More Related Content

What's hot (20)

Similar to Master budget (20)

Master budget

- 1. Introduction to Budgets and Preparing the Master Budget

- 2. Budgets A budget provides a comprehensive financial overview of planned company operations. Learning Objective 1 Goals and objectives

- 3. Provide an opportunity to reevaluate existing activities and evaluate new ones. Aid managers in communicating objectives and coordinating actions across the organization. Compel managers to think ahead

- 4. 1. Low levels of participation in the budget process and Lack of acceptance of responsibility for the final budget. 2. Incentives to lie and cheat in the budget process. 3. Difficulties in obtaining accurate sales forecasts. Learning Objective 2 Management should seek to create an environment where there is a true two-way flow of information.

- 5. Participative budgets are formulated with the active participation of all affected employees. Message conveyed by the budget system may be misaligned with incentives provided by the compensation system.

- 6. Dysfunctional incentives lead managers to make poor decisions. Lying can arise if the budget process creates incentives to bias the budget information. Budgetary Slack (budget padding) is the overstatement or understatement of budgeted revenue to create a goal that is easier to achieve. Learning Objective 3

- 7. A sales forecast is a prediction of sales under a given set of conditions. Sales forecasts are usually prepared under the direction of the top sales executive. Learning Objective 4 The sales budget is the result of decisions to create Conditions that will generate a desired level of sales.

- 8. Competitors’ actions Past patterns of sales Estimates made By sales force General economic conditions Changes in the firm’s prices Changes in product mix Market research studies Advertising and sales promotion plans

- 9. Strategic plan Long-range planning Capital budget Master budget Continuous budget Learning Objective 5

- 10. The most forward-looking budget is the strategic plan, which sets the overall goals and objectives of the organization. The strategic plan leads to long-range planning, which produces forecasted financial statements for five- to ten-year periods.

- 11. Long-range plans… are coordinated with capital budgets, which detail the planned expenditures for facilities, equipment, new products, and other long-term investments. Master budgets link to both long-range plans and short-term budgets.

- 12. The master budget is a detailed and comprehensive analysis of the first year of the long-range plan. It summarizes the planned activities of all subunits of an organization. Sales Production Distribution Finance

- 13. Rolling budgets... are a common form of master budgets that add a month in the future as the month just ended is dropped.

- 14. Operating budget (Profit plan). . . Financial budget. . . Focuses on the Income Statement and supporting schedules or budgeted expenses. Focuses on the effects that the operating budget and other plans will have on cash balances.

- 15. 1. Basic data Learning Objective 6 2. Operating budget 3. Financial budget

- 16. 1. Basic data a. Sales budget b. Cash collections from customers c. Purchases and cost-of-goods sold budget d. Cash disbursements for purchases e. Operating expense budget f. Cash disbursements for operating expenses The principal steps in preparing the master budget:

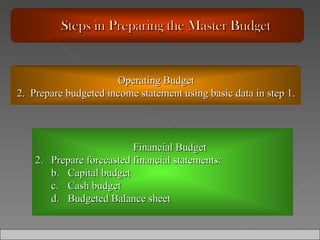

- 17. Financial Budget Prepare forecasted financial statements: b. Capital budget c. Cash budget d. Budgeted Balance sheet Operating Budget 2. Prepare budgeted income statement using basic data in step 1.

- 18. Sales budget Learning Objective 7 Cash collections from customers Disbursements for purchases Disbursements for operating expenses Purchases budget Operating expenses budget

- 19. It is easiest to prepare budgeted cash collections at the same time as the sales budget. Cash collections include the current month’s cash sales plus the previous month’s credit sales.

- 20. Budgeted purchases = Desired ending inventory + Cost of goods sold – Beginning inventory Disbursements could include 50% of the current month’s purchases and 50% of the Previous month’s purchases.

- 21. The budgeting of operating expenses depends on several factors. Month-to-month changes in sales volume and other cost-driver activities directly influence many operating expenses. Expenses driven by sales volume include sales commissions and many delivery expenses.

- 22. Other expenses are not influenced by sales or other cost-driver activity and are regarded as fixed, within appropriate relevant ranges. Rent Insurance Depreciation Salaries

- 23. Disbursements for operating expenses are based on the operating expense budget. Disbursements may include 50% of last month’s and this month’s wages and commissions plus miscellaneous and rent expenses. The total of these disbursements is then used in preparing the cash budget.

- 24. The income statement will be complete after addition of the interest expense, which is computed after the cash budget has been prepared. Budgeted income from operations is often a benchmark for judging management performance.

- 25. The Cash budget contains these major sections: available cash balance net cash receipts and disbursements financing Learning Objective 8 The cash budget is a statement of planned cash receipts and disbursements.

- 26. Available cash balance = Beginning cash balance – Minimum cash balance desired. Cash receipts depend on collections from customers’ accounts receivable, cash sales, and on other operating income sources.

- 27. Cash disbursements for purchases depend on the credit terms extended by suppliers and the bill-paying habits of the buyer. Payroll depends on wage, salary, and commission terms and on payroll dates.

- 28. Other disbursements include outlays for fixed assets, long-term investments, dividends, and the like. Disbursements for some costs and expenses depend on contractual terms for installment payments, mortgage payments, rents, leases, and miscellaneous items.

- 29. Management determines the minimum cash balance desired depending on the nature of the business and credit arrangements.

- 30. Financing requirements depend on how the total cash available compares with the total cash needed. Needs include the disbursements plus the desired ending cash balance.

- 31. Ending cash balance = Beginning cash balance + Receipts – Disbursements + Cash from financing The cash from financing can be either positive (borrowing) or negative (repayment).

- 32. The final step in preparing the master budget is to construct the budgeted balance sheet that projects each balance sheet item in accordance with the business plan. Management then considers all the major financial statements as a basis for changing the course of events.

- 33. An activity-based budgetary system emphasizes the planning and control purpose of cost management. Functional budgeting focuses on preparing budgets for various functions such as production, selling, and administrative support.

- 34. Financial models are only as good as the assumptions and the inputs used to build and manipulate them. Financial planning models are mathematical models that can incorporate the effects of alternative assumptions about sales, costs, or product mix.

- 35. Arithmetic errors are virtually nonexistent. Spreadsheet software for personal computers is a powerful and flexible tool for budgeting that can be used to prepare mathematical models. Financial planning models are mathematical models that can incorporate the effects of alternative assumptions about sales, costs, or product mix. Learning Objective 9

- 36. Ěý