Pramod kumar form_vs_substance_fit_06_december_2012

- 1. Pramod Kumar International Taxation Conference ¨C FIT, India December 6,2012 Pramod Kumar International Taxation Conference, Mumbai ? December 6, 2012.

- 2. This presentation seeks to present the factual and legal elements relating to various points of view about the concept of substance over form in Indian Tax laws. This presentation is only a compilation of such points of view and does not canvass or support any particular point of view. The views expressed herein, therefore, do not necessarily reflect the views or the understanding of the author or his employer i.e. the Income Tax Appellate Tribunal, Government of India. This presentation deals only with the judicial doctrine of substance over form, and does not deal with GAAR, on which a separate presentation is being made later, as also on statutory provisions dealing with substance over form.

- 3. ? Doctrine of substance over form is a judicial creation. It is invoked in cases in which taxpayer has conducted a scheme of transactional relationships in documents and has a view on tax advantages that flow from tax reporting based on such transactional relationships, rather than on the substance of arrangement. The economic reality is thus hidden and transaction exists in form only. ? This doctrine allows tax authorities to ignore the legal form of an arrangement and to look at its actual substance, so as to prevent artificial structures from being used for tax avoidance purposes.

- 4. ? In its pure form, when, on the basis of evaluation of evidence and analysis of facts, judicial authorities find that tax motivation outweighs business purpose or profit objective, it is held that the taxpayer?s efforts of form does not reflect the substance of economic transactions, and intended tax benefits are declined. ? Recent Indian decisions, however, can be viewed as proceeding on the basis that substance prevails over form only when the form has no commercial justification whatsoever and is completely tax driven.

- 5. ? It is extremely difficult, if not altogether impossible, for legislation to keep pace with dynamism of, and innovations in, business and commerce, and therefore, normative systems, which legal provisions inherently are, cannot effectively handle the aggressive tax positions taken by the businesses. ? This doctrine provides flexibility to judges to deal with the cases not visualized by the legislature and, as a judicial doctrine, it is inherently more flexible than a statutory rule, it can develop gradually and it cannot be undermined by microscopic examination in search of loopholes.

- 6. ? Substance over form is one of the fundamental tax issues debated right from the initial days of tax laws in India, but initial controversies about characterization of income and expenditure, and nomenclature assigned to the same by the taxpayers. Relatively simple matters and no major issues arose on application of this doctrine. ? The focus is now due to revenue?s challenge to investment and transaction structures on the basis that use of intermediate companies is for dominant purpose of obtaining tax benefits ¨C through treaty or otherwise. Relatively complex issues but doctrine of substance over form applied mainly when the structure is completely tax driven and devoid of any commercial justification whatsoever.

- 7. ? Judiciary cannot be a silent spectator when facts and circumstances clearly warrant the inference that there has been a dubious, though seemingly legal, method adopted with the sole motive of avoiding taxes. ? The role played by judges while handling tax cases is a tight rope walk. On the one hand, they should be entirely neutral towards the parties, even if not value neutral, and, on the other hand, their judgments should be objective, fair, reasonable and unaffected by their ideologies. Indian judicial doctrine on the substance over form, by and large, reflect this position.

- 8. ? Not everyone in the judiciary is, or can be, really confident in meeting the challenge of looking through the complex maze of contrived transactions, and understanding the core economic and business realities of such transactions. Is that the reason, as many believe, judiciary prefers to go by the form and prone to err on the side of excessive caution at the cost of the exchequer ? ? Should the judiciary be content with foundationalist approach to interpretation of tax statutes by implementing its plain meaning, intent or purpose, or has the time come that judges should approach the tax statutes by exploring for most sensible policy option. Will latter will essentially lead to more emphasis on substance over form ?

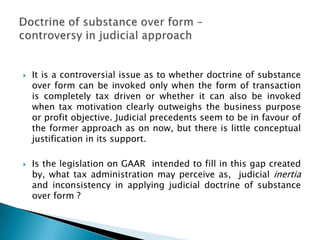

- 9. ? It is a controversial issue as to whether doctrine of substance over form can be invoked only when the form of transaction is completely tax driven or whether it can also be invoked when tax motivation clearly outweighs the business purpose or profit objective. Judicial precedents seem to be in favour of the former approach as on now, but there is little conceptual justification in its support. ? Is the legislation on GAAR intended to fill in this gap created by, what tax administration may perceive as, judicial inertia and inconsistency in applying judicial doctrine of substance over form ?

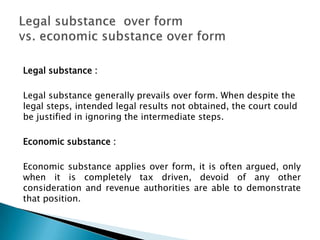

- 10. Legal substance : Legal substance generally prevails over form. When despite the legal steps, intended legal results not obtained, the court could be justified in ignoring the intermediate steps. Economic substance : Economic substance applies over form, it is often argued, only when it is completely tax driven, devoid of any other consideration and revenue authorities are able to demonstrate that position.

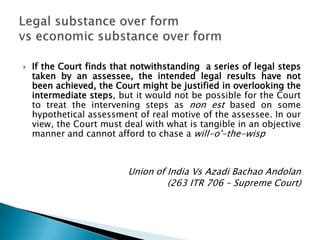

- 11. ? If the Court finds that notwithstanding a series of legal steps taken by an assessee, the intended legal results have not been achieved, the Court might be justified in overlooking the intermediate steps, but it would not be possible for the Court to treat the intervening steps as non est based on some hypothetical assessment of real motive of the assessee. In our view, the Court must deal with what is tangible in an objective manner and cannot afford to chase a will-o'-the-wisp Union of India Vs Azadi Bachao Andolan (263 ITR 706 ¨C Supreme Court)

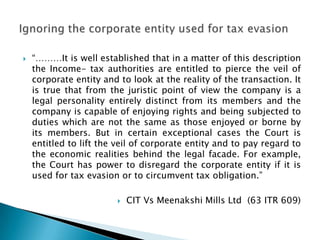

- 12. ? ¡°¡¡¡It is well established that in a matter of this description the Income- tax authorities are entitled to pierce the veil of corporate entity and to look at the reality of the transaction. It is true that from the juristic point of view the company is a legal personality entirely distinct from its members and the company is capable of enjoying rights and being subjected to duties which are not the same as those enjoyed or borne by its members. But in certain exceptional cases the Court is entitled to lift the veil of corporate entity and to pay regard to the economic realities behind the legal facade. For example, the Court has power to disregard the corporate entity if it is used for tax evasion or to circumvent tax obligation.¡± ? CIT Vs Meenakshi Mills Ltd (63 ITR 609)

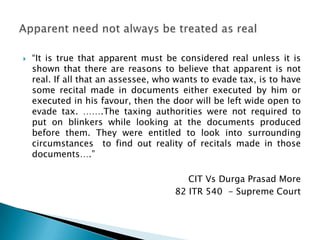

- 13. ? ¡°It is true that apparent must be considered real unless it is shown that there are reasons to believe that apparent is not real. If all that an assessee, who wants to evade tax, is to have some recital made in documents either executed by him or executed in his favour, then the door will be left wide open to evade tax. ¡¡.The taxing authorities were not required to put on blinkers while looking at the documents produced before them. They were entitled to look into surrounding circumstances to find out reality of recitals made in those documents¡.¡± CIT Vs Durga Prasad More 82 ITR 540 - Supreme Court

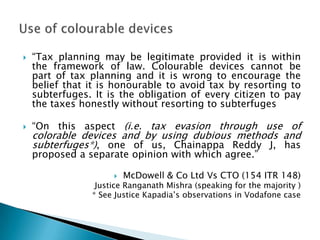

- 14. ? ¡°Tax planning may be legitimate provided it is within the framework of law. Colourable devices cannot be part of tax planning and it is wrong to encourage the belief that it is honourable to avoid tax by resorting to subterfuges. It is the obligation of every citizen to pay the taxes honestly without resorting to subterfuges ? ¡°On this aspect (i.e. tax evasion through use of colorable devices and by using dubious methods and subterfuges*), one of us, Chainappa Reddy J, has proposed a separate opinion with which agree.¡± ? McDowell & Co Ltd Vs CTO (154 ITR 148) Justice Ranganath Mishra (speaking for the majority ) * See Justice Kapadia?s observations in Vodafone case

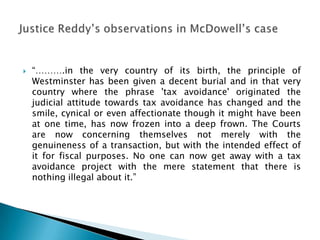

- 15. ? ¡°¡¡¡.in the very country of its birth, the principle of Westminster has been given a decent burial and in that very country where the phrase 'tax avoidance' originated the judicial attitude towards tax avoidance has changed and the smile, cynical or even affectionate though it might have been at one time, has now frozen into a deep frown. The Courts are now concerning themselves not merely with the genuineness of a transaction, but with the intended effect of it for fiscal purposes. No one can now get away with a tax avoidance project with the mere statement that there is nothing illegal about it.¡±

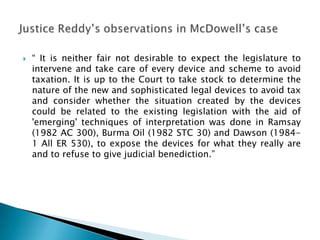

- 16. ? ¡° It is neither fair not desirable to expect the legislature to intervene and take care of every device and scheme to avoid taxation. It is up to the Court to take stock to determine the nature of the new and sophisticated legal devices to avoid tax and consider whether the situation created by the devices could be related to the existing legislation with the aid of 'emerging' techniques of interpretation was done in Ramsay (1982 AC 300), Burma Oil (1982 STC 30) and Dawson (1984- 1 All ER 530), to expose the devices for what they really are and to refuse to give judicial benediction.¡±

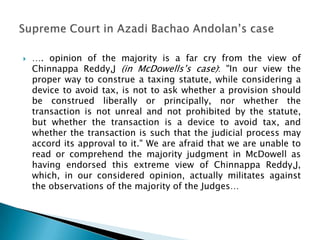

- 17. ? ¡. opinion of the majority is a far cry from the view of Chinnappa Reddy,J (in McDowells?s case): "In our view the proper way to construe a taxing statute, while considering a device to avoid tax, is not to ask whether a provision should be construed liberally or principally, nor whether the transaction is not unreal and not prohibited by the statute, but whether the transaction is a device to avoid tax, and whether the transaction is such that the judicial process may accord its approval to it." We are afraid that we are unable to read or comprehend the majority judgment in McDowell as having endorsed this extreme view of Chinnappa Reddy,J, which, in our considered opinion, actually militates against the observations of the majority of the Judges¡

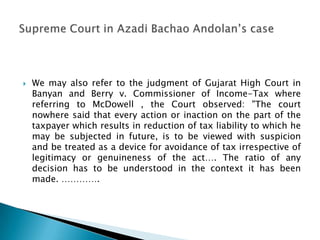

- 18. ? We may also refer to the judgment of Gujarat High Court in Banyan and Berry v. Commissioner of Income-Tax where referring to McDowell , the Court observed: "The court nowhere said that every action or inaction on the part of the taxpayer which results in reduction of tax liability to which he may be subjected in future, is to be viewed with suspicion and be treated as a device for avoidance of tax irrespective of legitimacy or genuineness of the act¡. The ratio of any decision has to be understood in the context it has been made. ¡¡¡¡.

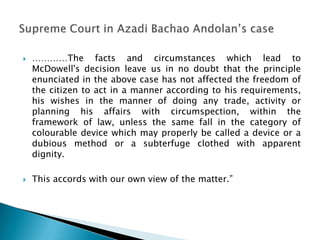

- 19. ? ¡¡¡¡The facts and circumstances which lead to McDowell's decision leave us in no doubt that the principle enunciated in the above case has not affected the freedom of the citizen to act in a manner according to his requirements, his wishes in the manner of doing any trade, activity or planning his affairs with circumspection, within the framework of law, unless the same fall in the category of colourable device which may properly be called a device or a dubious method or a subterfuge clothed with apparent dignity. ? This accords with our own view of the matter.¡±

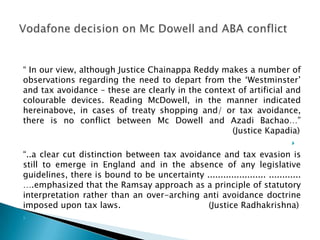

- 20. ¡° In our view, although Justice Chainappa Reddy makes a number of observations regarding the need to depart from the ?Westminster? and tax avoidance ¨C these are clearly in the context of artificial and colourable devices. Reading McDowell, in the manner indicated hereinabove, in cases of treaty shopping and/ or tax avoidance, there is no conflict between Mc Dowell and Azadi Bachao¡¡± (Justice Kapadia) ? ¡°..a clear cut distinction between tax avoidance and tax evasion is still to emerge in England and in the absence of any legislative guidelines, there is bound to be uncertainty ...................... ............ ¡.emphasized that the Ramsay approach as a principle of statutory interpretation rather than an over-arching anti avoidance doctrine imposed upon tax laws. (Justice Radhakrishna) ?

- 21. ? ¡°When it comes to taxation of a holding structure, the burden is on the Revenue to allege and establish tax abuse, in the sense of tax avoidance in the creation and/ or use of such structure(s).¡± ? ¡°In the application of a judicial anti avoidance rule, the Revenue may invoke the ¡°substance over form¡± principle or ¡°piercing the corporate veil¡± test only after it is able to establish, on the basis of facts and circumstances surrounding the transaction that the impugned transaction is a sham or tax avoidant.¡±

- 22. ? ¡°To give an example, if a structure is used for circular trading or round tripping or to pay bribes then such transactions, though having a legal form, should be discarded by applying the test of fiscal nullity. Similarly, in a case where the Revenue finds that in a Holding Structure an entity which has no commercial/business substance has been interposed only to avoid tax then in such cases applying the test of fiscal nullity it would be open to the Revenue to discard such interpositioning of that entity. However, this has to be done at the threshold.¡± ? ¡°It is the task of the Revenue/Court to ascertain the legal nature of the transaction and while doing so it has to look at the entire transaction as a whole and not to adopt a dissecting approach.¡±

- 23. ? ¡°...we are of the view that every strategic foreign direct investment coming to India, as an investment destination, should be seen in a holistic manner. While doing so, the Revenue/Courts should keep in mind the following factors: the concept of participation in investment, the duration of time during which the Holding Structure exists; the period of business operations in India; the generation of taxable revenues in India; the timing of the exit; the continuity of business on such exit. In short, the onus will be on the Revenue to identify the scheme and its dominant purpose.¡± Although there is a mention of ?dominant purpose? of the scheme here, earlier observations refer to discarding the structure when it has ¡°no commercial/ business substance¡±.

- 24. The doctrine of substance over form well entrenched in Indian tax laws, even as its application may not be as uniform and consistent as aggressively pursued by the revenue authorities. It is only in extreme cases where form of a transaction is not at all defensible on commercial basis (other than for tax planning) that the doctrine of substance over form is invoked. As long as there is some commercial justification for the form of a transaction, judiciary generally refrains from invoking it Schemes and transactions where economic substance is significantly different from the legal form, or where an entity without economic substance is used in a transaction, are at risk.

- 25. Thank you ! pramod.kumar@itat.nic.in