Operation and maintenance (o&m)

•Download as PPT, PDF•

3 likes•4,002 views

This document outlines procedures for operating and maintaining public infrastructure and income-generating subprojects completed under the Kalahi-CIDSS program. It discusses how completed subprojects will be turned over to community user groups for operation and maintenance. It also describes how income-generating subprojects should have separate financial management systems to fund ongoing O&M activities through an association collecting fees. The document provides details on the financial roles and processes involved in collecting, recording, and reporting on funds to ensure the long-term sustainability of the subprojects.

Operation and maintenance (o&m)

- 1. OPERATION AND MAINTENANCE (O&M) PUBLIC INFRASTRUCTURES AND INCOME-GENERATING SUBPROJECTS

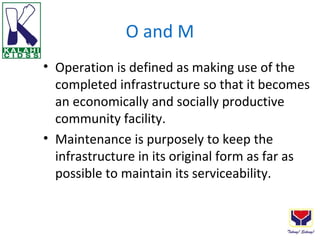

- 2. O and M • Operation is defined as making use of the completed infrastructure so that it becomes an economically and socially productive community facility. • Maintenance is purposely to keep the infrastructure in its original form as far as possible to maintain its serviceability.

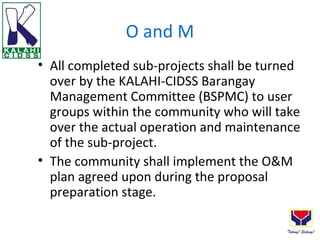

- 3. O and M • All completed sub-projects shall be turned over by the KALAHI-CIDSS Barangay Management Committee (BSPMC) to user groups within the community who will take over the actual operation and maintenance of the sub-project. • The community shall implement the O&M plan agreed upon during the proposal preparation stage.

- 5. KC Manual of Operations • SPs that are income-generating (IGPs) shall have a separate financial management systems to ensure project sustainability. • The Community shall organize and form an association for the primary purpose of generating funds to carry on the various operational and maintenance activity of the IGPs.

- 7. KC Manual of Operations • The Association shall open a bank account separate from the community bank account for the SP implementation which shall have at least two co-signatories for control purposes. • The Collector/Cashier shall issue a pre- number OR or AR or equivalent receipt in two copies for all cash collections.

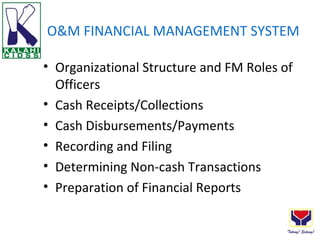

- 8. O&M FINANCIAL MANAGEMENT SYSTEM • Organizational Structure and FM Roles of Officers • Cash Receipts/Collections • Cash Disbursements/Payments • Recording and Filing • Determining Non-cash Transactions • Preparation of Financial Reports

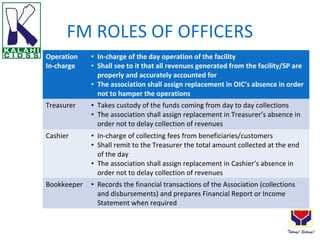

- 10. FM ROLES OF OFFICERS Operation • In-charge of the day operation of the facility In-charge • Shall see to it that all revenues generated from the facility/SP are properly and accurately accounted for • The association shall assign replacement in OIC’s absence in order not to hamper the operations Treasurer • Takes custody of the funds coming from day to day collections • The association shall assign replacement in Treasurer’s absence in order not to delay collection of revenues Cashier • In-charge of collecting fees from beneficiaries/customers • Shall remit to the Treasurer the total amount collected at the end of the day • The association shall assign replacement in Cashier’s absence in order not to delay collection of revenues Bookkeeper • Records the financial transactions of the Association (collections and disbursements) and prepares Financial Report or Income Statement when required

- 11. CASH RECEIPTS/COLLECTIONS • Cashier shall issue a pre-numbered OR or AR or equivalent receipt in 2 copies for all cash collections – Original copy to customer – Duplicate copy to file • Cashier shall accomplish List of Collection in 3 copies every day – Original copy to Treasurer – Duplicate copy to Bookkeeper – Triplicate copy to file • Treasurer shall verify cash remittances with List of Collection; record in the Treasurer’s Journal and keep cash in the Cash box for deposit the next banking day • Bookkeeper records transaction in the Cashbook

- 12. OR / AR • Color-coded: white for original copy and other color for duplicate copy • Use carbon paper to produce duplicate copy • In no case shall both copies be prepared separately Date Particular Amount OR/AR No.

- 13. LIST OF COLLECTION List of Collection Date ________________ No: ________________ No. Particular Amount OR/AR 1 2 3 4 5 Prepared by: Verified by: Recorded by: Cashier Bookkeeper Treasurer

- 14. TREASURER’S JOURNAL Date Ref Particular Receipt Disbursement Cumulative Balance

- 16. RECORDING AND FILING • Daily recording is greatly recommended • Safekeeping the books of accounts, records, accounting forms and reports are major responsibilities of the Bookkeeper • All records and documents should be locked and subjected to limited access • Association Officers should agree on report to be prepared, who received the report and how frequent is the submission

- 19. FINANCIAL REPORT PREPARATION Procedures to prepare Income Statement:

- 20. POST-AUDIT FINDINGS • Non-compliance by concerned LGUs on the allocation of funds for the operations and maintenance of SPs, affected the functionality and utilization of SPs. (Mutual Partnership Agreement) • Sustainability of some IGPs are uncertain due to failure of the Barangay Committee to comply with the requirements pertaining to the completed SPs. (KC Manual of Operations)