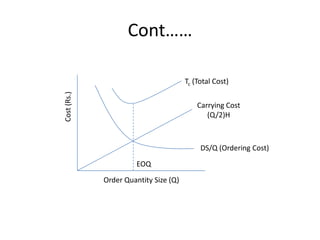

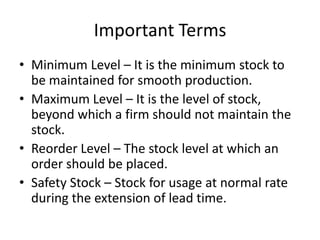

![Exampled=discount rate (.005)Discount on savings=dXPXA=(.005X50X1200) =300Savings on the ordering cost=(OA/Q)-(OA/q)Here Q=EOQ & q=discount quantity(400)=O[A/Q-A/q]=37.5[1200/300-1200/400] =37.5](https://image.slidesharecdn.com/fmppt-110221041250-phpapp02/85/inventory-control-ABC-analysis-ppt-34-320.jpg)

![ContĪŁĪŁNet return=[dPA+ savings on - additional discount] carrying cost =(300+37.5)-50 =287.5Here net return is +ve= firm should order 400 unit](https://image.slidesharecdn.com/fmppt-110221041250-phpapp02/85/inventory-control-ABC-analysis-ppt-36-320.jpg)

inventory control & ABC analysis ppt

- 2. INTRODUCTIONSignificant part of the current assetLarge amount of inventory leads to considerable lapse of fundImperative to manage to avoid unnecessary investment

- 3. ContĪŁĪŁĪŁ..Inventory Control measure and regulate to predetermine -size for order or production, -safety stock - minimum level of order - maximum level of order

- 4. Nature of inventoriesRaw materialWork in processFinished goods

- 5. NEED TO HOLD INVENTORIESTransaction motive(smooth production)Precautionary motive(demand)Production motive (price)

- 6. PRODUCTION CYCLETime span between introduction raw material to the conversion into the finished product

- 7. OBJECTIVE OF INVENTORY MANAGEMENTTo meet unforeseen future demand due to variation in forecast figures and actual figures.To meet the customer requirement timely, effectively, efficiently and smoothly To smoothen the production process.To facilitate intermittent production of several products on the same facility.

- 8. ContĪŁĪŁ..To gain economy of production or purchase in lots.To reduce loss due to changes in prices of inventory items.To meet the time lag for transportation of goods.To balance various costs of inventory such as order cost or set up cost and inventory carrying cost

- 9. ContĪŁĪŁ..To balance the stock out cost/opportunity cost due to loss of sales against the costs of inventory.To minimize losses due to deterioration, obsolescence, damage etc.

- 10. Optimum level of inventoryIt lies between two danger point,i.e between excessive and inadequate level

- 11. Major danger in the overinvesmentUnnecessary tie-up of firmĪ»s fund and loss of profitExcessive carrying costRisk of liquidity

- 12. Major danger in the inadequate levelProduction hold-upFailure to meet delivery commitment

- 13. Effective inventory managementContinues supply of raw material to facilitate productionMaintain sufficient stock of raw materials in periods of short supply and anticipate price changesMaintain sufficient finished goods inventory for smooth sales operation, and efficient customer service

- 14. ContĪŁĪŁ..Minimise the carrying cost and timeControl investment in inventories and keep it an optimum level

- 15. Inventory management techniquesAim to maximise the shareholder wealth For efficient inventory management, we have to answer -how much should be ordered ? (ans;EOQ) -when should it be ordered ? (ans;reorder point)

- 16. Economic order quantityordering materials whenever stock reaches the reorder pointIt tells how production to be schedule optimum level of inventory involves two types of cost 1.ordering cost 2.carrying cost

- 17. Ordering costIt is the entire cost to acquire the raw material(supplies).It include -Requisitioning -order placing -Transportation -Receiving, inspecting and storing -clerical and staff

- 18. Carrying costIt is the cost incurred to maintain the given level of inventoryIt include -Warehousing -Handling -clerical and staff -Insurance -Deterioration and obsolescene

- 19. Ordering and carrying cost trade offOptimum level of inventory referred to EOQTo determine EOQ-three approaches -Trial and error approach -Formula approach -Graphical approach

- 20. Trial and error approachAssumptions -known annual requirement -steady usage -ordering and carrying cost to be constant through the entire period

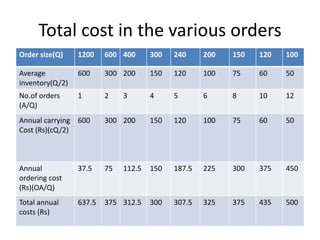

- 21. Example ©C illustrating the trial and error approachEstimated annual requirement, A =1200unitPurchasing cost per unit, P(Rs) =50Ordering cost (per order),O(Rs) =37.50Carrying cost per unit,c(Re) =1

- 22. Total cost in the various orders

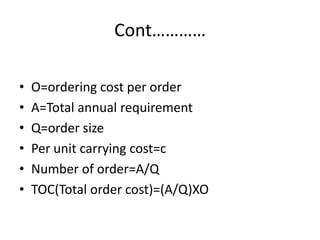

- 23. Inference from the TC tableOrderTotal cost 1.For single order(once in year) 637.52.12 order (once in a month) 5003.4 order(once in every 3 month) 300i.e.the third option is the most economic

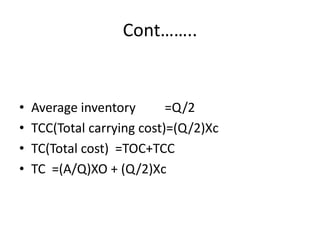

- 24. Order formula approach It is more easier way compared to trial and error approach Assumption -carrying cost per unit constant -ordering cost per order fixed

- 25. ContĪŁĪŁĪŁĪŁO=ordering cost per orderA=Total annual requirementQ=order sizePer unit carrying cost=cNumber of order=A/QTOC(Total order cost)=(A/Q)XO

- 26. ContĪŁĪŁ..Average inventory =Q/2TCC(Total carrying cost)=(Q/2)XcTC(Total cost) =TOC+TCCTC =(A/Q)XO + (Q/2)Xc

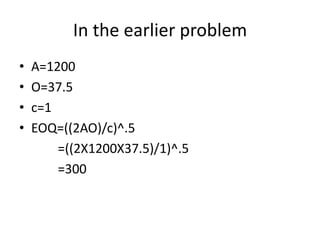

- 27. Inference from the equationFor larger quantity order =carrying cost increases =ordering cost decreasesFor lower quantity order=carrying cost decreases =ordering cost increase

- 28. ContĪŁĪŁĪŁ.EOQ should lie between larger & lower quantity orderSo EOQ = differentiate TC and equate to zeroTC =(A/Q)XO + (Q/2)XcEOQ=-(AO)/Q^2+c/2=0c/2=(AO)/Q^2EOQ=Q=((2AO)/c)^.5

- 29. In the earlier problemA=1200O=37.5c=1EOQ=((2AO)/c)^.5 =((2X1200X37.5)/1)^.5 =300

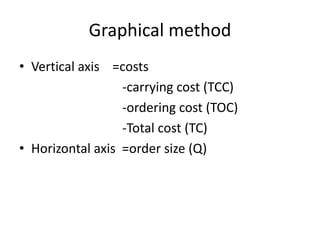

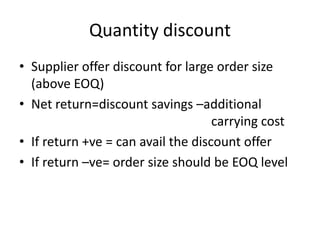

- 30. Graphical methodVertical axis =costs -carrying cost (TCC) -ordering cost (TOC) -Total cost (TC)Horizontal axis =order size (Q)

- 31. ContĪŁĪŁTc (Total Cost)Carrying Cost (Q/2)HCost (Rs.)DS/Q (Ordering Cost)EOQOrder Quantity Size (Q)

- 32. ContĪŁĪŁCarrying cost increases with increase order size, because of large have to be maintainedOrdering cost decline with increase in order size, because larger order size means lesser no of orderTotal cost has the behaviour of both ordering cost and carrying costEOQ=deviating point of TC

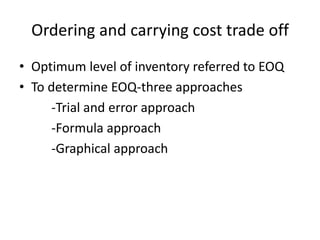

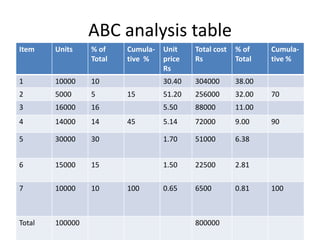

- 33. Quantity discountSupplier offer discount for large order size (above EOQ)Net return=discount savings ©Cadditional carrying costIf return +ve = can avail the discount offer If return ©Cve= order size should be EOQ level

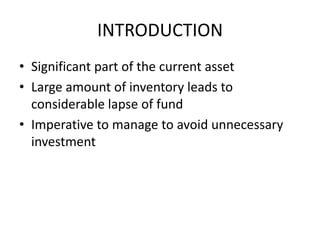

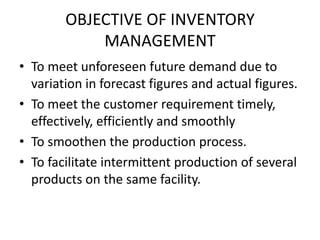

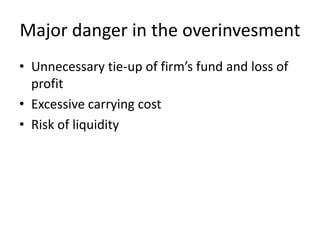

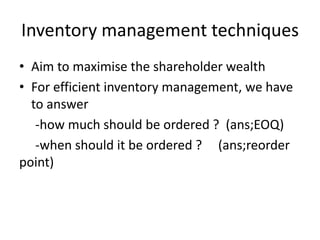

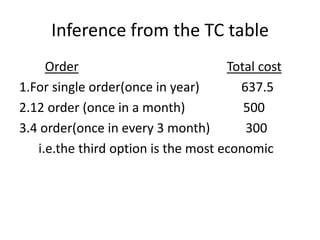

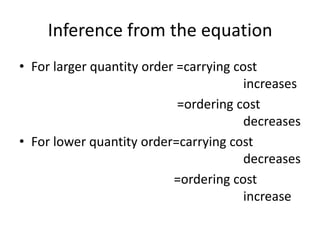

- 34. Exampled=discount rate (.005)Discount on savings=dXPXA=(.005X50X1200) =300Savings on the ordering cost=(OA/Q)-(OA/q)Here Q=EOQ & q=discount quantity(400)=O[A/Q-A/q]=37.5[1200/300-1200/400] =37.5

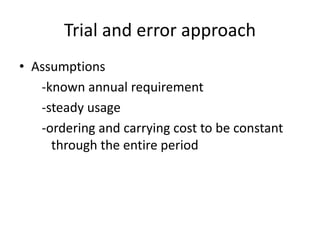

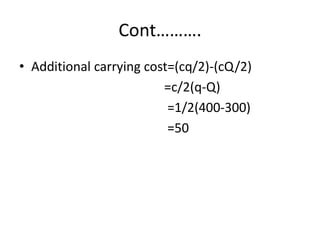

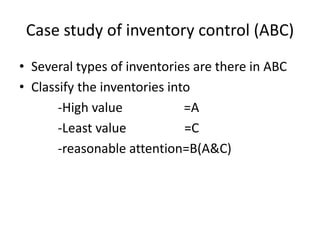

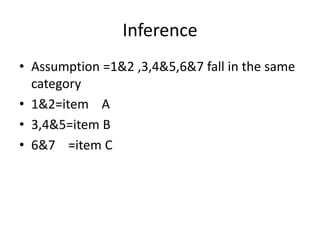

- 35. ContĪŁĪŁĪŁ.Additional carrying cost=(cq/2)-(cQ/2) =c/2(q-Q) =1/2(400-300) =50

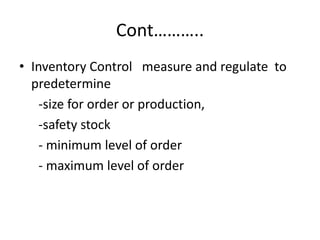

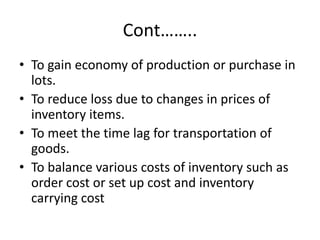

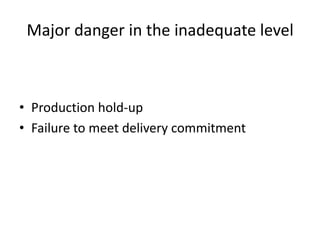

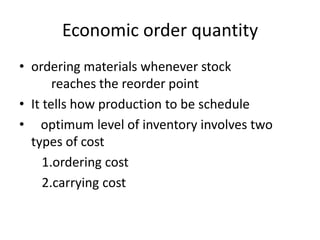

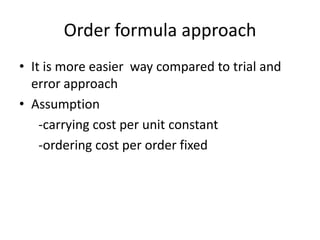

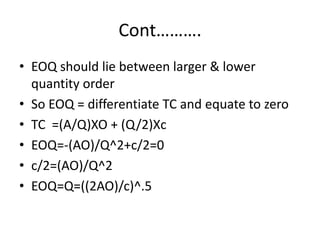

- 36. ContĪŁĪŁNet return=[dPA+ savings on - additional discount] carrying cost =(300+37.5)-50 =287.5Here net return is +ve= firm should order 400 unit

- 37. Important TermsMinimum Level ©C It is the minimum stock to be maintained for smooth production.Maximum Level ©C It is the level of stock, beyond which a firm should not maintain the stock.Reorder Level ©C The stock level at which an order should be placed.Safety Stock ©C Stock for usage at normal rate during the extension of lead time.

- 38. Case study of inventory control (ABC)Several types of inventories are there in ABCClassify the inventories into -High value =A -Least value =C -reasonable attention=B(A&C)

- 39. ContĪŁĪŁ.ABC analysis concentrate on important items =Control by important exception(CIE)Classified in the importance of their relative value=Proportion Value Analysis(PVA)

- 40. Step involved in implementing the ABC analysisClassify ,determine expected use & price of the inventoriesDetermine total value of item(expected unitXunit price)Rank the items (according to total value)Compute the ratios (no.of unit/total unit) & (each value of item/total value of all item)Combine on the basis of relative values (A,B,C)

- 42. Inference Assumption =1&2 ,3,4&5,6&7 fall in the same category1&2=item A3,4&5=item B6&7 =item C