More Related Content

What's hot (20)

Viewers also liked (7)

Similar to Presentation on Income Tax Deductions (20)

Presentation on Income Tax Deductions

- 1. 1

- 2. (I) (a) Individual/HUF/AOP/BOI and every artificial judicial person 2 Level of Total Income Rate Of Income Tax Where the total income does not exceed Rs 2,50000 NIL Where the total income does exceed Rs 2,50000 but does not exceed Rs 5,000,00. 10% of the amount by which the total income exceeds Rs 2,50000. Where the total income does exceed Rs 5,000,00. but does not exceed Rs 10,000,00. Rs 25000 plus 20% of the amount by which the total income exceeds Rs 5,000,00. Where the total income does exceed Rs 10,000,00. Rs 1,25000 plus 30% of the amount by which the total income exceeds Rs 10,000,00.

- 3. (b) Resident Individual of age of 60 years or more but less than 80 Years at any time during the financial year 3 Level of Total Income Rate Of Income Tax Where the total income does not exceed Rs 30,0000 NIL Where the total income does exceed Rs 30,0000 but does not exceed Rs 5,000,00. 10% of the amount by which the total income exceeds Rs 30,0000. Where the total income does exceed Rs 5,000,00. but does not exceed Rs 10,000,00. Rs 20000 plus 20% of the amount by which the total income exceeds Rs 5,000,00. Where the total income does exceed Rs 10,000,00. Rs 1,20000 plus 30% of the amount by which the total income exceeds Rs 10,000,00.

- 4. (c) For Resident Individual of age of 80 years or more at any time during the financial year 4 Level of Total Income Rate Of Income Tax Where the total income does not exceed Rs 50,0000 NIL Where the total income does exceed Rs 50,0000 but does not exceed Rs 10,000,00. 20% of the amount by which the total income exceeds Rs 50,0000. Where the total income exceeds Rs 10,000,00. Rs 1,00000 plus 30% of the amount by which the total income exceeds Rs 10,000,00.

- 5. Other Types Of Assesse (ii) Co-operative Society: - There is no change in the rate structure as compared to assessment year 2015-16. (iii) Firm/Limited Liability Partnership: - The rate of tax for AY 2016-17 is 30% on the whole of the total incomeof the firm. The rate would apply to LLP also. 5 Level of Total Income Rate of Income Tax Where the total income does not exceed Rs 10000. 10% of total income. Where the total income does exceed Rs 10000 but does not exceed Rs 20000. Rs 1000 plus 20% of amount by which the total income exceeds Rs 10000. Where the total income exceeds Rs 20000. Rs 3000 plus 30% of amount by which the total income exceeds Rs 20000.

- 6. (iv) Local Authority: -The rate of tax for local authority is 30% on the whole of the total income of the local authority. (v) Company: - 6 In the case of a domestic company. 30% of Total Income. In the case of companies other than domestic company. 40% of Total Income.

- 7. Basic Terminology Used i. Previous Year: - As per the income tax act 1961, previous year means the financial year immediately preceding the assessment year. ii. Assessment Year: - Assessment year is basically a 12 months period starting from April 1, during which an assesse is required to file the return of income (ITR) and the ITO has to initiate assessment proceedings for income as per ITR and tax thereon. Since Income Tax is on income of a financial/ previous year or period, so tax filings and assessment can start thereafter. Probably, thatŌĆÖs why itŌĆÖs called assessment year/ period. iii. Surcharge: - An additional tax i.e. not included in the existing tax which is chargeable when the total income exceeds Rs 1crore. iv. Co-operative Society: - A co-operative is an autonomous association of people united voluntarily to meet their common economic, social, and cultural needs and aspirations through a jointly owned and democratically controlled business. 7

- 8. V Circular: - It is internal memorandum or note of the ministry/department which may clarify certain aspect of law. It may be superseded by yet another circular or amendment. VI Notification: - It is a public notification in official gazette. In various enactments we see phrases such as ŌĆ£as may be prescribedŌĆØ. These are later notified through notification. Notifications are integral part of enactment. VII Amendment: - Change in legal document made by adding, altering, or omitting a certain part or term. Amended documents when properly executed retain the legal validity of original documents. VIII Official Gazette: - It is a public journal and it prints official notices from the government. It is strictly in accordance with the government policies and decisions. It is published weekly by department of publication , ministry of urban development. 8

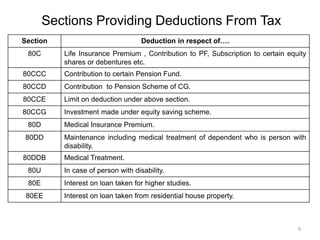

- 9. Sections Providing Deductions From Tax 9 Section Deduction in respect ofŌĆ”. 80C Life Insurance Premium , Contribution to PF, Subscription to certain equity shares or debentures etc. 80CCC Contribution to certain Pension Fund. 80CCD Contribution to Pension Scheme of CG. 80CCE Limit on deduction under above section. 80CCG Investment made under equity saving scheme. 80D Medical Insurance Premium. 80DD Maintenance including medical treatment of dependent who is person with disability. 80DDB Medical Treatment. 80U In case of person with disability. 80E Interest on loan taken for higher studies. 80EE Interest on loan taken from residential house property.

- 10. 10 Section Deduction in respect ofŌĆ”. 80GGA Certain donations for scientific research or rural development. 80GGB Contribution given by companies to political parties or electoral trust. 80GGC Contribution given by any person to political parties or electoral trust. 80JJAA Employment of new workmen. 80LA Certain incomes of offshore banking unit & International Financial Service centre. 80QQB Royalty Income etc of authors for certain books other than text books. 80RRB Royalty on Patents. 80TTA Interest on Deposits in Saving Accounts.

- 11. Overlook on Few Important Sections Section 80C: - Deductions under this section shall be allowed to individual or HUF. Eligible Amount: - Any sum paid or deposited by the assesse- 1. As life insurance premium to keep in force the insurance on life of (a)self , spouse and any child in case of individual and (b) any member in case of HUF. 2. A five year term deposit in an account under the post office time deposit Rules 1981. 11 Policy Issued before 1st April 2012 20% of actual capital sum assured. Policy Issued after 1st April 2012 10% of actual capital sum assured. Policy Issued on or after 1st April 2013- In case of person with disability or person with severe disability or suffering from disease or ailment 15% of actual capital sum assured.

- 12. 3. A subscription to any notified bonds of National Bank for Agriculture and Rural Development(NABARD). 4. A Term Deposit(Fixed Deposit) for 5 years or more with any scheduled bank in accordance with a scheme framed by central government. 5. Tuition fees( excluding any payment towards any development fees or donation or payment of similar nature), to any university, college, school or other educational institution situated within India for the purpose of full time education of any two children of individual. 6. Subscription to National Saving Certificates(NSC). 7. Any sum deposited in a 10 years or 15 years account under the post office saving bank rules 1959 in the name of self, and as a guardian of minor in case of individual and in name of any member in case of HUF. 8. Any contribution by any individual to statutory provident fund. 9. Any contribution to public provident fund in the name of self, spouse and any child in case of individual. 12

- 13. Extent of deduction: - 100% of amount invested or Rs 1,500,00 whichever is less. Section 80D: - Deduction in respect of Medical Insurance Premium (Individual & HUF) a) Up-to Rs 25000 to an assesse being an individual in respect of- (1) Health Insurance premium, paid by any mode, other than cash, to effect or to keep in force an insurance on the health of assesse or his family(spouse and dependent children); (2) Any contribution made to the central government health scheme or any other notified scheme. (3) Any payment made on account of preventive health check of the assesse and his family. In case any of the above person is of the age of 60 years or more than the deduction has been raised to Rs 30000. (b) An additional deduction of Rs 25000 is provided to an individual to keep in force insurance on the health of his or her parent or parents. In case any of the above person is of the age of 60 years or more than the deduction has been raised to Rs 30000. 13

- 14. For Super Senior Citizens: - As a welfare mechanism for the super senior citizens who are unable to get health insurance coverage, Section 80(D) has been amended to provide that deduction of up-to Rs 30000 would be allowed in respect of any payment made on account of medical expenditure in respect of a very senior citizen, if no payment has been made to keep in force an insurance on the health of such person. Maximum Rs 5000 allowed as deduction for aggregate of preventive health check up expenditure subject to overall limit of Rs 25000 or Rs 30000 as the case may be. Example: - Mr Arjun(52 years old) furnish the following particulars: - 14 S. No Particulars Amount(Rs) 1. Premium paid for insuring the health of ŌĆó Self ŌĆó Spouse ŌĆó Dependent son ŌĆó Mother 10,000 8,000 4,000 18,000 2. ŌĆó Paid for preventive health check up of

- 15. Compute the deductions available to Mr. Arjun under Section 80D for the AY 2016-17. Solution: - 15 ŌĆó Self ŌĆó Spouse ŌĆó Mother 2,000 1,500 4,000 3. Incurred medical expenditure of Rs 25,000 and Rs 15,000 for his mother, aged 80 Years and father aged 85 Years. Both mother and father are resident of India. S.No Particulars Amount(In Rs) 1. Premium paid for insuring the health of ŌĆó Self ŌĆó Spouse ŌĆó Dependent Children 10,000 8,000 4,000 Total 22,000 Preventive Health Check up of ŌĆó Self ŌĆó Spouse 2000 1500 Total 3500 25,500 Maximum Deduction 25,000

- 16. 16 Aggregate deduction is restricted to 25,000 2. In respect of payment of life insurance premium of ŌĆó Mother 18,000 Preventive Health check up of ŌĆó Mother (Rs 4000 but restricted to only Rs 2000;being Rs 3000 is utilised earlier by Mr Arjun). 2000 Medical Expenditure incurred for his father aged 85 Years. 15000 Total Deduction 35000 Amount of deduction restricted to 30000 Total Deduction under 80 D 55,000

- 17. Section 80DD: - Deduction in respect of maintenance including medical treatment of dependant who is a person with disability: - i. Section 80DD provides for a deduction of Rs 75,000 to an individual or HUF who is resident in India, who has incurred- (a) Expenditure for the medical treatment(including nursing), training and rehabilitation of a dependent, being a person with disability or, (b) paid any amount to LIC or any other insurer in respect of a scheme for the maintenance of a disabled dependent. If the dependent is suffering from severe disability the deduction under section 80DD is Rs 1,25000. Section 80 U: - It provides for the deduction of Rs 75,000 to an individual being a resident who at any time during the previous year is certified by the medical authority to be a person with disability. If the person is suffering from severe disability then deduction available under this section is Rs 1,25000. 17

- 18. Section 80DDB: -Deduction in respect to medical treatment, Etc Where an assesse who is a resident in India has, during the previous year actually paid any amount for the medical treatment of such disease or ailment as may be specified in the rules made in this behalf by the board- (a) For himself or a dependent, in case the assesse is an Individual. (b) For any member of a HUF, in case the assesse is Hindu Undivided Family. The assesse shall be allowed a deduction of the amount actually paid or a sum of Rs 40000 whichever is less in the year in which such amount was actually paid. Further, in order to remove hardship this section has been amended to provide that assesse will be required to obtain a prescription for such medical treatment from a specialised doctor for availing this deduction. The requirement; that such specialist should be working in a government hospital has been removed. 18

- 19. (c) A higher deduction of up to Rs 60000 is allowed, where the expenditure is in respect of senior citizen i.e. residential individual who is of the age of Rs 60 years or more at any time during the relevant financial. (d) Further it has been provided to provide for higher limit of deduction of up to Rs 80000 for the expenditure incurred in respect of medical treatment of himself or a dependent being a ŌĆ£very senior citizenŌĆØ. Section 80TTA: - Deduction shall be available on Interest earned by the assesse on its saving account in: - ŌĆó Bank ŌĆó Cooperative Banks ŌĆó Post Office However no deduction shall be available in respect of fixed deposits. Amount of deductions: - (i) In case where the amount of such income does not exceed in aggregate Rs 10000, the whole of such amount , and (ii) In any other case Rs 10000. 19

- 20. Section-80E: - Deduction in respect of Interest on loan taken for Higher Education. (1) In computing the total income of an assesse, being an individual, there shall be deducted any amount paid by him in previous year, out of his income chargeable to tax, by way of interest on loan taken by him from any financial institution or any approved charitable institution for the purpose of pursuing his higher education or for the purpose of higher education of his relative. (2) The deduction specified in sub section(1) shall be allowed in computing the total income in respect of assessment year and 7 assessment years immediately succeeding the initial assessment year or until the interest referred to in subsection (1) is paid by assesse in full, whichever is earlier. 20

- 21. Topic For Our Next Interaction Would be- ŌĆśTAX- Present & FutureŌĆÖ 21