risk aversion based on neurotransmitter receptor theoryŌĆØ, Neuro Endocrinology Letters, 2008 Aug;29(4):399-404. Lee, D.; ŌĆ£Neuroeconomics: making risky choices in the brainŌĆØ, Nature Neuroscience, 2005 Sep;8(9):1129-30. Caraco,Thomas; ŌĆ£Aspects of risk-aversion in foraging white-crowned sparrowsŌĆØ Animal Behaviour, Volume 30, Issue 3, August 1982, Pages 719-727. Marsh, B. & Kacelnik, A.; ŌĆ£Framing effects and risky decisions in starlingsŌĆØ Proceedings of the National Academy of Science, USA, 2002, 99, 3352ŌĆō3355. Real, Leslie A.; ŌĆ£Animal Choice Behavior and the Evolution of Cognitive ArchitectureŌĆØ, Science, 30 August 1991, 980-986. Heilbronner, Sarah R., Alexandra G. Rosati, Jeffrey R. Stevens, Brian Hare and Marc D. Hauser; ŌĆ£A fruit in the hand or two in the bush? Divergent risk preferences in chimpanzees and bonobosŌĆØ, Biology Letters, (2008) 4, 246ŌĆō249. ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 15

- 17. Now, letŌĆÖs change direction and ask a couple of simple questions. What is a corporation? ŌĆó ŌĆ£The private corporation or firm is simply one form of legal fiction which serves as a nexus for contracting relationships and which is also characterized by the existence of divisible residual claims on the assets and cash flows of the organizationŌĆ”ŌĆØ* Why do corporations exist? ŌĆó Adopting the corporate form lowers the costs of contracting between and among the owners of factors of production/claimants to the assets and cash flows of the organization. What is the role of corporate equity holders? ŌĆó Equity holders own the residual value of the corporation ŌĆō they are residual claimants ŌĆō and thus bear the bulk of the business risk of the organization. For whom does the management of a public corporation work? *Jensen, Michael and William Meckling; ŌĆ£Theory of the Firm: Managerial Behavior, Agency Costs and Ownership StructureŌĆØ, Journal of Financial Economics, October, 1976, V. 3, No. 4, pp. 305-360 ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 16

- 18. LetŌĆÖs summarize what we have learned thus far and ask a few critical questions. ŌĆó Risk aversion is strictly a function of diminishing marginal utility. ŌĆó Utility is not directly observable, calculable or comparable across individuals. ŌĆó There are mathematical definitions of risk aversion and risk tolerance. ŌĆó Risk aversion is found in humans and other animals and appears to have origins in natural selection. (Competition weeds out risk preferrers.) ŌĆó The mechanism by which risk aversion becomes manifest appears to be neurochemical. ŌĆó Corporations are legal fictions that serve as connecting points for contracts among providers of factors of production. ŌĆó Corporations exist to lower the costs of contracting among these providers. ŌĆó Equity owners are ŌĆ£residual claimantsŌĆØ to corporate assets and cash flows. ŌĆó Residual claimants provide risk-bearing service to the other claimants to the firmŌƤs assets and cash flows. ŌĆó Management acts on behalf of the equity owners/residual claimants. ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 17

- 19. When we speak of the ŌĆ£risk aversionŌĆØ of a corporation, what in the #%$@ are we talking about? ŌĆó Risk aversion is strictly a function of diminishing marginal utility. ŌĆó Utility is not directly observable, calculable or comparable across individuals. ŌĆó There are mathematical definitions of risk aversion and risk tolerance. ŌĆó Risk aversion is found in humans and other animals and appears to have origins in natural selection. (Competition weeds out risk preferrers.) ŌĆó The mechanism by which risk aversion becomes manifest appears to be neurochemical. ŌĆó Corporations are legal fictions that serve as connecting points for contracts among providers of factors of production. ŌĆó Corporations exist to lower the costs of contracting among these providers. ŌĆó Equity owners are ŌĆ£residual claimantsŌĆØ to corporate assets and cash flows. ŌĆó Residual claimants provide risk-bearing service to the other claimants to the firmŌƤs assets and cash flows. ŌĆó Management acts on behalf of the equity owners/residual claimants. ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 18

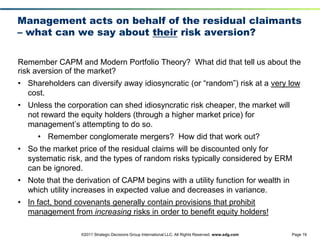

- 20. Management acts on behalf of the residual claimants ŌĆō what can we say about their risk aversion? Remember CAPM and Modern Portfolio Theory? What did that tell us about the risk aversion of the market? ŌĆó Shareholders can diversify away idiosyncratic (or ŌĆ£randomŌĆØ) risk at a very low cost. ŌĆó Unless the corporation can shed idiosyncratic risk cheaper, the market will not reward the equity holders (through a higher market price) for managementŌƤs attempting to do so. ŌĆó Remember conglomerate mergers? How did that work out? ŌĆó So the market price of the residual claims will be discounted only for systematic risk, and the types of random risks typically considered by ERM can be ignored. ŌĆó Note that the derivation of CAPM begins with a utility function for wealth in which utility increases in expected value and decreases in variance. ŌĆó In fact, bond covenants generally contain provisions that prohibit management from increasing risks in order to benefit equity holders! ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 19

- 21. To see how increasing risk might help shareholders, letŌĆÖs look at a simplified example of a corporation. For our example we will look at an imaginary company that holds a single asset and a single liability. ŌĆó Asset: 10,000mmbtus of natural gas to be delivered exactly one year from today. ŌĆó Liability: An obligation to pay exactly $30,000 in one year from today (i.e. $3.00/mmbtu in the forward contract). ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 20

- 22. First, letŌĆÖs take assume that there is no risk in the value of the contract at expiration. Forward Purchase of Natural Gas ŌĆó The firm has a single asset, a forward natural gas contract for delivery of 10,000 mmbtus of gas in exactly one year. ŌĆó Upon delivery, the firm is obligated to make a payment of $30,000. ŌĆó The riskless rate of interest is 5.0%. ŌĆó The gas will be sold at the spot price immediately upon receipt. ŌĆó The current one-year forward price of natural gas is $3.50. The present value of the Zero-Risk Balance Sheet $30,000 obligation Assets Liabilities and Equity discounted at the riskless Cash $0 $28,537 Debt rate. Forward Contract $33,293 $4,756 Equity Total $33,293 $33,293 Total Price of $3.50 times 10,000 mmbtuŌƤs The asset value less the discounted at the riskless rate. value of the debt. ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 21

- 23. To see how increasing risk might help shareholders, letŌĆÖs look at a simplified example of a corporation. For our example we will look at an imaginary company that holds a single asset and a single liability. ŌĆó Asset: 10,000mmbtus of natural gas to be delivered exactly one year from today. ŌĆó Liability: An obligation to pay exactly $30,000 in one year from today (i.e. $3.00/mmbtu in the forward contract). While the approach we will illustrate is perfectly general, this simplified example will allow us to focus on the result of changing risk levels rather than the details of risk assessment, measurement, etc. ŌĆó The company is subject to a single risk ŌĆō the risk that the price of natural gas in one year will change from todayŌƤs observed forward price. ŌĆó The metric for price risk on such contracts has been standardized (volatility) and can, in many instances, be derived directly from the market. ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 22

- 24. Next we will introduce risk in the form of random price volatility of 35%. Using option pricing, we develop a market value balance sheet. Asset Value ŌĆō Equity Value Market Value Balance Sheet Assets Liabilities and Equity Cash $0 $26,215 Debt Forward Contract $33,293 $7,078 Equity Total $33,293 $33,293 Total The value of a one-year call option on a forward contract with: Price of $3.50 times 10,000 mmbtuŌƤs discounted at the riskless rate. ŌĆó Strike Price = $3.00 x 10,000 mmbtus ŌĆó Volatility = 35% ŌĆó Riskless Rate = 5% ŌĆó Asset Value = $3.50 x 10,000 mmbtus ŌĆó The equity value is the value of an option, and the debt value is the PV of the future cash flows (at the riskless rate) less the extrinsic value of the equity option. ŌĆó The market value of the debt is $26,215 with the 35% volatility, which is $2,322 lower than the value without risk. The implied market debt yield here is 13.48% or 848 bps above the riskless rate. ŌĆó By increasing the asset volatility from 0% to 35% the shareholders have expropriated $2,322 of the debtholdersŌƤ wealth for themselves! ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 23

- 25. ŌĆ£So, we donŌĆÖt care about risk? ThatŌĆÖs nuts! I want my tuition back!ŌĆØ Please remain seated and try to stay calmŌĆ” ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 24

- 26. However we define ERM, it must be directed toward the maximization of shareholder wealth. There must be an understood causal relationship between the actions prescribed and the value of residual claims. Unsupported assertions of ŌĆ£corporate risk aversionŌĆØ do not suffice. Here are some candidates for value- adding risk management activities: ŌĆó Ideation ŌĆō Attempts to add value often focus on incremental revenue generation or high probability cost lowering (e.g. production rationalization). Actions that lower the chance or severity of bad outcomes may have positive value but be overlooked. ŌĆó De-biasing ŌĆō Humans are prone to cognitive biases leading to over- optimism, many of which relate to the treatment of risks. ERM can formalize processes for de-biasing estimates and improve decision making. ŌĆó Cost of risk capital in strategic decisions ŌĆō Decisions of a scale sufficient to alter the probability of financial distress by definition involve corporate risk capital, whose cost is seldom recognized. ŌĆó Value of real options ŌĆō The value of management flexibility as resolution of uncertainty improves is often missed in analysis and implementation. ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 25

- 27. Introduction to Risk Aversion in Enterprise Risk Management Presented by: John Lehman Managing Director SDG-Galway Energy Strategy Practice 22 March 2011 ┬®2011 Strategic Decisions Group International LLC. All Rights Reserved. www.sdg.com Page 26