Lifting Cost Rig Count Oil1 (2) (4) (2)

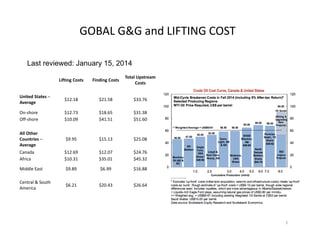

- 1. Lifting┬ĀCosts Finding┬ĀCosts Total┬ĀUpstream┬Ā Costs United┬ĀStates┬ĀŌĆō Average $12.18 $21.58 $33.76 OnŌĆÉshore $12.73 $18.65 $31.38 OffŌĆÉshore $10.09 $41.51 $51.60 All┬ĀOther┬Ā Countries┬ĀŌĆō Average $9.95 $15.13 $25.08 Canada $12.69 $12.07 $24.76 Africa $10.31 $35.01 $45.32 Middle┬ĀEast $9.89 $6.99 $16.88 Central┬Ā&┬ĀSouth┬Ā America $6.21 $20.43 $26.64 GOBAL┬ĀG&G┬Āand┬ĀLIFTING┬ĀCOST Last reviewed: January 15, 2014 1

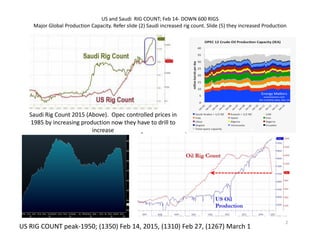

- 2. US┬Āand┬ĀSaudi┬Ā┬ĀRIG┬ĀCOUNT;┬ĀFeb┬Ā14ŌĆÉ DOWN┬Ā600┬ĀRIGS Major┬ĀGlobal┬ĀProduction┬ĀCapacity.┬ĀRefer┬Āslide┬Ā(2)┬ĀSaudi┬Āincreased┬Ārig┬Ācount.┬Ā║▌║▌▀Ż┬Ā(5)┬Āthey┬Āincreased┬ĀProduction┬Ā Saudi┬ĀRig┬ĀCount┬Ā2015┬Ā(Above).┬Ā┬ĀOpec controlled┬Āprices in┬Ā 1985┬Āby┬Āincreasing┬Āproduction┬Ānow┬Āthey┬Āhave┬Āto┬Ādrill┬Āto┬Ā increase US┬ĀRIG┬ĀCOUNT┬ĀpeakŌĆÉ1950;┬Ā(1350)┬ĀFeb┬Ā14,┬Ā2015,┬Ā(1310)┬ĀFeb┬Ā27,┬Ā(1267)┬ĀMarch┬Ā1 2

- 6. 6

- 7. 7

- 8. Costs A┬Āmajor┬Āfactor┬Āinfluencing┬Āthe┬Ācost┬Āof┬Āextraction┬Āis┬Āthe┬Ālifecycle┬Āof┬Āeach┬Ātype┬Āof┬Āoil┬Āsource.┬ĀSaudi┬Āwells┬Ālast┬Ālonger.┬ĀThere is more┬Āoil┬Āto┬Āpump┬Āwithin┬Āeach┬Ācavity┬Āand┬Āso┬Āthe┬Ācost┬Āof┬Āsetting┬Āup┬Āthat┬Ā well┬Ācan┬Ābe┬Āwritten┬Āoff┬Āover┬Āa┬Ālonger┬Āperiod┬Āthan┬Āthe┬Ācost┬Āof┬Āsetting┬Āup┬Āa┬Āfracking┬Āand┬Āhorizontal┬Ādrilling┬Āoperation.┬ĀA┬ĀlongŌĆÉterm┬Āproducer┬Ācan┬Āalso┬Āwrite┬Āoff┬Āthe┬Ācost┬Āof┬Ādistribution┬Āmethods┬Ā over┬Āa┬Ālonger┬Āperiod.┬ĀSo┬Āif┬Āa┬Ānew┬Āwell┬Ācan┬Ābe┬Ābuilt┬Āalongside┬Āexisting┬Āroads┬Āand┬Āpipelines,┬Āthat┬Āmethod┬Āwill┬Āend┬Āup┬Ācheaper┬Āin┬Āthe┬Ālong┬Ārun┬Āthan┬Āfracking┬Āin┬Āremote┬Āand┬Āpreviously┬Āunexplored┬Ā areas┬Āwhere┬Āa┬Ānew┬Āpipeline┬Āor┬Ārailroad┬Āinfrastructure┬Āadds┬Āto┬Āsetup┬Ācosts.┬Ā Staff┬Ācosts┬Āare┬Āhigher┬Āwith┬Āfracking┬Āmethods┬Ābecause┬Āeach┬Ādrilling┬Āsite┬Āis┬Ādistant┬Āfrom┬Āearlier┬Āsites.┬ĀAny┬Āoil┬Āextractor┬Āhas┬Āto┬Āspend┬Ātime┬Āand┬Āmoney┬Ālocating┬Āstaff┬Āfor┬Āeach┬Āproject.┬ĀThose┬Ā employees┬Āthen┬Āneed┬Āto┬Ābe┬Ātransported┬Āand┬Āhoused.┬ĀIf┬Āa┬Āwell┬Ālasts┬Āfor┬Ādecades,┬Āthe┬Āsame┬Āaccommodation┬Ācan┬Ābe┬Āused┬Āfor┬Āstaff┬Āover a┬Ālonger┬Āperiod┬Āthan┬Āthe┬ĀshortŌĆÉterm┬Ānature┬Āof┬Āeach┬Āfracking┬Ā location.┬ĀThe┬Āperipatetic┬Ānature┬Āof┬Āfracking┬Āalso┬Āmeans┬Āthat┬Āstaff┬Āwill┬Ābe┬Āless┬Ālikely┬Āto┬Āsettle┬Āin┬Āone┬Āplace┬Āwith┬Ātheir┬Āfamilies┬Āand┬Ātherefore┬Ādemand┬Āhigher┬Āwages┬Āto┬Ācompensate┬Āfor┬Āthe┬Ā loneliness┬Āof┬Āworking┬Āaway┬Āfrom┬Āhome┬Āin┬Āfreezing┬ĀŌĆÉ40F┬ĀNorth┬ĀDakota┬Āwinters.┬Ā Capacity Fracking┬Āis┬Āmore┬Āexpensive┬Āthan┬Āextracting┬Āoil┬Āby┬Āconventional┬Āmethods.┬ĀThus,┬Āconventional┬Āproducers┬Ācan┬Āafford┬Āto┬Ākeep┬Āextracting┬Āand┬Āselling┬Ātheir┬Āoil┬Āat┬Ālower┬Ācrude┬Āindex┬Āprices┬Āthan┬Ā frackers.┬ĀSo┬Āwhy┬Ābother┬Āinvesting┬Āin┬Āhydraulic┬Āfracturing┬Āand┬Āhorizontal┬Ādrilling?┬ĀA┬Āhigh┬Āoil┬Āprice┬Āoffers┬Āan┬Āincentive┬Āto┬Āendeavor.┬ĀAmerican┬Āoil┬Āexploration┬Āand┬Āextraction┬Ācompanies┬Āwould┬Ā much┬Ārather┬Āwork┬Āin┬Ātheir┬Āown┬Ācountry,┬Āand┬Āin┬Ātheir┬Āown┬Ālanguage,┬Āthan┬Āhave┬Āto┬Ātravel┬Āto┬Āunstable┬Āplaces┬Āand┬Ārisk┬Āhostile┬Ācultures┬Āin┬Āorder┬Āto┬Āmake┬Āa┬Āliving.┬ĀThus,┬ĀUS┬Āoil┬Ācompanies┬Āexpanded┬Ā production┬Āin┬Ātheir┬Āown┬Ācounty once┬Āprices┬Āreached┬Āa┬Ācertain┬Ālevel┬Āwhere┬Āunconventional┬Āmethods┬Ābecame┬Āeconomically┬Āviable.┬ĀFinanciers┬Āand┬Āinvestors┬Āhad┬Ālittle┬Ārisk┬Āof┬Ālosing┬Ātheir┬Ā investment.┬ĀThe┬ĀOPEC┬Ācountries consistently┬Ātrimmed┬Ātheir┬Āoutput┬Āto┬Āmatch┬Āworld┬Ādemand,┬Āso┬Āprojections┬Āof┬Āoil┬Āprices┬Āand┬Ārates┬Āof┬Āreturn┬Ācreated┬Āa┬ĀoneŌĆÉway┬Ābet.┬Ā American┬Āoil┬Āproducers┬Ācould┬Ājust┬Ākeep┬Āincreasing┬Ācapacity┬Āinfinitely┬Ā(or┬Āso┬Āit┬Āseemed),┬Ābecause┬Āsomeone┬Āelse┬Āwould┬Āadjust┬Ātheir output┬Āto┬Āmake┬Āroom┬Āin┬Āthe┬Āmarket.┬ĀProspects┬Ālooked┬Āgood┬Āfor┬Ā expansion┬Ābecause┬Ācutbacks┬Āin┬ĀOPEC┬Āproduction┬Āmeant┬ĀAmerica┬Ācould┬Ājust┬Ākeep┬Ātaking┬Āa┬Ālarger┬Āand┬Ālarger┬Āshare┬Āof┬Āthe┬Āmarket.┬Ā Circumstances The┬ĀSaudis┬Āand┬Ātheir┬ĀcheapŌĆÉoil┬ĀPersian┬ĀGulf┬Āneighbors┬Āsuddenly┬Āhad┬Āenough┬Āof┬Āmaking┬Āroom┬Āfor┬ĀAmerican┬Āexpansion.┬ĀThey┬Āknew┬Āthat┬Āthey┬Āhad┬Ābeen┬Āobliging┬Āto┬Āother┬Ānations,┬Ābut┬Āfelt┬Āthat┬Āthey┬Ā had┬Ānot┬Ābeen┬Ātreated┬Āwith┬Āthe┬Ācourtesies┬Āthat┬Āthey┬Ādeserved.┬ĀSaudi┬ĀArabia┬Āwas┬Āparticularly┬Āangry┬Āthat┬ĀAmerica┬Āand┬Āits┬ĀWestern allies┬Āhad┬Āfailed┬Āto┬Ātopple┬ĀBashar┬ĀalŌĆÉAssad┬Āin┬ĀSyria and┬Āthey┬Āwere┬Ā furious┬Āwith┬ĀRussia┬Āfor┬Āblocking┬Āinitial┬Āattempts┬Āto┬Āoust┬Āthe┬ĀSyrian┬Āpresident.┬ĀThe┬Āsudden┬Āreturn┬Āto┬Āmarket┬Āof┬ĀAlgeria,┬ĀLibya and┬ĀIraq┬Āmeant┬Āthat┬ĀOPEC┬Ābegan┬Āto┬Āoverproduce.┬ĀUnder┬Ānormal┬Ā circumstances,┬Āboth┬Āthis┬Āextra┬Āproduction┬Āand┬Āadded┬Ācapacity┬Āfrom┬Āfracking┬Āwould┬Āhave┬Āprompted┬Āthe┬ĀSaudis┬Āand┬Ātheir┬ĀOPEC┬Āallies┬Āto┬Āreduce┬Āproduction┬Āto┬Āmaintain┬Āprice┬Ālevels.┬ĀThis┬Āyear,┬Āthe┬Ā Saudis┬Āswitched┬Ātactics┬Āand┬Ādecided┬Āto┬Ādefend┬Ātheir┬Āmarket┬Āshare┬Āno┬Āmatter┬Āwhere┬Āthe┬Āprice┬Āwent.┬Ā Endgame A┬Āfalling┬Āoil┬Āprice┬Āpunishes┬ĀRussia and┬Ābrings┬Āeconomic┬Ārealities┬Āto┬Ācalculations┬Āover┬Āwhether┬Āto┬Āinvest┬Āin┬Āfurther┬Āoil┬Āexploration.┬ĀFortunately,┬Āthis┬Ātactic┬Āis┬Ānot┬Āthe┬Ādisaster┬Āit┬Āmight┬Āat┬Āfirst┬Āseem.┬Ā The┬Āsecond┬Āpart┬Āof┬Āany┬Āprice┬Ācalculation┬Ālies┬Āwith┬Ādemand┬Āfor┬Āa┬Āproduct.┬ĀAt┬Āthe┬Āsame┬Ātime┬Āthat┬Āoil┬Āsupply┬Āsurged,┬Ādemand┬Āfor┬Āoil dropped.┬ĀChina┬Āmaintained┬Āthe┬Āillusion┬Āof┬Āgrowth┬Āover┬Āthe┬Āpast┬Ā year┬Āby┬ĀoverŌĆÉordering┬Āraw┬Āmaterials.┬ĀNow┬Ā┬Āthey┬Āneed┬Āto┬Āabsorb┬Ātheir┬Āstocks,┬Āwhich┬Ātakes┬Āa┬Ālarge┬Āpart┬Āof┬Āworld┬Ādemand┬Āfor┬Āoil┬Āout┬Āof┬Āthe┬Āmarket.┬ĀEurope's┬Āgrowth┬Āis┬Āstuttering,┬Āremoving┬Āmore┬Ā demand.┬ĀEconomists┬Ācalculate┬Āthat┬Āfor┬Āevery┬Ā10%┬Ādrop┬Āin┬Āthe┬Āprice┬Āof┬Āoil,┬Āthe┬Āworld's┬ĀGDP┬Āwill┬Āgrow┬Āby┬Ā0.1%.┬ĀEvidently,┬Āthe┬Ācurrent┬Āfalls┬Āin┬Āoil┬Āprice┬Āwill┬Āeventually┬Ācorrect┬Āthe┬Ālack┬Āof┬Ādemand┬Āin┬Ā the┬Āmarket┬Āand┬Āsupply┬Āand┬Ādemand┬Āwill┬Āreturn┬Āto┬Āequilibrium.┬Ā Pricing Faced┬Āwith┬Ālack┬Āof┬Ādemand┬Āand┬Āfalling┬Āprices,┬Āany┬Ābusiness┬Āhas┬Āthree┬Āoptions:┬Ācarry┬Āon┬Āregardless;┬Āreduce,┬Āor┬Āsuspend┬Āproduction;┬Āor┬Ālower┬Ācosts.┬ĀSaudi┬ĀArabia┬Āchose┬Āoption┬Āone.┬ĀThis┬Āstrategy┬Ā relies┬Āon┬Āothers┬Āeither┬Āgoing┬Āout┬Āof┬Ābusiness,┬Āor┬Āsuspending┬Āoperations┬Āto┬Āreduce┬Āsupply.┬ĀThe┬ĀArabian┬Āproducers┬Ācan┬Āafford┬Āto pick┬Āthat┬Āoption┬Ābecause┬Āthey┬Āhave┬Āthe┬Ālowest┬Āproduction┬Ācosts┬Ā among┬Āall┬Āoil┬Āproducers.┬ĀAccording┬Āto┬ĀMorgan┬ĀStanley┬ĀCommodity┬ĀResearch,┬Āsome┬ĀMiddleŌĆÉEastern┬Āonshore┬Āproduction┬Ācan┬Ābreak┬Āeven┬Āat┬Ā$10┬Āper┬Ābarrel.┬ĀOthers┬Āin┬Āthat┬Āregion┬Āneed┬Āaround┬Ā$37┬Ā per┬Ābarrel,┬Āwith┬Āthe┬Āaverage┬Ābreakeven┬Āpoint┬Āfor┬Āonshore┬Āwells┬Āin┬Āthe┬ĀGulf┬Āstates┬Āat┬Āaround┬Ā$27┬Āper┬Ābarrel.┬ĀUS┬Āshale┬Āoil┬Ādoesn't start┬Āto┬Āpay┬Āback┬Āuntil┬Āit┬Āachieves┬Āa┬Āprice┬Āof┬Āat┬Āleast┬Ā$50┬Āper┬Ā barrel.┬ĀCurrent┬Āproduction┬Ācosts┬Āvary┬Ābetween┬Āthat┬Ābreakeven┬Āpoint┬Āand┬Āa┬Āprice┬Āof┬Ā$80┬Āper┬Ābarrel.┬Ā Long┬ĀTerm┬ĀEffects The┬Ādepletion┬Ārate┬Āof┬Āfracked┬Āwells┬Āis┬Āhigh.┬ĀBakken┬Āproduction┬Āfor┬Āany┬Āgiven┬Āfracked┬Āwell┬Ādeclines┬Ā45┬Āper┬Ācent┬Āper┬Āyear,┬Āvs.┬Ā5┬Āper┬Ācent┬Āper┬Āyear┬Āfor┬Āconventional┬Āwells. So after┬Āone┬Āyear┬Āthe┬Ā same┬Āwell┬Āproduces┬Ā55%┬Āof┬Āits┬Āinitial┬Āoutput,┬Āafter┬Ātwo┬Āyears┬Āthat┬Āreduces┬Āto┬Ā30%,┬Āand┬Āonly┬Ā17%┬Āafter┬Ā3┬Āyears.┬ĀProducers┬Āneed to keep┬Ādrilling┬Āin┬Āorder┬Āto┬Āstay┬Āin┬Āproduction┬Āwith┬Āa┬Āsteady┬Āflow┬Ā of┬Āoil.┬ĀThis┬Āseries┬Āof┬Āwells┬Āat┬Ādifferent┬Ālevels┬Āof┬Ādepletion┬Āin┬Āproduction┬Āby┬Āthe┬Āsame┬Ācompany┬Āis┬Ātermed┬Āthe┬Ā"drilling┬Ātreadmill."┬Ā Although┬Āin┬Āestablished┬Āfracking┬Āstates,┬Āsuch┬Āas┬ĀTexas,┬Āit┬Ātakes┬Āonly┬Āseven┬Ādays┬Āto┬Āget┬Āpermits┬Āto┬Āstart┬Āextraction,┬Āproduction┬Āin┬Āother┬Āregions,┬Āless┬Āused┬Āto┬Āthe┬Āprocess┬Ācan┬Āentail┬Āmonths┬Āof┬Ā delays┬Āfrom┬Ālegislators┬Āand┬Āpressure┬Āgroups.┬ĀEnvironmental┬Ārestrictions┬Āplaced┬Āon┬Āpotential┬Āsites┬Ācan┬Āpile┬Āon┬Ācosts┬Āand┬Āmake┬Āthe benefits┬Āof┬Āextending┬Āthe┬Āmethod┬Āinto┬Ānew┬Ālocales┬Āa┬Āpricey┬Ā prospect.┬ĀUnfortunately┬Āfracking┬Ācompanies┬Āhave┬Āalready┬Āexploited┬Āthe┬Āeasier,┬Ālarger┬Āreserves.┬ĀSince┬Āon┬Āaverage┬Āeach┬Ānew┬Āwell has┬Āa┬Āfixed┬Āstart┬Āup┬Ācost┬Āof┬Āaround┬Ā$9┬Āmillion,┬Āregardless┬Āof┬Āhow┬Ā much┬Āoil┬Āit┬Āwill┬Āproduce,┬Āfurther┬Āexpansion┬Āof┬Āshale┬Āoil┬Āproduction┬Āwill┬Āonly┬Ābreak┬Āeven┬Ānorth┬Āof┬Āthe┬Ācurrent┬Ā$76ŌĆÉ$77┬Ālevel.┬Ā When┬Āoil┬Āsold┬Āfor┬Ā$100┬Āper┬Ābarrel┬Āproducers┬Āgained┬Āa┬Āmargin┬Āof┬Ā$23┬Āper┬Ābarrel┬Āafter┬Āa┬Ācost┬Āof┬Ā$77┬Āper┬Ābarrel┬Āfor┬Ādrilling┬Āthe existing┬Āwells┬Āand┬Āoperating┬Āthem.┬ĀThat┬Āmargin┬Āprovided┬Āfunding┬Āfor┬Ā the┬Ā"drilling┬Ātreadmill"┬Āto┬Ācreate┬Āmore┬Āwells.┬ĀTherefore,┬Āalthough┬Āa┬Āfalling┬Āprice┬Āmay┬Ānot┬Ācause┬Āan┬Āimmediate┬Āslow┬Ādown┬Āin┬Āproduction,┬Āthe┬Ādisincentive┬Āof┬Ālower┬Āreturns,┬Ālonger┬Ādelays┬Āand┬Ā uncertain┬Ārewards┬Ācould┬Ādiscourage┬Āfuture┬Ādevelopment.┬ĀThe┬Āloss┬Āof┬Āa┬Āprofit┬Āon┬Āsales┬Āmeans┬Āfracking┬Ācompanies┬Āno┬Ālonger┬Āhave┬Āmoney┬Āto┬Ākeep┬Ādrilling┬Ānew┬Āwells.┬ĀThis┬Āwould┬Ācause┬Āa┬Āreduction┬Ā in┬ĀAmerica's┬Ācapacity┬Āto┬Āproduce┬Āoil┬Āin┬Āthe┬Ālong┬Āterm.┬Ā 8