Net payment method accounts

Download as pptx, pdf1 like4,678 views

Under the net payment method, consideration is calculated by adding the cash paid, agreed value of assets given, and agreed value of securities allotted by the transferee company to the transferor company. The document provides an example, where P Ltd takes over S Ltd and agrees to give 10 preference shares worth Rs. 10 each for every preference share in S Ltd, and Rs. 1 in cash plus 1 equity share worth Rs. 15 for every equity share in S Ltd. The total consideration is calculated as Rs. 20 lakh for preference shares, Rs. 1.2 crore for equity shares allotted, and Rs. 0.8 lakh for cash, amounting to Rs. 1.48 crore.

1 of 3

Download to read offline

Ad

Recommended

Certificate of deposit (cd)

Certificate of deposit (cd)Pankaj Mishra

╠²

Certificates of deposit (CDs) are short-term deposit instruments issued by banks and financial institutions to raise large amounts of money. CDs can be issued with maturities ranging from 7 days to 12 months by banks and 1 to 3 years by financial institutions. They must be purchased in amounts of at least Rs. 1 lakh. Banks and corporations use CDs to mobilize funds when needed, such as providing loans. CDs provide liquidity to banks while offering depositors higher returns than regular fixed deposits. However, the CD market in India has yet to be fully developed due to the lack of a secondary market and low usage despite being available for some time.Life insurance corporation ppt(1)

Life insurance corporation ppt(1)Himani Desai

╠²

This document provides an overview of Life Insurance Corporation (LIC) of India. It discusses that LIC was established in 1956 by the Parliament of India by consolidating over 245 private life insurance companies. LIC is wholly owned by the Government of India and is the largest life insurance company in India. The document outlines LIC's history, functions, benefits of life insurance, plans offered, rights of policyholders, subsidiaries and interesting facts such as LIC being the largest insurer in the world with over 29 crore policyholders.Vouching of cash transactions

Vouching of cash transactionsMahithaKatragadda

╠²

This document provides information on the process of vouching in accounting. It defines vouching as comparing accounting entries to supporting documents like receipts. It then discusses vouching for different types of cash transactions recorded in the cash book, including opening balances, cash sales, payments to creditors, and payments for expenses. For each transaction type, it lists the supporting documents that should be examined to verify the entry, such as cash memos, invoices, pay stubs, and receipts. The document provides guidance on steps an auditor should take to properly voucher transactions during an audit.Absorption of Company.pptx

Absorption of Company.pptxSnehal Pandey

╠²

The document discusses absorption of companies, which is when an existing company purchases another company doing similar business. After the purchase, the vendor company ceases to exist. It provides examples and discusses the objectives, methods, accounts, and journal entries involved in an absorption. It also compares absorption to amalgamation and provides a conclusion on absorption being a way for a company to take over another entity and use the acquired company's reputation and strengths.Appointment of Auditor

Appointment of AuditorAnkit Agarwal

╠²

The document summarizes the key provisions around appointment and qualifications of auditors under the Companies Act. It discusses who can be appointed as an auditor, circumstances for disqualification, appointment of first, subsequent and casual vacancy auditors, appointment through special/ordinary resolution, remuneration of auditors, ceiling on number of audits, and provisions for special, cost and branch audits.Non Performing Assets (NPA)

Non Performing Assets (NPA)Sanchit

╠²

The document discusses non-performing assets (NPAs) in the Indian banking system. It defines NPAs and outlines the different categories of assets based on their performance - standard, sub-standard, doubtful, and loss assets. Gross and net NPAs are also defined. The rise of NPAs can be attributed to both internal and external factors. Banks employ both preventive and curative strategies to manage their NPAs, such as restructuring loans, pursuing debt recovery, and using asset reconstruction companies. Tables show trends in NPAs for public sector banks, private banks, and all scheduled commercial banks from 2006-2007 to 2010-2011.Bills discounting

Bills discountingKalpana Udhaya

╠²

Bills discounting allows sellers to deposit genuine commercial bills with banks or financial institutions in exchange for immediate financial accommodation. Key features include a discount charge, fixed maturity date, ready access to finance, and the bank either discounting or purchasing the bill. For a bill to be eligible, it must be a usance bill with at least two good signatures, typically drawn between reputable companies. The discount period starts when the bank discounts the bill and ends at the bill's maturity. Bills discounting provides advantages like easy access to funds, safety of funds until maturity, certainty of payment, profitability, liquidity, an ideal investment, and relatively stable prices.Challenges for banking in current scenario

Challenges for banking in current scenarioHumsi Singh

╠²

The document outlines various challenges facing modern banking, including losses in rural branches, corruption, political pressures, and competition from non-banking financial institutions. It highlights issues such as high overdue loans, non-performing assets, and the bureaucratic nature of nationalized banks, which hinder efficiency and decision-making. The conclusion emphasizes the need for improvement in operational efficiency while maintaining a focus on customer service and profitability.fundamental analysis

fundamental analysisNoorulhadi Qureshi

╠²

The document discusses fundamental analysis, a method used to evaluate the past and expected performance of companies, industries, and economies for investment decisions. It covers various aspects of economic analysis, including how factors like economic cycles, inflation, interest rates, government finances, exchange rates, infrastructure, and seasonal impacts influence company performance. Ultimately, the document emphasizes the importance of a systematic approach to estimating future financial outcomes based on historical data.Collecting banker

Collecting banker ramandeepjrf

╠²

The document outlines the duties and protections of a collecting banker, who acts as an agent for customers by handling cheque collections while maintaining due care and diligence. It details the statutory protections under the Negotiable Instruments Act, conditions for becoming a holder or holder in due course, and defines the concept of negligence, including types and duties to avoid it. Key points include the requirements for cross cheques, payment considerations, and the implications of negligence in banking practices.Role of Banks in "ECONOMIC DEVELOPMENT OF INDIA"

Role of Banks in "ECONOMIC DEVELOPMENT OF INDIA"Shivaprasad Bhavikatti

╠²

Banks are financial institutions that accept deposits and lend money, playing a crucial role in economic development through various activities like capital formation, providing loans to agriculture and small industries, and linking organized and unorganized sectors. They act as catalysts for social change, aid in industrial development, and help regulate national savings while contributing to balance of trade and managing trade cycles. Overall, banks enhance savings, production, and employment in the economy.Company - Definition and explain the types of company as per income tax act 1...

Company - Definition and explain the types of company as per income tax act 1...Sundar B N

╠²

The document defines a company as an association of persons contributing to a common stock for specific purposes, subject to taxation under the Income Tax Act, 1961. It outlines various types of companies, including widely held, closely held, Indian, domestic, foreign, investment, and industrial companies based on their characteristics and tax liabilities. The conclusion emphasizes that while companies may offer similar benefits, the culture is shaped by employee treatment and levels of trust.Commercial paper

Commercial paperHimanshu Kumar

╠²

The document discusses commercial paper, which are short-term unsecured promissory notes issued by financially strong companies to raise funds for a period of up to one year. It explains what commercial paper is, who issues and invests in it, how it works, and provides an example of a company issuing commercial paper worth 50 crores. Commercial paper provides short-term funding to companies at lower interest rates than bank loans.Payment of cheques chapter 1

Payment of cheques chapter 1Nayan Vaghela

╠²

The document discusses the obligations and precautions of banks when honoring customer cheques under the Negotiable Instruments Act. It explains that banks must honor cheques drawn by customers if there are sufficient funds, and outlines various precautions banks must take regarding genuineness of cheques, customer accounts and balances, and legal restrictions. Precautions include verifying signatures, dates, amounts, endorsements, checking for stops on payments or legal orders, and only making payments that constitute "payment-in-due-course".Rights and duties of company auditor

Rights and duties of company auditorSundar B N

╠²

The document outlines the roles, rights, and duties of auditors under the Companies Act 2013, emphasizing their responsibility in examining financial transactions and ensuring accurate reporting. It details the auditor's rights to access company records, seek information, correct statements, and provide assistance in investigations. Additionally, it identifies the statutory duties imposed on auditors and the provisions regarding their appointment and removal.Debentures

DebenturesKarthik Bharadwaj

╠²

Debentures are instruments used by companies to raise long-term debt capital. A debenture acknowledges that a company has borrowed money from debenture holders that it promises to repay in the future. Debentures can be classified based on security, redemption terms, records, or convertibility. They provide advantages like no dilution of ownership and tax deductible interest payments. However, companies must make mandatory interest payments and repay the principal, or risk bankruptcy, so debentures also carry repayment risks.Gst

GstChaudhary Charan Singh Haryana Agricultural University

╠²

The Goods and Services Tax (GST) was implemented in India on July 8, 2017, to unify multiple indirect taxes and improve the overall tax system, impacting pricing and reducing economic distortions. It is a comprehensive tax applied at national levels on the sale, manufacturing, and consumption of goods and services and aims to enhance revenue and economic growth. The tax framework involves different types, such as Central GST, State GST, and Integrated GST, and abolishes many previous taxes to streamline the process.Extraordinary general meeting

Extraordinary general meetingDevesh Dhruw

╠²

An extraordinary general meeting (EGM) is a meeting other than the annual general meeting that is usually called to deal with urgent matters. An EGM can be convened by the board of directors, directors on requisition by shareholders holding at least 10% of shares, the requisitionists themselves if the board fails to call a meeting within 45 days, or the tribunal if deemed impracticable to hold a meeting otherwise. The board must give at least 21 days notice for an EGM unless 95% of shareholders consent to shorter notice. If requisitioned, the board must call an EGM within 45 days and it must be held within 3 months.Factoring services

Factoring servicesVikram Sankhala IIT, IIM, Ex IRS, FRM, Fin.Engr

╠²

Factoring is a financial transaction where a business sells its accounts receivable to a third party called a factor in exchange for immediate cash. This differs from a bank loan in that factoring emphasizes the receivable's value rather than the firm's creditworthiness, it is a purchase of assets rather than a loan, and involves three parties rather than two. The three parties are the seller of the receivable, the debtor, and the factor. Factoring transfers ownership of the receivables to the factor, giving them the right to collect payment from debtors and bear the risk of nonpayment.Central bank and credit control

Central bank and credit controlNayan Vaghela

╠²

This document discusses central bank credit control and its objectives and methods. It outlines several quantitative and qualitative methods used by central banks to regulate money supply and credit in the economy. The quantitative methods discussed are bank rate policy, open market operations, and variations in reserve ratios. The qualitative or selective methods discussed are fixation of margin requirements, consumer credit regulation, issuing directives, and rationing of credit. The objectives of credit control are to maintain price stability, economic growth, and meet financial needs during normal and emergency times.Income from business or profession

Income from business or professionParminder Kaur

╠²

The document discusses key aspects of income from business and profession under the Income Tax Act of 1961 in India. It defines business and profession, outlines the basis of charge for income from business/profession, and describes various deductions that are allowed under sections 30-37 of the Act such as rent, repairs, insurance, depreciation, bad debts, and more. It provides explanations and conditions for claiming many of these deductions.Commercial papers

Commercial papersTata Mutual Fund

╠²

Commercial paper (CP) is an unsecured, short-term debt instrument issued by corporations to meet short-term liabilities. CP was introduced in India in 1990 to provide highly rated corporations an alternative to bank borrowing. Only reputable corporations with good credit ratings can issue CPs to borrow at lower interest rates than banks and save on financing costs. CPs can be issued for periods between 15 days to one year, making them suitable for meeting working capital or current asset needs.Indian depository receipt(IDR)

Indian depository receipt(IDR) Rohit Kumar

╠²

Indian Depository Receipts (IDRs) allow foreign companies to raise capital from Indian investors in their home market. IDRs are issued by a domestic depository and represent underlying shares of the foreign company held in custody by an overseas custodian. Key features include being listed and traded on Indian stock exchanges, providing exposure to foreign stocks for Indian investors within the Indian regulatory framework, and allowing investors rights equivalent to shareholders such as voting and dividends. However, currency risk and lack of attendance at shareholder meetings are limitations of IDRs. Strict eligibility criteria, approvals, and disclosure guidelines regulate the issuance of IDRs in India.E-Banking Services and Challenges in India

E-Banking Services and Challenges in IndiaDheeraj Kumar Tiwari

╠²

The document discusses the evolution and significance of e-banking services in India, highlighting its growing popularity, convenience, and the challenges posed by cybercrime. It provides an overview of various e-banking services such as ATMs, debit and credit cards, and mobile banking, alongside significant government initiatives aimed at promoting financial inclusion. Additionally, it emphasizes the need for enhanced cybersecurity measures to protect customers and the banking system from fraudulent activities in an increasingly digital landscape.Sarfaesi act

Sarfaesi actjagannath ojha

╠²

The document discusses the Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act of 2002 in India. It provides a history of debt recovery laws in India prior to SARFAESI. SARFAESI allows banks and financial institutions to auction residential or commercial properties to recover loans in case of default. It enables banks to reduce non-performing assets by taking possession of secured assets without court intervention. The act established asset reconstruction companies and empowers banks to seize assets and sell them off in order to strengthen banks' ability to recover non-performing assets faster.Classification of Companies

Classification of CompaniesJayasankarJayasoman2

╠²

The document provides a comprehensive overview of the classification of companies in the Indian economy, highlighting various categories based on factors such as incorporation, liability, number of members, domicile, and other miscellaneous factors. It discusses types of companies like royal charter, statutory, registered, limited by shares, private, public, foreign, and government companies, among others. The conclusion emphasizes that these classifications help in understanding the distinct characteristics and legal identities of various companies.Leasing

LeasingMaksudul Huq Chowdhury

╠²

This document discusses leasing, which allows one party to use an asset owned by another party. There are two main types of leases: operating/service leases and financial/net leases. Operating leases provide maintenance services while financial leases do not. Leasing offers advantages over ownership like facilitating asset acquisition and improving financial position, but parties must consider tax and ownership implications.Sarfaesi act ppt

Sarfaesi act pptAkshayChaudhary82

╠²

The document outlines the history, mechanisms, and implications of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI Act) in India, highlighting its role in addressing the rising issue of non-performing assets (NPAs) in the banking sector. It discusses the act's provisions, enforcement mechanisms, and the challenges faced by borrowers and banks alike, emphasizing the need for a balance between effective debt recovery and borrower protection. Additionally, the document presents criticisms of the act's implementation and suggests the necessity for proper adherence to guidelines and resolution of grievances.Packing and Packaging of Cookies

Packing and Packaging of Cookiesbreakfreez

╠²

Packing involves preparing products for basic protection from damage and loss during transport using materials like butter paper and string. Packaging may also involve using handmade paper and cylindrical boxes to handle and transport cookies. Labels provide important product details like best before dates, manufacturing information, and price to ensure quality and compliance.Portafolio diagnosticoliz Juarez

╠²

El documento presenta el portafolio de diagn├│stico de Lizet Juarez J. En ├®l, se describen las actividades y conocimientos previos de la autora, los recursos did├Īcticos utilizados como presentaciones en PowerPoint, y ├Īreas de oportunidad como el espacio limitado del aula y el desconocimiento de programas inform├Īticos y plataformas. El objetivo futuro es implementar estrategias mediante recursos educativos abiertos para socializar el conocimiento y explorar m├Īs las nuevas tecnolog├Łas.More Related Content

What's hot (20)

fundamental analysis

fundamental analysisNoorulhadi Qureshi

╠²

The document discusses fundamental analysis, a method used to evaluate the past and expected performance of companies, industries, and economies for investment decisions. It covers various aspects of economic analysis, including how factors like economic cycles, inflation, interest rates, government finances, exchange rates, infrastructure, and seasonal impacts influence company performance. Ultimately, the document emphasizes the importance of a systematic approach to estimating future financial outcomes based on historical data.Collecting banker

Collecting banker ramandeepjrf

╠²

The document outlines the duties and protections of a collecting banker, who acts as an agent for customers by handling cheque collections while maintaining due care and diligence. It details the statutory protections under the Negotiable Instruments Act, conditions for becoming a holder or holder in due course, and defines the concept of negligence, including types and duties to avoid it. Key points include the requirements for cross cheques, payment considerations, and the implications of negligence in banking practices.Role of Banks in "ECONOMIC DEVELOPMENT OF INDIA"

Role of Banks in "ECONOMIC DEVELOPMENT OF INDIA"Shivaprasad Bhavikatti

╠²

Banks are financial institutions that accept deposits and lend money, playing a crucial role in economic development through various activities like capital formation, providing loans to agriculture and small industries, and linking organized and unorganized sectors. They act as catalysts for social change, aid in industrial development, and help regulate national savings while contributing to balance of trade and managing trade cycles. Overall, banks enhance savings, production, and employment in the economy.Company - Definition and explain the types of company as per income tax act 1...

Company - Definition and explain the types of company as per income tax act 1...Sundar B N

╠²

The document defines a company as an association of persons contributing to a common stock for specific purposes, subject to taxation under the Income Tax Act, 1961. It outlines various types of companies, including widely held, closely held, Indian, domestic, foreign, investment, and industrial companies based on their characteristics and tax liabilities. The conclusion emphasizes that while companies may offer similar benefits, the culture is shaped by employee treatment and levels of trust.Commercial paper

Commercial paperHimanshu Kumar

╠²

The document discusses commercial paper, which are short-term unsecured promissory notes issued by financially strong companies to raise funds for a period of up to one year. It explains what commercial paper is, who issues and invests in it, how it works, and provides an example of a company issuing commercial paper worth 50 crores. Commercial paper provides short-term funding to companies at lower interest rates than bank loans.Payment of cheques chapter 1

Payment of cheques chapter 1Nayan Vaghela

╠²

The document discusses the obligations and precautions of banks when honoring customer cheques under the Negotiable Instruments Act. It explains that banks must honor cheques drawn by customers if there are sufficient funds, and outlines various precautions banks must take regarding genuineness of cheques, customer accounts and balances, and legal restrictions. Precautions include verifying signatures, dates, amounts, endorsements, checking for stops on payments or legal orders, and only making payments that constitute "payment-in-due-course".Rights and duties of company auditor

Rights and duties of company auditorSundar B N

╠²

The document outlines the roles, rights, and duties of auditors under the Companies Act 2013, emphasizing their responsibility in examining financial transactions and ensuring accurate reporting. It details the auditor's rights to access company records, seek information, correct statements, and provide assistance in investigations. Additionally, it identifies the statutory duties imposed on auditors and the provisions regarding their appointment and removal.Debentures

DebenturesKarthik Bharadwaj

╠²

Debentures are instruments used by companies to raise long-term debt capital. A debenture acknowledges that a company has borrowed money from debenture holders that it promises to repay in the future. Debentures can be classified based on security, redemption terms, records, or convertibility. They provide advantages like no dilution of ownership and tax deductible interest payments. However, companies must make mandatory interest payments and repay the principal, or risk bankruptcy, so debentures also carry repayment risks.Gst

GstChaudhary Charan Singh Haryana Agricultural University

╠²

The Goods and Services Tax (GST) was implemented in India on July 8, 2017, to unify multiple indirect taxes and improve the overall tax system, impacting pricing and reducing economic distortions. It is a comprehensive tax applied at national levels on the sale, manufacturing, and consumption of goods and services and aims to enhance revenue and economic growth. The tax framework involves different types, such as Central GST, State GST, and Integrated GST, and abolishes many previous taxes to streamline the process.Extraordinary general meeting

Extraordinary general meetingDevesh Dhruw

╠²

An extraordinary general meeting (EGM) is a meeting other than the annual general meeting that is usually called to deal with urgent matters. An EGM can be convened by the board of directors, directors on requisition by shareholders holding at least 10% of shares, the requisitionists themselves if the board fails to call a meeting within 45 days, or the tribunal if deemed impracticable to hold a meeting otherwise. The board must give at least 21 days notice for an EGM unless 95% of shareholders consent to shorter notice. If requisitioned, the board must call an EGM within 45 days and it must be held within 3 months.Factoring services

Factoring servicesVikram Sankhala IIT, IIM, Ex IRS, FRM, Fin.Engr

╠²

Factoring is a financial transaction where a business sells its accounts receivable to a third party called a factor in exchange for immediate cash. This differs from a bank loan in that factoring emphasizes the receivable's value rather than the firm's creditworthiness, it is a purchase of assets rather than a loan, and involves three parties rather than two. The three parties are the seller of the receivable, the debtor, and the factor. Factoring transfers ownership of the receivables to the factor, giving them the right to collect payment from debtors and bear the risk of nonpayment.Central bank and credit control

Central bank and credit controlNayan Vaghela

╠²

This document discusses central bank credit control and its objectives and methods. It outlines several quantitative and qualitative methods used by central banks to regulate money supply and credit in the economy. The quantitative methods discussed are bank rate policy, open market operations, and variations in reserve ratios. The qualitative or selective methods discussed are fixation of margin requirements, consumer credit regulation, issuing directives, and rationing of credit. The objectives of credit control are to maintain price stability, economic growth, and meet financial needs during normal and emergency times.Income from business or profession

Income from business or professionParminder Kaur

╠²

The document discusses key aspects of income from business and profession under the Income Tax Act of 1961 in India. It defines business and profession, outlines the basis of charge for income from business/profession, and describes various deductions that are allowed under sections 30-37 of the Act such as rent, repairs, insurance, depreciation, bad debts, and more. It provides explanations and conditions for claiming many of these deductions.Commercial papers

Commercial papersTata Mutual Fund

╠²

Commercial paper (CP) is an unsecured, short-term debt instrument issued by corporations to meet short-term liabilities. CP was introduced in India in 1990 to provide highly rated corporations an alternative to bank borrowing. Only reputable corporations with good credit ratings can issue CPs to borrow at lower interest rates than banks and save on financing costs. CPs can be issued for periods between 15 days to one year, making them suitable for meeting working capital or current asset needs.Indian depository receipt(IDR)

Indian depository receipt(IDR) Rohit Kumar

╠²

Indian Depository Receipts (IDRs) allow foreign companies to raise capital from Indian investors in their home market. IDRs are issued by a domestic depository and represent underlying shares of the foreign company held in custody by an overseas custodian. Key features include being listed and traded on Indian stock exchanges, providing exposure to foreign stocks for Indian investors within the Indian regulatory framework, and allowing investors rights equivalent to shareholders such as voting and dividends. However, currency risk and lack of attendance at shareholder meetings are limitations of IDRs. Strict eligibility criteria, approvals, and disclosure guidelines regulate the issuance of IDRs in India.E-Banking Services and Challenges in India

E-Banking Services and Challenges in IndiaDheeraj Kumar Tiwari

╠²

The document discusses the evolution and significance of e-banking services in India, highlighting its growing popularity, convenience, and the challenges posed by cybercrime. It provides an overview of various e-banking services such as ATMs, debit and credit cards, and mobile banking, alongside significant government initiatives aimed at promoting financial inclusion. Additionally, it emphasizes the need for enhanced cybersecurity measures to protect customers and the banking system from fraudulent activities in an increasingly digital landscape.Sarfaesi act

Sarfaesi actjagannath ojha

╠²

The document discusses the Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act of 2002 in India. It provides a history of debt recovery laws in India prior to SARFAESI. SARFAESI allows banks and financial institutions to auction residential or commercial properties to recover loans in case of default. It enables banks to reduce non-performing assets by taking possession of secured assets without court intervention. The act established asset reconstruction companies and empowers banks to seize assets and sell them off in order to strengthen banks' ability to recover non-performing assets faster.Classification of Companies

Classification of CompaniesJayasankarJayasoman2

╠²

The document provides a comprehensive overview of the classification of companies in the Indian economy, highlighting various categories based on factors such as incorporation, liability, number of members, domicile, and other miscellaneous factors. It discusses types of companies like royal charter, statutory, registered, limited by shares, private, public, foreign, and government companies, among others. The conclusion emphasizes that these classifications help in understanding the distinct characteristics and legal identities of various companies.Leasing

LeasingMaksudul Huq Chowdhury

╠²

This document discusses leasing, which allows one party to use an asset owned by another party. There are two main types of leases: operating/service leases and financial/net leases. Operating leases provide maintenance services while financial leases do not. Leasing offers advantages over ownership like facilitating asset acquisition and improving financial position, but parties must consider tax and ownership implications.Sarfaesi act ppt

Sarfaesi act pptAkshayChaudhary82

╠²

The document outlines the history, mechanisms, and implications of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI Act) in India, highlighting its role in addressing the rising issue of non-performing assets (NPAs) in the banking sector. It discusses the act's provisions, enforcement mechanisms, and the challenges faced by borrowers and banks alike, emphasizing the need for a balance between effective debt recovery and borrower protection. Additionally, the document presents criticisms of the act's implementation and suggests the necessity for proper adherence to guidelines and resolution of grievances.Viewers also liked (9)

Packing and Packaging of Cookies

Packing and Packaging of Cookiesbreakfreez

╠²

Packing involves preparing products for basic protection from damage and loss during transport using materials like butter paper and string. Packaging may also involve using handmade paper and cylindrical boxes to handle and transport cookies. Labels provide important product details like best before dates, manufacturing information, and price to ensure quality and compliance.Portafolio diagnosticoliz Juarez

╠²

El documento presenta el portafolio de diagn├│stico de Lizet Juarez J. En ├®l, se describen las actividades y conocimientos previos de la autora, los recursos did├Īcticos utilizados como presentaciones en PowerPoint, y ├Īreas de oportunidad como el espacio limitado del aula y el desconocimiento de programas inform├Īticos y plataformas. El objetivo futuro es implementar estrategias mediante recursos educativos abiertos para socializar el conocimiento y explorar m├Īs las nuevas tecnolog├Łas.Portafolio de trabajoliz Juarez

╠²

El documento describe los objetivos de Lizet Ju├Īrez de identificar recursos educativos abiertos en l├Łnea para difundir informaci├│n sobre el desarrollo infantil. Se├▒ala que las bibliotecas digitales de universidades prestigiosas como la UNAM, el ITESM y la UCM son buenas fuentes de informaci├│n, ya que cuentan con centros de investigaci├│n, actualizan regularmente sus bases de datos y el contenido es de acceso p├║blico. Tambi├®n enfatiza la importancia de citar correctamente las fuentes de informaci├│n siguiendo el formato APA 2014.Dß╗ŗch vß╗ź quß║Żng c├Īo facebook

Dß╗ŗch vß╗ź quß║Żng c├Īo facebook LongKingAds001

╠²

Phß║Īm Anh Long

─ÉT: 016.3388.5294

Email: anhlong@kingads.net

Website: kingads.net

(quß║Żng c├Īo facebook, t─āng like facebook, quß║Żn trß╗ŗ fanpage)Wildlifeconservationsuryanshsinghppt 140714000450-phpapp02

Wildlifeconservationsuryanshsinghppt 140714000450-phpapp02Prateek Gupta

╠²

This presentation discusses wildlife conservation in India. It covers the key laws and organizations related to wildlife protection, including the Wildlife Protection Act of 1972, the Forest Conservation Act of 1980, and the International Union for Conservation of Nature. The document outlines the main threats to wildlife such as habitat loss and pollution, and emphasizes the importance of conservation efforts like protected areas and breeding programs.Excel dwellings

Excel dwellingsExcel Dwellings

╠²

Founded in 2013, Excel is the brainchild of four real estate professionals with more than 40yrs experience altogether in the fields of real estate, finance and marketing. A process-driven and product oriented enterprise, its services are focused on meeting quality standards and being tailored to suitevery customers needs. Backed by private equity and other financial institutions, Excel has sufficient funds to complete its ongoing projects on time, without compromising on quality. With products that encompass all the quality parameters, the company envisions a larger goal of being an incomparable developer, not just in the region, but nationally, legal, finance, engineering and architecture teams, along with second-line management ar in place in the company

Being tied up with international architects and other overseas institutions, Excel guarantees transperency at all levels and ensures minimum mistakes while executing the projects. The company performs intensive financial analysis, taking into account all the future market scenarios. This leads to the belief in joy of growth by giving back to community and by constantly striving to enhance the growth of all stakeholders .Store Promotion

Store Promotionbreakfreez

╠²

Store promotion is an increasingly popular method where a country's merchandise is promoted by a chain or department store. A private, family-run retail group with over 1230 years of history aims to make good and beautiful products accessible to all. The group has stores in locations like Boulevard Haussmann in Paris and one designed by Jean Nouvel in Berlin.Role of ngo

Role of ngoPrateek Gupta

╠²

This document discusses the roles of non-governmental organizations (NGOs) and voluntary agencies in preserving the environment. It provides examples of several major international NGOs working on environmental issues, such as the International Union for Conservation of Nature, The Nature Conservancy, World Wide Fund for Nature, Environmental Defense Fund, Greenpeace, Earthwatch Institute, Fauna and Flora International, World Resources Institute, and Forest Stewardship Council. These organizations work to protect biodiversity, combat climate change, promote sustainable practices, advocate for environmental policies, and educate the public on environmental issues through research, conservation projects, advocacy, and partnerships with other groups.Ad

Recently uploaded (20)

2025 June Year 9 Presentation: Subject selection.pptx

2025 June Year 9 Presentation: Subject selection.pptxmansk2

╠²

2025 June Year 9 Presentation: Subject selectionROLE PLAY: FIRST AID -CPR & RECOVERY POSITION.pptx

ROLE PLAY: FIRST AID -CPR & RECOVERY POSITION.pptxBelicia R.S

╠²

Role play : First Aid- CPR, Recovery position and Hand hygiene.

Scene 1: Three friends are shopping in a mall

Scene 2: One of the friend becomes victim to electric shock.

Scene 3: Arrival of a first aider

Steps:

Safety First

Evaluate the victimŌĆśs condition

Call for help

Perform CPR- Secure an open airway, Chest compression, Recuse breaths.

Put the victim in Recovery position if unconscious and breathing normally.

THE PSYCHOANALYTIC OF THE BLACK CAT BY EDGAR ALLAN POE (1).pdf

THE PSYCHOANALYTIC OF THE BLACK CAT BY EDGAR ALLAN POE (1).pdfnabilahk908

╠²

Psychoanalytic Analysis of The Black Cat by Edgar Allan Poe explores the deep psychological dimensions of the narratorŌĆÖs disturbed mind through the lens of Sigmund FreudŌĆÖs psychoanalytic theory. According to Freud (1923), the human psyche is structured into three components: the Id, which contains primitive and unconscious desires; the Ego, which operates on the reality principle and mediates between the Id and the external world; and the Superego, which reflects internalized moral standards.

In this story, Poe presents a narrator who experiences a psychological breakdown triggered by repressed guilt, aggression, and internal conflict. This analysis focuses not only on the gothic horror elements of the narrative but also on the narratorŌĆÖs mental instability and emotional repression, demonstrating how the imbalance of these three psychic forces contributes to his downfall.Introduction to Generative AI and Copilot.pdf

Introduction to Generative AI and Copilot.pdfTechSoup

╠²

In this engaging and insightful two-part webinar series, where we will dive into the essentials of generative AI, address key AI concerns, and demonstrate how nonprofits can benefit from using MicrosoftŌĆÖs AI assistant, Copilot, to achieve their goals.

This event series to help nonprofits obtain Copilot skills is made possible by generous support from Microsoft.PEST OF WHEAT SORGHUM BAJRA and MINOR MILLETS.pptx

PEST OF WHEAT SORGHUM BAJRA and MINOR MILLETS.pptxArshad Shaikh

╠²

Wheat, sorghum, and bajra (pearl millet) are susceptible to various pests that can significantly impact crop yields. Common pests include aphids, stem borers, shoot flies, and armyworms. Aphids feed on plant sap, weakening the plants, while stem borers and shoot flies damage the stems and shoots, leading to dead hearts and reduced growth. Armyworms, on the other hand, are voracious feeders that can cause extensive defoliation and grain damage. Effective management strategies, including resistant varieties, cultural practices, and targeted pesticide applications, are essential to mitigate pest damage and ensure healthy crop production.LAZY SUNDAY QUIZ "A GENERAL QUIZ" JUNE 2025 SMC QUIZ CLUB, SILCHAR MEDICAL CO...

LAZY SUNDAY QUIZ "A GENERAL QUIZ" JUNE 2025 SMC QUIZ CLUB, SILCHAR MEDICAL CO...Ultimatewinner0342

╠²

¤¦Ā Lazy Sunday Quiz | General Knowledge Trivia by SMC Quiz Club ŌĆō Silchar Medical College

Presenting the Lazy Sunday Quiz, a fun and thought-provoking general knowledge quiz created by the SMC Quiz Club of Silchar Medical College & Hospital (SMCH). This quiz is designed for casual learners, quiz enthusiasts, and competitive teams looking for a diverse, engaging set of questions with clean visuals and smart clues.

¤Ä» What is the Lazy Sunday Quiz?

The Lazy Sunday Quiz is a light-hearted yet intellectually rewarding quiz session held under the SMC Quiz Club banner. ItŌĆÖs a general quiz covering a mix of current affairs, pop culture, history, India, sports, medicine, science, and more.

Whether youŌĆÖre hosting a quiz event, preparing a session for students, or just looking for quality trivia to enjoy with friends, this PowerPoint deck is perfect for you.

¤ōŗ Quiz Format & Structure

Total Questions: ~50

Types: MCQs, one-liners, image-based, visual connects, lateral thinking

Rounds: Warm-up, Main Quiz, Visual Round, Connects (optional bonus)

Design: Simple, clear slides with answer explanations included

Tools Needed: Just a projector or screen ŌĆō ready to use!

¤¦Ā Who Is It For?

College quiz clubs

School or medical students

Teachers or faculty for classroom engagement

Event organizers needing quiz content

Quizzers preparing for competitions

Freelancers building quiz portfolios

¤ÆĪ Why Use This Quiz?

Ready-made, high-quality content

Curated with lateral thinking and storytelling in mind

Covers both academic and pop culture topics

Designed by a quizzer with real event experience

Usable in inter-college fests, informal quizzes, or Sunday brain workouts

¤ōÜ About the Creators

This quiz has been created by Rana Mayank Pratap, an MBBS student and quizmaster at SMC Quiz Club, Silchar Medical College. The club aims to promote a culture of curiosity and smart thinking through weekly and monthly quiz events.

¤öŹ SEO Tags:

quiz, general knowledge quiz, trivia quiz, ║▌║▌▀ŻShare quiz, college quiz, fun quiz, medical college quiz, India quiz, pop culture quiz, visual quiz, MCQ quiz, connect quiz, science quiz, current affairs quiz, SMC Quiz Club, Silchar Medical College

¤ōŻ Reuse & Credit

YouŌĆÖre free to use or adapt this quiz for your own events or sessions with credit to:

SMC Quiz Club ŌĆō Silchar Medical College & Hospital

Curated by: Rana Mayank PratapHow to Manage Inventory Movement in Odoo 18 POS

How to Manage Inventory Movement in Odoo 18 POSCeline George

╠²

Inventory management in the Odoo 18 Point of Sale system is tightly integrated with the inventory module, offering a solution to businesses to manage sales and stock in one united system.Q1_ENGLISH_PPT_WEEK 1 power point grade 3 Quarter 1 week 1

Q1_ENGLISH_PPT_WEEK 1 power point grade 3 Quarter 1 week 1jutaydeonne

╠²

Grade 3 Quarter 1 Week 1 English part 2Community Health Nursing Approaches, Concepts, Roles & Responsibilities ŌĆō Uni...

Community Health Nursing Approaches, Concepts, Roles & Responsibilities ŌĆō Uni...RAKESH SAJJAN

╠²

This PowerPoint presentation is based on Unit 6 ŌĆō Community Health Nursing Approaches, Concepts, Roles & Responsibilities of Community Health Nursing Personnel, designed for B.Sc Nursing 5th Semester students under the subject Community Health Nursing ŌĆō I, following the syllabus of the Indian Nursing Council (INC).

This unit focuses on the various approaches in community health, the organizational framework, and the responsibilities of different levels of nursing staff in the healthcare system. It emphasizes the real-world application of nursing principles to provide comprehensive and preventive care to the community.

¤ōś Key Areas Covered in this Presentation:

Introduction to the concept of community health nursing

Approaches to community health:

Nursing Process Approach

Epidemiological Approach

Evidence-Based Approach

Problem-Solving Approach

Nursing Theories in Community Health Practice

Explanation of teamwork and intersectoral coordination

Concept of primary health care and its application in community nursing

Levels of health care delivery ŌĆō primary, secondary, and tertiary care

Home visit process: principles, planning, implementation, and follow-up

Use of community bag and record maintenance

Roles and responsibilities of:

Auxiliary Nurse Midwives (ANMs)

Community Health Officers (CHOs)

Staff Nurses

ASHA workers

Public Health Nurses (PHNs)

Documentation and reporting in community settings

Promotion of health education, immunization, maternal and child health, and nutritional support

Role of nurse in disease surveillance, outbreak control, and health promotion

Ethical principles in community nursing

Coordination with health team members and village health committees

This presentation is useful for:

Nursing students preparing for university theory exams, class tests, or viva

Nursing educators conducting lectures or field discussions

Interns and trainees working in PHCs, sub-centers, or community settings

Community nurses and health educators involved in rural and urban outreach

The content is simplified, clear, and enhanced with point-wise explanations, flowcharts, and field-related examples for better retention and application.Health Care Planning and Organization of Health Care at Various Levels ŌĆō Unit...

Health Care Planning and Organization of Health Care at Various Levels ŌĆō Unit...RAKESH SAJJAN

╠²

This comprehensive PowerPoint presentation is prepared for B.Sc Nursing 5th Semester students and covers Unit 2 of Community Health Nursing ŌĆō I based on the Indian Nursing Council (INC) syllabus. The unit focuses on the planning, structure, and functioning of health care services at various levels in India. It is especially useful for nursing educators and students preparing for university exams, internal assessments, or professional teaching assignments.

The content of this presentation includes:

Historical development of health planning in India

Detailed study of various health committees: Bhore, Mudaliar, Kartar Singh, Shrivastava Committee, etc.

Overview of major health commissions

In-depth understanding of Five-Year Plans and their impact on health care

Community participation and stakeholder involvement in health care planning

Structure of health care delivery system at central, state, district, and peripheral levels

Concepts and implementation of Primary Health Care (PHC) and Sustainable Development Goals (SDGs)

Introduction to Comprehensive Primary Health Care (CPHC) and Health and Wellness Centers (HWCs)

Expanded role of Mid-Level Health Providers (MLHPs) and Community Health Providers (CHPs)

Explanation of national health policies: NHP 1983, 2002, and 2017

Key national missions and schemes including:

National Health Mission (NHM)

National Rural Health Mission (NRHM)

National Urban Health Mission (NUHM)

Ayushman Bharat ŌĆō Pradhan Mantri Jan Arogya Yojana (PM-JAY)

Universal Health Coverage (UHC) and IndiaŌĆÖs commitment to equitable health care

This presentation is ideal for:

Nursing students (B.Sc, GNM, Post Basic)

Nursing tutors and faculty

Health educators

Competitive exam aspirants in nursing and public health

It is organized in a clear, point-wise format with relevant terminologies and a focus on applied knowledge. The slides can also be used for community health demonstrations, teaching sessions, and revision guides.ABCs of Bookkeeping for Nonprofits TechSoup.pdf

ABCs of Bookkeeping for Nonprofits TechSoup.pdfTechSoup

╠²

Accounting can be hard enough if you havenŌĆÖt studied it in school. Nonprofit accounting is actually very different and more challenging still.

Need help? Join Nonprofit CPA and QuickBooks expert Gregg Bossen in this first-time webinar and learn the ABCs of keeping books for a nonprofit organization.

Key takeaways

* What accounting is and how it works

* How to read a financial statement

* What financial statements should be given to the board each month

* What three things nonprofits are required to track

What features to use in QuickBooks to track programs and grantsSCHIZOPHRENIA OTHER PSYCHOTIC DISORDER LIKE Persistent delusion/Capgras syndr...

SCHIZOPHRENIA OTHER PSYCHOTIC DISORDER LIKE Persistent delusion/Capgras syndr...parmarjuli1412

╠²

SCHIZOPHRENIA INCLUDED TOPIC IS INTRODUCTION, DEFINITION OF GENERAL TERM IN PSYCHIATRIC, THEN DIFINITION OF SCHIZOPHRENIA, EPIDERMIOLOGY, ETIOLOGICAL FACTORS, CLINICAL FEATURE(SIGN AND SYMPTOMS OF SCHIZOPHRENIA), CLINICAL TYPES OF SCHIZOPHRENIA, DIAGNOSIS, INVESTIGATION, TREATMENT MODALITIES(PHARMACOLOGICAL MANAGEMENT, PSYCHOTHERAPY, ECT, PSYCHO-SOCIO-REHABILITATION), NURSING MANAGEMENT(ASSESSMENT,DIAGNOSIS,NURSING INTERVENTION,AND EVALUATION), OTHER PSYCHOTIC DISORDER LIKE Persistent delusion/Capgras syndrome(The Delusion of Doubles)/Acute and Transient Psychotic Disorders/Induced Delusional Disorders/Schizoaffective Disorder /CAPGRAS SYNDROME(DELUSION OF DOUBLE), GERIATRIC CONSIDERATION, FOLLOW UP, HOMECARE AND REHABILITATION OF THE PATIENT, Paper 108 | ThoreauŌĆÖs Influence on Gandhi: The Evolution of Civil Disobedience

Paper 108 | ThoreauŌĆÖs Influence on Gandhi: The Evolution of Civil DisobedienceRajdeep Bavaliya

╠²

Dive into the powerful journey from ThoreauŌĆÖs 19thŌĆæcentury essay to GandhiŌĆÖs mass movement, and discover how one manŌĆÖs moral stand became the backbone of nonviolent resistance worldwide. Learn how conscience met strategy to spark revolutions, and why their legacy still inspires todayŌĆÖs social justice warriors. Uncover the evolution of civil disobedience. DonŌĆÖt forget to like, share, and follow for more deep dives into the ideas that changed the world.

M.A. Sem - 2 | Presentation

Presentation Season - 2

Paper - 108: The American Literature

Submitted Date: April 2, 2025

Paper Name: The American Literature

Topic: ThoreauŌĆÖs Influence on Gandhi: The Evolution of Civil Disobedience

[Please copy the link and paste it into any web browser to access the content.]

Video Link: https://youtu.be/HXeq6utg7iQ

For a more in-depth discussion of this presentation, please visit the full blog post at the following link: https://rajdeepbavaliya2.blogspot.com/2025/04/thoreau-s-influence-on-gandhi-the-evolution-of-civil-disobedience.html

Please visit this blog to explore additional presentations from this season:

Hashtags:

#CivilDisobedience #ThoreauToGandhi #NonviolentResistance #Satyagraha #Transcendentalism #SocialJustice #HistoryUncovered #GandhiLegacy #ThoreauInfluence #PeacefulProtest

Keyword Tags:

civil disobedience, Thoreau, Gandhi, Satyagraha, nonviolent protest, transcendentalism, moral resistance, Gandhi Thoreau connection, social change, political philosophyLDM Recording Presents Yogi Goddess by LDMMIA

LDM Recording Presents Yogi Goddess by LDMMIALDM & Mia eStudios

╠²

A bonus dept update. Happy Summer 25 almost. Do Welcome or Welcome back. Our 10th Free workshop will be released the end of this week, June 20th Weekend. All Materials/updates/Workshops are timeless for future students.

6/17/25: ŌĆ£My now Grads, YouŌĆÖre doing well. I applaud your efforts to continue. We all are shifting to new paradigm realities. Its rough, thereŌĆÖs good and bad days/weeks. However, Reiki with Yoga assistance, does work.ŌĆØ

6/18/25: "For those planning the Training Program Do Welcome. Happy Summer 2k25. You are not ignored and much appreciated. Our updates are ongoing and weekly since Spring. I Hope you Enjoy the Practitioner Grad Level. There's more to come. We will also be wrapping up Level One. So I can work on Levels 2 topics. Please see documents for any news updates. Also visit our websites. Every decade I release a Campus eMap. I will work on that for summer 25. We have 2 old libraries online thats open. https://ldmchapels.weebly.com "

A Safe House,

sanctuary of virtual relaxation and rejuvenation.

By ┬®YogiGoddess of ┬®LDMMIA, ┬®LDMYoga.

ŌÖźTeacher Dept: (Rev Dr) Leslie Moore, ND Yoga (Aide/LPN Trained), Metaphysician,

Using Reiki Practitioner/Master Level Trained.

#yogigoddess @YogiGoddessVEVO

ŌÖźLDMMIA & Depts: are fusing the fan clubs so do welcome.

We are timeless and a safe haven / Cyber Space. ThatŌĆÖs the design of our Fan/Reader/Loyal Blog.ŌÖź

LDM HQ Est. in Ann Arbor, MI 2005.

- Moved to Detroit in 2006,

- Expanded online 2007-2024+

- Became a Beatz Studio in 2009 as Yogi Goddess. After our Apple Podcast

- Relocated to Mount Pleasant MI for College The Pandemic Ending.

- Endemic - Present; Moved back to assist Family in Metro Detroit.

Practitioner Student. Level/Session 2

* The Review & Topics:

* All virtual, adult, education students must be over 18 years to attend LDMMIA eClasses and vStudio Thx.

* Please refer to our Free Workshops anytime for review/notes.

*Tech: Products Sold Separately are for Uploading Size Reasons, THX.

MIA TECH: Videos under Copyright including our Music Video for Yogi Goddess, Can only be picked up vs shop downloaded. We are under vydia.com

Pickup will be our Youtube, for unlisted Playlist.

We do have another Vod for Session 2, Level 1.

After that we move on to Session 3.

Levels 1-3 should be done by August to Sept.

LDM Recording, Yogi Goddess Bio (ReverbNation)

Organization functions as a Studio 1st. We are a Media Co, Private Sector, and Global Listed.

Imagine we are 2 different studios. One for Yoga, the Other for Music Beatz. We are also Vevo TV for Smart TV and Youtube, 2 platforms. The audience differs.

Our Biz income are Media monetization within The Entertainment genre. This includes the category of Yoga, Reiki, ASMR, and Music Beatz. Any other tips, donations, B2C sales/Student Tuition are extra. The Biz gifts are appreciated. (We have been given a few $K for random emergencies.)

How to Implement Least Package Removal Strategy in Odoo 18 Inventory

How to Implement Least Package Removal Strategy in Odoo 18 InventoryCeline George

╠²

In Odoo, the least package removal strategy is a feature designed to optimize inventory management by minimizing the number of packages open to fulfill the orders. This strategy is particularly useful for the business that deals with products packages in various quantities such as boxes, cartons or palettes. LAZY SUNDAY QUIZ "A GENERAL QUIZ" JUNE 2025 SMC QUIZ CLUB, SILCHAR MEDICAL CO...

LAZY SUNDAY QUIZ "A GENERAL QUIZ" JUNE 2025 SMC QUIZ CLUB, SILCHAR MEDICAL CO...Ultimatewinner0342

╠²

Ad

Net payment method accounts

- 1. Net payment Method Under this method , consideration is ascertained by adding up the cash paid , agreed value of assets given and the agreed values of securities allotted by the transferee company to the transferor company in discharge of consideration.

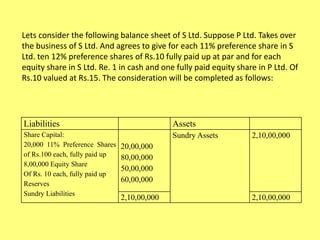

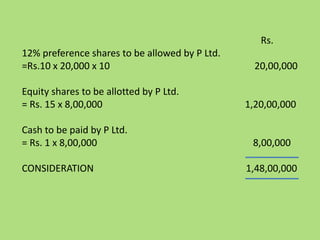

- 2. Lets consider the following balance sheet of S Ltd. Suppose P Ltd. Takes over the business of S Ltd. And agrees to give for each 11% preference share in S Ltd. ten 12% preference shares of Rs.10 fully paid up at par and for each equity share in S Ltd. Re. 1 in cash and one fully paid equity share in P Ltd. Of Rs.10 valued at Rs.15. The consideration will be completed as follows: Liabilities Assets Share Capital: 20,000 11% Preference Shares 20,00,000 of Rs.100 each, fully paid up 80,00,000 8,00,000 Equity Share 50,00,000 Of Rs. 10 each, fully paid up 60,00,000 Reserves Sundry Liabilities Sundry Assets 2,10,00,000 2,10,00,000 2,10,00,000

- 3. Rs. 12% preference shares to be allowed by P Ltd. =Rs.10 x 20,000 x 10 20,00,000 Equity shares to be allotted by P Ltd. = Rs. 15 x 8,00,000 1,20,00,000 Cash to be paid by P Ltd. = Rs. 1 x 8,00,000 8,00,000 CONSIDERATION 1,48,00,000