Economy and Everyday Life of the UK

•Download as PPT, PDF•

2 likes•5,992 views

The United Kingdom has the 6th largest economy in the world by GDP and is the 2nd largest financial economy. It transitioned from an economy based on mercantilism and manufacturing during the industrial revolution to one focused on free trade and international finance by the late 19th century. However, the two world wars devastated the UK economy. Post-war economic policies aimed to revive the economy through state involvement and joining the European Economic Community. Under Thatcher in the 1980s, privatization and deregulation reformed the economy.

Economy and Everyday Life of the UK

- 1. Economy and Everyday Life of the UK By Dasha Reznikova

- 2. The United Kingdom is the sixth largest economy in the world by nominal GDP and the sixth largest by purchasing power parity (PPP). It is the third largest economy in Europe after Germany's and France's in nominal terms and the second largest after Germany's in terms of purchasing power parity. The United Kingdom is the second largest financial economy in the World, second only to the United States and is home to many of the World’s largest banks and companies.

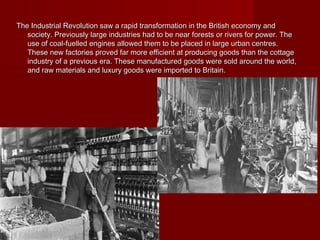

- 3. 18th century The Age of Mercantilism and the Industrial Revolution The basis of the British Empire was founded in the age of mercantilism, an economic theory that stressed maximizing the trade inside the empire, and trying to weaken rival empires. Mercantilism was the basic policy imposed by Britain on its colonies: the eastern colonies of North America, colonizations of the smaller islands of the Caribbean such as Trinidad and Tobago, the Bahamas, the Leeward Islands, Barbados, Jamaica and Bermuda. The period of time from the 1770s to the 1820s is known as the “industrial revolution”. It started with the mechanisation of the textile industries, the development of iron-making techniques and the increased use of refined coal.

- 4. The Industrial Revolution saw a rapid transformation in the British economy and society. Previously large industries had to be near forests or rivers for power. The use of coal-fuelled engines allowed them to be placed in large urban centres. These new factories proved far more efficient at producing goods than the cottage industry of a previous era. These manufactured goods were sold around the world, and raw materials and luxury goods were imported to Britain.

- 5. 19th century Free trade Railways After 1840 Britain abandoned mercantilism and committed its economy to free trade, with few barriers or tariffs. From 1815 to 1870 Britain reaped the benefits of being the world's first modern, industrialised nation. It was the 'workshop of the world', meaning that its finished goods were produced so efficiently and cheaply that they could often undersell comparable, locally manufactured goods in almost any other market.  The British invented the modern railway system and exported it to the world. For example, Thomas Brassey brought British railway engineering to the world.

- 6. During the First Industrial Revolution, the industrialist replaced the merchant as the dominant figure in the capitalist system. New products and services were also introduced which greatly increased international trade. By the 1870s, financial houses in London had achieved an unprecedented level of control over industry. Foreign trade tripled in volume between 1870 and 1914; most of the activity occurred with other industrialised countries. Britain ranked as the world's largest trading nation in 1860, but by 1913 it had lost ground to both the United States and Germany. With London as the world's financial capital, the export of capital was a major base of the British economy 1880 to 1913. It was the "golden era" of international finance.

- 7. Postwar stagnation The human and material losses of the World War in Britain were enormous. They included 745,000 servicemen killed and 24,000 civilians, with 1.7 million wounded. The total of lost shipping came to 7.9 million tons (much of it replaced by new construction), and £7,500 million in financial costs to the Empire. In 1919 Britain reduced the working hours in major industries to a 48-hour week for industrial workers. By 1921, more than 2,000,000 Britons were unemployed as a result of the postwar economic downturn.

- 8. The Great Depression In 1929, the Wall St Crash affected Britain resulting in leaving the Gold Standard. By the early 1930s, the depression again signaled the economic problems the British economy faced. In political terms, the economic problems found expression in the rise of radical movements who promised solutions which conventional political parties were no longer able to provide.

- 9. After World War II, the British economy had again lost huge amounts of absolute wealth. Both wars had demonstrated the possible benefits of greater state involvement. The Conservative Government and The Labour Party had come to the conclusion that Britain needed to enter the European Economic Community (EEC) in order to revive its economy. This decision came after establishing a European Free Trade Association (EFTA).

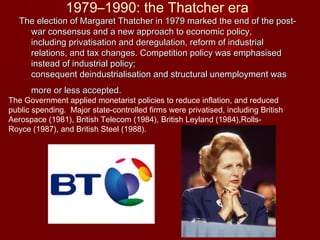

- 10. 1979–1990: the Thatcher era The election of Margaret Thatcher in 1979 marked the end of the post- war consensus and a new approach to economic policy, including privatisation and deregulation, reform of industrial relations, and tax changes. Competition policy was emphasised instead of industrial policy; consequent deindustrialisation and structural unemployment was more or less accepted. The Government applied monetarist policies to reduce inflation, and reduced public spending.  Major state-controlled firms were privatised, including British Aerospace (1981), British Telecom (1984), British Leyland (1984),Rolls- Royce (1987), and British Steel (1988).

- 11. In the Labour Party's second term in office, beginning in 2001, the party increased taxes and borrowing. The government wanted the money to increase spending on public services, notably the National Health Service, which they claimed was suffering from chronic under-funding.  Following two quarters of negative growth, Britain entered a recession in 2012.  This is the first double-dip recession since 1975.