LEDGER ACCOUNTS.pptx

Download as pptx, pdf50 likes330 views

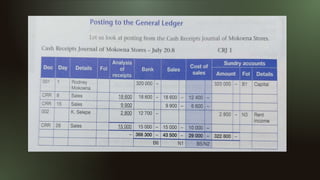

This document discusses posting cash transactions from a Cash Receipts Journal to a general ledger. It recaps the accounting cycle and double entry principle. It explains that on the last day of the month, the totals from all columns except analysis of receipts in the Cash Receipts Journal are posted to the general ledger. Individual entries in the sundry accounts column are posted on the day the transaction occurs. It then provides an example of posting a total from the Cash Receipts Journal for the bank to the bank account in the general ledger.

LEDGER ACCOUNTS.pptx

- 2. RecapâĶ âĒ Accounting cycle âĒ Double entry principle âĒ Sections within the General ledger

- 3. In this unit you will âĒ Learn about the posting of cash transactions of a trading business from Cash Receipts Journal (CRJ) to the general ledger

- 4. Posting transactions from the CRJ to the General Ledger âĒ Cash Receipts Journal âĒ On the last day of the month, the total of all columns excluding analysis of receipts, for example, bank, and sales, is posted to the general ledger. âĒ In the sundry accounts column, entries are individually posted on the day the transaction occurs.

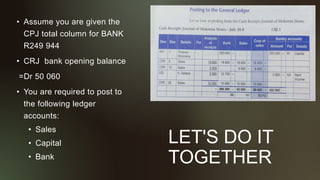

- 6. LET'S DO IT TOGETHER âĒ Assume you are given the CPJ total column for BANK R249 944 âĒ CRJ bank opening balance =Dr 50 060 âĒ You are required to post to the following ledger accounts: âĒ Sales âĒ Capital âĒ Bank

- 8. MEMO- Sales 20.8 Jul 31 Bank CRJ 43 500

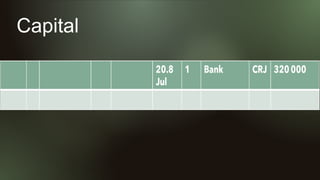

- 9. Capital

- 10. Bank