How P2P Finance Models Work: Risks, Controls and Regulatory Barriers

ŌĆó

1 likeŌĆó2,872 views

The document discusses peer-to-peer (P2P) finance, including how P2P models work, common risks, operational controls, and regulatory barriers. It describes that P2P platforms allow individuals to directly invest in or lend to others without platform operators taking on financial risk. Standard risks include lack of internal controls, credit/investment risk, and fraud. Common controls address governance, funds segregation, communications, and risk management. Regulatory barriers include confusion over permission needed, overlap between financial regulations, and rules discouraging competition and innovation beyond traditional products.

How P2P Finance Models Work: Risks, Controls and Regulatory Barriers

- 1. PEER-TO-PEER FINANCE POLICY SUMMIT 2012 How P2P Finance Models Work: Risks, Controls And Regulatory Barriers Simon Deane-Johns 7 December 2012 Keystone Law

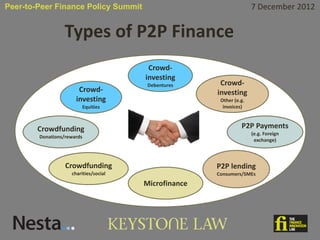

- 2. Peer-to-Peer Finance Policy Summit 7 December 2012 Types of P2P Finance Crowd- investing Debentures Crowd- Crowd- investing investing Other (e.g. Equities invoices) Crowdfunding P2P Payments (e.g. Foreign Donations/rewards exchange) Crowdfunding P2P lending charities/social Consumers/SMEs Microfinance

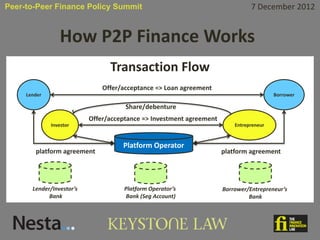

- 3. Peer-to-Peer Finance Policy Summit 7 December 2012 How P2P Finance Works Transaction Flow Offer/acceptance => Loan agreement Lender Borrower Share/debenture Offer/acceptance => Investment agreement Investor Entrepreneur Platform Operator platform agreement platform agreement Lender/InvestorŌĆÖs Platform OperatorŌĆÖs Borrower/EntrepreneurŌĆÖs Bank Bank (Seg Account) Bank

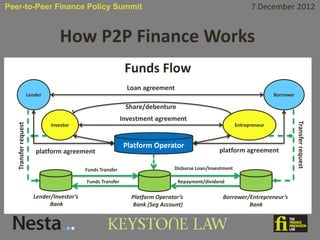

- 4. Peer-to-Peer Finance Policy Summit 7 December 2012 How P2P Finance Works Funds Flow Loan agreement Lender Borrower Share/debenture Investment agreement Transfer request Investor Entrepreneur Transfer request Platform Operator platform agreement platform agreement Funds Transfer Disburse Loan/Investment Funds Transfer Repayment/dividend Lender/InvestorŌĆÖs Platform OperatorŌĆÖs Borrower/EntrepreneurŌĆÖs Bank Bank (Seg Account) Bank

- 5. Peer-to-Peer Finance Policy Summit 7 December 2012 Common Features ŌĆó Platform operator is not a party to instrument agreed between participants ŌĆō Segregates participantsŌĆÖ funds rather than treating them as own assets; ŌĆō Margin stays with the participants; ŌĆó Online only ŌĆō> low cost ŌĆō> lower fees ŌĆó Low minimum commitment ŌĆō accessible to ordinary people ŌĆō Aids diversification of small investment amounts; ŌĆō Finance from many in small amounts at outset ŌĆō> no need to securitise; ŌĆó Data centralised to aid risk assessment, performance analysis, collections, enforcement ŌĆó Transparency and funds segregation removes ŌĆśmoral hazardŌĆÖ

- 6. Peer-to-Peer Finance Policy Summit 7 December 2012 Standard Operational Risks ŌĆó Lack of adequate internal controls, governance ŌĆō Financial mismanagement, operator insolvency; ŌĆō Internal fraud; ŌĆō lack of system integrity/availability; ŌĆō lack of business continuity; ŌĆō failure to manage/respond appropriately to customer complaints; ŌĆō Unclear, unfair or misleading promotions/communications. ŌĆó Basic credit or investment risk ŌĆó Money laundering, external Fraud

- 7. Peer-to-Peer Finance Policy Summit 7 December 2012 Common Operational Controls ŌĆó Senior management systems and controls; ŌĆó Minimum working capital; ŌĆó Segregation of participantsŌĆÖ funds; ŌĆó Clear, fair and not misleading service terms/communications/promotions; ŌĆó Secure and reliable IT systems; ŌĆó Fair complaints handling; ŌĆó Orderly administration if platform ceases to operate; ŌĆó Appropriate risk assessment, AML and anti-fraud measures ŌĆó Extra measures appropriate to specific instruments available

- 8. Peer-to-Peer Finance Policy Summit 7 December 2012 Regulatory Barriers ŌĆó Confusion as to whether you can lawfully participate on platforms; ŌĆó Tiny differences have seismic implications in permission or licence needed; ŌĆó Regulatory ŌĆścreepŌĆÖ: uncertainty/ risk aversion leads to unnecessary complexity; ŌĆó Regulatory overlap/conflict (e.g. FSMA/MiFID, Prospectus Directive/CoŌĆÖs Act); ŌĆó Different ŌĆśbusiness testŌĆÖ criteria for different activities; ŌĆó Unclear when participants might be acting in the course of a business; ŌĆó Different rules for ŌĆśpromotingŌĆÖ vs ŌĆśofferingŌĆÖ a security; ŌĆó Unregulated operators may still face rules on public offers and promotions; ŌĆó Regulators can only look inside the regulated markets to foster competition; ŌĆó Regulation (coupled with perverse tax incentives) discourages diversifying beyond regulated cash/investment products, limiting innovation and competition.