Point of Sale Industry study

?

6 likes?4,921 views

This document provides an overview of the Indian point-of-sale (POS) terminal market. It discusses the current market scenario, trends driving growth, major players and their market shares, and return on investment for POS terminals. The key points are: - India's non-cash payments account for only 0.2% of the global market but are growing rapidly. POS terminals are helping drive adoption of debit and credit cards. - There are over 4.27 lakh POS terminals deployed in India, with major bank players like ICICI, HDFC, and Axis Bank having the largest shares. - ROI on POS terminals is around 2% of transaction value. Higher transaction volumes and amounts provide better returns.

Point of Sale Industry study

- 1. Indian POS Terminal Market An overview

- 2. Agenda ? Why POS? ? Current market scenario ? RoI on a POS Terminal ? POS Business model ? Trends and growth drivers ? Major Players ? Where would I put my money?

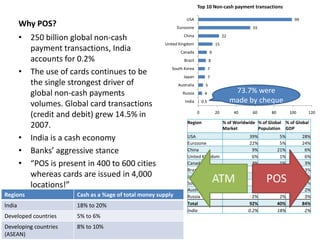

- 3. Why POS? ? 250 billion global non-cash payment transactions, India accounts for 0.2% ? The use of cards continues to be the single strongest driver of global non-cash payments volumes. Global card transactions (credit and debit) grew 14.5% in 2007. ? India is a cash economy ? BanksˇŻ aggressive stance ? ˇ°POS is present in 400 to 600 cities whereas cards are issued in 4,000 locations!ˇ± Regions Cash as a %age of total money supply India 18% to 20% Developed countries 5% to 6% Developing countries (ASEAN) 8% to 10% 0.5 4 5 7 7 8 9 15 22 55 99 0 20 40 60 80 100 120 India Russia Australia Japan South Korea Brazil Canada United Kingdom China Eurozone USA Top 10 Non-cash payment transactions 73.7% were made by cheque Region % of Worldwide Market % of Global Population % of Global GDP USA 39% 5% 28% Eurozone 22% 5% 24% China 9% 21% 6% United Kingdom 6% 1% 6% Canada 3% 1% 3% Brazil 3% 3% 3% Japan 3% 2% 9% South Korea 3% 1% 2% Australia 2% 0.3% 2% Russia 2% 2% 3% Total 92% 40% 84% India 0.2% 18% 2% ATM POS

- 4. ICICI Bank, 180,000 Axis Bank, 114,500 HDFC , 70,000 HSBC, 15,000 POS Terminals 4.27 Lakh POS Terminals deployed Key players: 1. Venture Infotek 2. Prizm Payments 3. MRL Posnet 4. Reliance Money* 5. Financial Technologies 6. TVS-Electronics Cash that moved through POS in 2008-09: Rs. 83,903 crores. Card issuer Bank Merchant Cards issued Merchant Acquirer Bank Visa/ Mastercard Settlement Gateway 1% to 1.2% Rs. 839 crores to Rs. 1,007 crores 0.3% to 0.5% Rs. 250 crores to Rs. 420 crores 0.3% to 0.7% Rs. 250 crores to Rs. 600 crores ICICI, 70 .00 HDFC, 4 0.30 HSBC, 3 5.00 SBI, 27.0 0 Citibank , 25.00 Credit Card Base: 247 Lakhs SBI, 406 ICICI, 140.00 Axis Bank, 117.00 HDFC, 90.00 Punjab National Bank, 67.00 Canara Bank, 57.50 Andhra Bank, 40.78 Bank of Baroda, 35.00 Debit Cards Base: 1,374 Lakhs

- 5. ? All banks pushing debit cards. ? Expectation from increasing penetration of POS terminals ¨C to increase average annual spend per debit card. 19557 17888 21049 26461 1185 1090 1222 1350 2006 2007 2008 2009 Average annual credit card spend (INR) Average annual debit card spend (INR) 25686 33886 41361 57985 65356 5361 5897 8172 12521 18547 2005 2006 2007 2008 2009 Credit Card (INR Crores) Debit Cards (INR Crores) 141.05 173.27 231.23 275.47 246.99 226.64 355.01 497.63 749.76 1024.37 1374.31 1732.75 2005 2006 2007 2008 2009 2010 (P) Credit card base (in Lakhs) Debit card base (in Lakhs) Cards market Share at POS terminals Average annual spend per card

- 6. ROI on a POS Terminal Bank Merchant Bank partner 1. +20% rule 2. CRM: Cash Register Management! 3. MDR v/s Opportunity cost 4. Bank Relationship Management 1. SBI: 5,00,000 POS Terminals over the next 3 years. 5. Merchant classification Monthly card business (INR) Avg. per transaction No. of transactions Variable cost (Re 1/-) 2% Rental Total cost % cost 1,00,000 500 200 200 2,000 200 2,400 2.40% 2,50,000 700 357 357 5,000 200 5,557 2.22% 5,00,000 1,000 500 500 10,000 200 10,700 2.14% 7,50,000 1,200 625 625 15,000 200 15,825 2.11% 10,00,000 2,000 500 500 20,000 200 20,700 2.07% 12,50,000 2,000 625 625 25,000 200 25,825 2.07% 15,00,000 2,500 600 600 30,000 200 30,800 2.05% 20,00,000 2,500 800 800 40,000 200 41,000 2.05% 25,00,000 3,000 833 833 50,000 200 51,033 2.04% 50,00,000 5,000 1,000 1,000 1,00,000 200 1,01,200 2.02%

- 7. POS Business Models ? Bank acquires merchant ? Bank installs own POS ? Bank maintains POS ? Bank charges rental, transaction fees and maintenance fees from merchant. ? BP acquires merchant ? BP takes POS on lease from Bank ? BP installs POS ? BP maintains POS for a rental from merchant/ transaction %age.

- 8. Trends and Growth drivers ? Debit card transactions v/s credit card ? SBIˇŻs plans ? Hindrances in implementation of mobile payments ¨C Interoperability ¨C RBI regulations ? Prepaid/ smart/ sim cards ? Indiapay

- 9. ATM Payment Processing Network POS Payment Processing Network 58,000+ INR 6,16,456 crores 235 Crores 4.27 Lakh INR 83,903 crores 39 Crores CBS CBS ATM ATM NFS POS Visa/ Mastercard settlement gateway Merchant Bank payment gateway Merchant Bank payment gateway POS POS POS POS

- 10. Before Indiapay After Indiapay Visa/ Mastercard settlement gateway Merchant Bank payment gateway Merchant Bank payment gateway POS POS POS POS INDIAPAY Merchant Bank payment gateway Merchant Bank payment gateway POS POS POS POS

- 11. Major Players ? Problems plaguing these players: ¨C Per terminal revenue: Rs. 50/- to Rs. 55/- per year ¨C Merchant acquisition ¨C Rural strategies and regulatory constraints Company Annual Revenue Installed base USP Venture funded by Venture Infotek INR 80 crores in FY 2009 (E) 1,60,000 First-mover Promoters Prizm Payments About a crore (E) 3,500 End-to-end solution provider Sequoia

- 12. Where would I put my money? ? Nascent phase of the industry. ¨C POS and ATM are driving card adoption ? POS terminal installation and maintenance is a small market and a low margin game. ¨C Very small market, about Rs. 400 crores annually. ¨C Volumes are growing, but ATMs already there. ¨C Might become door-openers for pure ATM manufacturers like Vortex to increase their margins. ¨C Prizm and Venture Infotek exploring tie-ups with Vortex for inclusion of ATMs in their portfolio.

- 13. Thank You VenturEast Tenet Fund II

Editor's Notes

- In just six years (between 2001 and 2007), developing countriesˇŻ share has jumped from 9% to 20%, led by CEMEA and BRIC (Brazil, Russia, India and China), in which annual growth was around 25% during the 2001-07 period.

- Debit cards accounted for 57.5% of total non-cash purchase transactions in 2008, up from 22.9% just ten years earlier. Debit cards first overtook credit cards as the preferred means of US consumer payments in 2004, and their rise has been notable ever since. Still, the economic downturn made credit cards even less popular in 2008, and the debit cardsˇŻ share of transactions grew by 5 percentage points from 2007.