Principles of accounts sba

•Download as DOCX, PDF•

93 likes•228,073 views

This document is an accounting project submitted by Anna Kay Blake for her Principles of Accounts certification. It contains the accounting records for Blanna's Fashion Boutique for the period ending September 30, 2011. The records include various journals, ledgers, trial balance, stock valuation and other financial statements that provide details of the business transactions and financial position of the boutique. The aim of the project is to demonstrate Anna's understanding of business accounting and to analyze the strengths and weaknesses of Blanna's Fashion Boutique.

Principles of accounts sba

- 1. Principles of Accounts School-Based Assessment On Blanna’s Fashion Boutique Submitted by : Anna Kay Blake Registration number: 1000290074 Submitted To: The Donald Quarrie High School School code: 100029 Territory: Jamaica This project is submitted in partial fulfillment of the requirements for certification in Principles of Accounts by the Caribbean Examinations Council (CXC)

- 2. Title Page Accounting Records Of Blanna’s Fashion Boutique

- 3. Acknowledgement I would like to express my sincere gratitude to all the persons who have been helpful towards the successful completion of this assignment. First and foremost I would like to thank Shadae Russell, Shakeyra Millington, Jonathon Butler and Ovasha Bartley for their support and assistance towards carrying out the research to complete this assignment. Secondly I want to thank my guardians for providing me with the suitable materials to finalize this assignment. I would also like to thank Mrs. K. Elliot for her assistance and guidance in completing this project. Last but certainly not least I would like to thank God for his extended mercies unto me.

- 4. Introduction This assignment is about a business that started approximately three (3) years ago which is situated in a busy area that allows it to generate large amounts of money each day to carry out its operations. This assignment contains all the information about this Blanna’s Fashion Boutique business. The information which this assignment contains includes the financial records for the period ending September 30 2011. This assignment serves to keep track of all the money that goes inside the business bank account, all the cash which the business uses within visiting the business bank account, all the money that goes outside of the business bank account, all the money that came into the business by cash and not with the use of cheques and the purposes for each transaction. Therefore this assignment provides a clear understand of all the operations the business under goes on a day to day basis.

- 5. Table of Contents Headings Page # Cover Page I Title Page II Acknowledgement III Introduction IV Aim of the Project 1 Description of Business Entity 2 Mission Statement 3 Logo and Slogan 4 Accounting Cycle 5 Accounting Information Journals 6-7 Cash Book 8 Ledgers 9-13 Trial Balance 14 Stock Valuation 15-19 Trading, Profit and Loss and Appropriation A/c 20-21 Balance Sheet 22

- 6. Bank Reconciliation Statement 23 Accounting Ratios 24-25 Performance of the Business 26 Comparisons 27 Recommendations and Suggestions 28 Conclusion 29 Appendix Price list (showing mark up %) 30 Diagrams Charts and Graphs Pictures Invoices, Cheques, Receipts etc References

- 7. Aim of the Project The aim of this project is:  To arrive at a comprehensive understanding of the financial sector of businesses.  To highlight the strength and the weaknesses of the Blanna’s Fashion Boutique business.  To present the financial records for the year ended September 30, 2011 for Blanna’s Fashion Boutique business.

- 8. Description of Business Entity Blanna’s Fashion Boutique is a partnership. This business is owned and operated by Anna Kay Blake, Shadae Russell and Ovasha Bartley a Group of ambitious young ladies. Our main aim is to make a profit while catering for the needs of the community which it is situated in. Blanna’s Fashion Boutique is situated in Montego Bay at the Blue diamond plaza 10 Pearl Street. This business has been in existence since June 20, 2008. We employ approximately fifteen (15) workers. We cater for the petite to the full figured women. We produce a wide variety of slippers, pants, skirts, handbags and accessories. Prices are always lower than that of our competitors. In cases of fashion emergencies you can call us at (1876) 3553980/4275646 or email us at Blanna’s_EmergencyStop5@yahoo.com.

- 9. The mission of Blanna’s Fashion Boutique is to:  Provide the latest fashion for all females  Provide goods and services at a reasonable cost  Ensure that the quality of our goods meets the standards of our business.  Ensure that whatever the business do doesn’t affect the environment negatively.  Provide employment for members of the community  Provide sponsors to underprivileged children Blanna’s Fashion Boutique Mission Statement

- 10. Logo and Slogan Logo Slogan With passion we send out the latest fashion

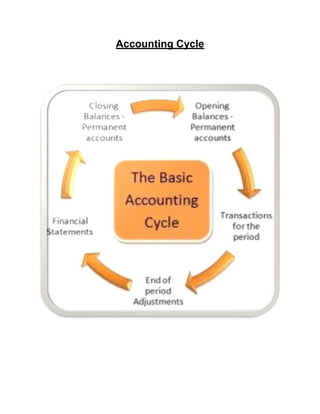

- 11. Accounting Cycle

- 13. General Journal Date Details Folio Debit Credit September 1 Bank CB01 364000 Cash CB01 27160 Debtor (J. Simpson) SL01 31600 Motor Van GL02 62840 Building GL03 100000 Stock 24960 Creditor (Super Supreme) PL01 10560 Capital GL01 600000 Opening entries 610560 610560 Purchase journal Page 01 Date Details Folio Amount 1-Sep Super Supreme International PL01 237,040 27-Sep Super Supreme International PL01 57,960 Sep 30 Total credit purchases to be transferred to the purchases account in the general ledger GL02 295,000 Page 01

- 14. SALES JOURNAL Date Details Folio Amount 5-Sep J. Simpson SL01 57000 13-Sep B. Banton SL03 78,550 20-Sep N. Kidman SL02 104,400 Sep 30 Total credit sales to be transferred to the sales account in the general ledger GL13 239,950 RETURN OUTWARDS JOURNAL Date Details Folio Amount 9-Sep Super Supreme International PL01 13,600 Sep 30 Total return outwards to be transferred to the return outwards account in the general ledger GL16 13,600 Return Inwards Day Book Date Details Folio Amount 24-Sep B. Banton SL03 16,800 30-Sep N. Kidman SL02 9,600 Sep 30 Total goods returned to us to be transferred to the return inwards account in the general ledger GL15 26,400

- 16. Cash Book Date Details Folio Discount Allowed Cash Bank Date Details Folio Discoun t Receive d Cash Bank Septembe r 1 Balance b/d GJ01 27,160 364,000 September 1 Machinery GL3 48,000 Septembe r 2 Bank C 50,000 2 Cash C 50,000 3 Sales GL1 3 59,350 3 Rent GL4 30,000 7 Sales GL1 3 37,750 6 Fixtures GL5 65,000 18 J. Simpson SJ01 12,000 45,000 8 Wages GL1 2 10,000 29 B. Banton SJ03 6,175 55,575 11 Insurance GL6 6,100 30 Sales GL1 3 120,540 11 Electricity GL7 3,300 11 Rates GL8 2,600 15 Super Supreme International PL01 7,500 142,500 15 Wages GL1 2 10,000 16 Drawings GL1 0 6,200 19 Furniture GL1 1 3,600 22 Wages GL1 2 10,000 29 Wages GL1 2 10,000 30 Balance c/d 123,075 239,000 18,175 350,375 409,000 7,500 350,375 409,000

- 18. General Ledger Date Details Folio Amount Date Details Folio Amount Capital A/C Page 01 September 31 Balance c/d 600,000 September 1 Balance b/d GJ01 600,000 October 1 Balance b/d 600,000 Motor Van A/C Page 02 September 1 Balance b/d GJ12 62,840 September 30 Balance c/d 62,840 October 1 Balance b/d 62,840 Buildings A/C Page 03 September 1 Balance b/d GJ01 100,000 September 30 Balance c/d 100,000 October 1 Balance b/d 100,000 Machinery A/C September 1 Bank CB01 48,000 September 31 Balance c/d 48,000 October 1 Balance b/d 48,000 Rent A/C September 3 Bank CB01 30,000 September 30 Profit & Loss 30,000 Page 4 Page 5

- 19. Fixtures A/C September 6 Cash CB01 65,000 September 31 Balance c/d 65,000 October 1 Bal b/d 65,000 Insurance A/C September 11 Bank CB01 6,100 September 30 Profit & Loss 6,100 Electricity A/C September 11 Bank CB01 3,300 September 30 Profit & Loss 5,500 30 Accruals c/d 1,200 5,500 5,500 October 1 Accruals b/d 1200 Rates September 11 Bank CB01 2,600 September 30 Profit & Loss 2,600 Drawings September 16 Cash CB01 6,200 September 30 Balance c/d 6,200 September 30 Balance b/d 6,200 Furniture September 19 Cash CB01 3,600 September 30 Balance c/d 3,600 October 1 Balance b/d 3,600 Page 10 Page 11 Page 6 Page 7 Page 8 Page 9

- 20. Wages September 8 Bank C01 10,000 September 31 Profit & Loss 40,000 15 Cash C01 10,000 22 Bank C01 10,000 29 Bank C01 10,000 40,000 40,000 Sales September 30 Trading Account 457,590 September 3 Cash CB01 59,350 September 7 Cash CB01 37,750 September 30 Cash CB01 120,540 September 30 Total Credit Sales SJ01 239,950 457,590 457,590 Purchases September 31 Total Credit Purchases PJ01 295,000 September 31 Trading Account 295,000 Return Inwards September 31 Total for month RI01 26,400 September 31 Trading Account 26,400 Return Outwards September 31 Trading Account RO01 13,600 September 31 Total for month 13,600 Page 15 Page 16 Page 14 Page 13 Page 12

- 21. Discount Allowed September 30 Total Discount Given to customers 18,175 September 30 P & L 18,175 Discount Received September 30 P & L 7,500 September 11 Super Supreme International 7,500 Purchases Ledger Super Supreme International September 9 Return Outwards RO01 13,600 September 1 Balance b/d GJ01 10,560 15 Bank CB01 142,500 1 Purchases PJ01 237,040 15 Discount Received CB01 7,500 27 Purchases PJ01 57,960 30 Balance c/d 141,960 305,560 305,560 October 1 Balance b/d 141,960 Sales Ledger J. Simpson September 1 Balance b/d 31,600 September 18 Discount Allowed CB01 12,000 September 5 Sales SJ01 57,000 September 18 Bank CB01 45000 September 30 Balance c/d 31,600 88,600 88,600 October 1 Balance b/d 31,600 Page 01 Page 01 Page 17 Page 18

- 22. N. Kidman September 20 Sales SJ01 104,400 September 30 Return Inwards RI01 9,600 September 30 Balance c/d 94,800 104,400 104,400 October 1 Balance b/d 94,800 B. Banton September 13 Sales SJ01 78,550 September 24 Return Inwards RI01 16,800 September 29 Discount Allowed CB01 6,175 29 Cash CB01 55,575 78,550 78,550 Page 03 Page 02

- 23. Trial Balance Blanna’s Fashion Boutique Trial Balance as at September 30, 2011 Details Debit $ Credit $ Capital 600,000 Motor Van Buildings 100,000 Machinery 48,000 Stock 24,960 Rent 30,000 Fixtures 65,000 Sales 457,590 Purchases 295,000 Cash 123,075 Bank 239,000 Wages 40,000 Return Outwards 13,600 Super Supreme International 141,960 Electricity 3,300 Insurance 6,100 Rates 2,600 Furniture 3,600 Drawings 6,200 Return Inwards 26,400 N. Kidman 94,800 J. Simpson 31,600 Discount Received 7,500 Discount Allowed 18,175 1,220,650 1,220,650

- 24. Stock Valuation (A) Pants Date Received Issued Balance Quantit y Unit Price Amount Quantit y Unit Price Amoun t Quantit y Unit Price Amount 1-Sep 12 900 10,800 1-Sep 96 1,000 96,000 12 96 900 1,000 10,800 96,000 3-Sep 12 12 900 1,000 10,800 12,000 84 1,000 84,000 5-Sep 12 1,000 12,000 72 1,000 72,000 13-Sep 24 1,000 24,000 48 1,000 48,000 20-Sep 24 1,000 24,000 24 1,000 24,000 27-Sep 36 1,100 39,600 24 36 1,000 1,100 24,000 39,600 30-Sep 24 12 1,000 1,100 24,000 13,200 24 1,100 26,400

- 25. (B) Blouse Date Received Issued Balance Quantity Unit Price Amount Quantity Unit Price Amount Quantity Unit Price Amount 1-Sep 12 400 4,800 1-Sep 96 440 42,240 12 96 400 440 4,800 42,240 5-Sep 12 12 400 440 4,800 5,280 84 440 36,960 13-Sep 24 440 10,560 60 440 26,400 20-Sep 36 440 15,840 24 440 10,560 30-Sep 12 440 5,280 12 440 5,280

- 26. (C ) Handbag Date Received Issued Balance Quantit y Unit Price Amount Quantit y Unit Price Amoun t Quantit y Unit Price Amount 1-Sep 4 1,600 6400 4 1,600 6,400 3-Sep 1 1,600 1,600 3 1,600 4,800 7-Sep 1 1,600 1,600 2 1,600 3,200 13-Sep 1 1,600 1,600 1 1,600 1,600 27-Sep 4 1,650 6,600 1 4 1,600 1,650 1,600 6,600 30-Sep 1 3 1,600 1,650 1,600 4,950 1 1,650 1,650

- 27. (D ) Skirts Date Received Issued Balance Quantity Unit Cost Amount Quantity Unit Cost Amount Quantit y Unit Cost Amount 1-Sep 12 780 9,360 1-Sep 60 820 49,200 12 60 780 820 9,360 49,200 3-Sep 12 780 9,360 60 820 49,200 7-Sep 12 820 9,840 48 820 39,360 13-Sep 12 820 9,840 36 820 29,520 30-Sep 24 820 19,680 12 820 9,840

- 28. (E) Slipper Date Received Issued Balance Quantity Unit Price Amount Quantity Unit Price Amount Quantity Unit Price Amoun t 1-Sep 48 900 43,200 48 900 43,200 5-Sep 12 900 10,800 36 900 32,400 7-Sep 12 900 10,800 24 900 21,600 20-Sep 24 900 21,600 27-Sep 12 980 11,760 12 980 11,760

- 29. Trading, Profit and Loss and Appropriation Account Blanna’s Fashion Boutique Trading Profit & Loss Account for the year ended September 30, 2011 $ $ $ Sales 457,590 Less Return Inwards (26,400) Net Sales 431,190 Less Cost of Goods Sold: Opening Stock 24,960 Purchases 95,000 Less Return Outwards (13,600) Net Purchases 281,400 Cost of Goods Available 306,360 Less Closing Stock (54,930) 251,430 Gross Profit 179,760 Add Revenues Discount Received 7,500 187,260 Less Expenses Wages 40,000 Rent 30,000 Electricity 4,500 Insurance 5,100 Rates 2,600 Depreciation 400 Discount Allowed 18,175 100,775 86,485 Net Profit Add interest on Drawings: Shadae 620 Less: 85,865 Interest on capital Anna kay 12,500 Shadae 7500 Ovasha 10,000 30,000 Salary: Anna kay 12,000 42,000

- 30. 43,865 Share of Profit: Anna kay 18,277.08 Shadae 10966.25 Ovasha 14,621.67 43,865

- 31. Balance Sheet Blanna’s Fashion Boutique Balance Sheet as at September 30, 2011 Fixed Assets Cost Accumulated Depreciation NBV Buildings 100000 100,000 Fixtures 65000 65,000 Machinery 48000 400 47,600 Furniture 3600 3,600 Motor Car 62840 62,840 400 279,040 Current Assets Stock 54,930 Debtors 126,400 Prepayment 1,000 Bank 239,000 Cash 123,075 544,405 Less Current Liabilities Creditors 141960 Accruals 1,200 143160 Working Capital 401,245 680,285 Financed by: Capital 600,000 Net Profit 86,485 686,485 Less Drawings 6,200 680,285

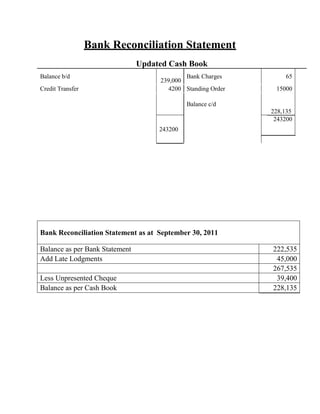

- 32. Bank Reconciliation Statement Updated Cash Book Balance b/d 239,000 Bank Charges 65 Credit Transfer 4200 Standing Order 15000 Balance c/d 228,135 243200 243200 Bank Reconciliation Statement as at September 30, 2011 Balance as per Bank Statement 222,535 Add Late Lodgments 45,000 267,535 Less Unpresented Cheque 39,400 Balance as per Cash Book 228,135

- 33. Accounting Ratios ÔÉò Inventory Turnover Ratio- Cost of Goods sold Average Inventory/2 =244,470 24960+61890/2 =5.62 ÔÉò Current Ratio- Current assets Current Liabilities =551365 143160 =3.85 ÔÉò Gross profit as a percentage of sales- Gross profit x 100 Sales =179,760 x 100 457590 = 39.28% For every sale of $100 the business earns $39.28 as gross profit. ÔÉò Net profit Ratio- Net profit / Net sales x l00 =86,485 / 431,190 x 100 =20.06% For every sale of $100 the business earns $20.06 as net profit.

- 34. ÔÉò Acid Test Ratio- Current Assets- Stock Current liabilities = 544,405 - 54,930 143160 =3.42

- 35. Performance of the Business In preparing the financial statements of Blanna’s Fashion Boutique the Trading, profit and loss and appropriation account shows a profit of eighty six thousand four hundred and eighty five thousand dollar (86,485) at the end of the financial period of September 30,2011. The business started out with six hundred thousand dollar. In the closing of the financial period of Blanna’s Fashion Boutique there was an increase in the amount of capital that the business has. The business made a gross profit of one hundred and seventy nine seven hundred and sixty dollars (179,760) instead of making a gross loss.

- 36. Comparisons The comparison is being done between the opening capital and the closing capital for Blanna’s Fashion Boutique, at the end of the financial period. At the beginning of the financial year the opening capital was six hundred thousand dollar (600,000). At the end of the financial period the closing capital is six hundred and eighty thousand two hundred and eighty five dollar (680,285) which means there is an increase of eighty thousand two hundred and eighty five dollar (80,285). Another comparison is being done between the fixed assets of the business and the current assets. The fixed asset of the business is two hundred and seventy nine thousand and forty dollar (279,040) while the current asset is five hundred and forty four thousand four hundred and five dollars (544,405). This means that the amount of money that the business spend of items that stays in the business with no intention of selling it is lesser than the amount of money that the business spend on assets that will allow the business to generate a profit.

- 37. Recommendations and Suggestions It is recommended that Blanna’s Fashion Boutique:  Ploughed back a portion of the profit that the business makes into it.  Introduces new products to the business.  Purchase new equipment for the business  Uses some of the profit that the business makes to attach another department on to the business. It is suggested that Blanna’s Fashion Boutique should:  Purchase cheaper equipments to use in the business. This will increase the amount of money available in the business.  Offer more sale discounts this will force more customers to purchase from Blanna’s Fashion Boutique.

- 38. Conclusion It is clear that Blanna’s Fashion Boutique keeps all the records of the transactions that take place in the business over the financial period of time. Blanna’s Fashion Boutique could increase the gross profit and net profit of the business by adhering to the suggestions or recommendations outlined. Never the less Blanna’s Fashion Boutique made a good net profit of eighty six thousand four hundred and eighty five dollars (86,485) during the month of September in 2011. Blanna’s Fashion Boutique was able to make a profit due to the large amount of sales the business made.

- 40. Price list Goods Price Pants $ Blouse $ Handbags $ Skirts $ Slippers $

- 41. INVOICE Blanna’s Fashion Boutique Invoice No. 001 Date: From: To: Quantity Description Unit price $

- 42. Debit note

- 45. Principles of Accounts School Based Assessment (2012-2013) You are required to name the firm and state the nature of the business. This must be in accordance with the items sold*. After the initial accounting entries (Tasks 1 -3) have been completed you will then record the additional adjusting entries as set out at Tasks 4 and 5. You may choose goods from the following list for the transactions. * Computer Store Clothes and Accessories Store A Keyboard Pants (guess) B Mouse Blouse (guess) C Printer Hand bags (guess)

- 46. D Surge Protector Skirts (guess) E Speakers Slippers (guess) ABC Enterprise (Remember that you are to rename the firm) The following transactions were taken from the books of ABC Enterprise. You are required to asses them carefully then write up the relevant books as outlined in the requirements below: 2011 Sept 1 Opening Balances Capital $600, 000 Bank $364, 000 Cash $ 27, 160 Debtor (J Simpson) $ 31, 600 Creditor (Super Supreme International) $ 10, 560 Motor Van $ 62, 840 Building $100, 000 Stock 1doz A $ 10,800 1doz B $ 4,800

- 47. 1doz D $ 9,360 Sept 1 Bought goods on credit from Super Supreme International. 8 doz A @ $1,000 each 8 doz B @ $440 each 4 boxes C @ $1,600 each 5 doz D @ $820 each 4 doz E @ $900 each Sept 1 Bought Machinery by cheque $48, 000. Sept 2 Withdrew $50, 000 cash from the bank account to be used in the business. Sept 3 Cash Sales 2 doz A @ $1, 650 each 1 box C @ $2, 950 each 1 doz D @ $1, 400 each Sept 3 Paid rent by cheque $30, 000. Sept 5 sold goods on credit to J. Simpson. 1 doz A @ $1, 650 each 2 doz B @ $800 each 1 doz E @ $1, 500 each Sept 6 Bought fixtures with cash $65, 000. Sept 7 Cash Sales

- 48. 1 box C @ $2, 950 each 1 doz D @ $1, 400 each 1 doz E @ $1, 500 each Sept 8 Paid wages $10, 000 by cheque. Sept 9 Returned goods to Super Supreme International as items were damaged. 1 doz A 1 box C Sept 11 Paid the following expenses by cheque: Insurance $6,100, Electricity $3,300 and Rates $2,600. Sept 13 Sold goods on credit to B. Banton: 2 doz A @ $1, 650 each 2 doz B @ $ 800 each 1 box C @ $2, 950 each 1 doz D @ $1, 400 each Sept 15 Made payment to Super Supreme International by cash $150, 000, received a 5% cash discount. Sept 15 Paid wages with cash $10, 000 Sept 16 Owner withdrew $6,200 cash to fix his personal motor car. Sept 18 Collected Cheque from J. Simpson for goods sold on Sept 5th 2011, $45, 000. Sept 19 Bought furniture $3,600 with cash from Courts Ja. Ltd.

- 49. Sept 20 Sold goods on credit to N. Kidman 2 doz A @ $1, 650 each 3 doz B @ $ 800 each 2 doz E @ $1, 500 each Sept 22 Paid wages with cheque $10, 000. Sept 24 1 doz D returned to us by B. Banton as they were the wrong size. Sept 27 Bought goods on credit from Super Supreme International. 3 doz A @ $ 1,100 each 4 boxes C @ $1, 650 each 1 doz E @ $ 980 each Sept 29 B. Banton settled his account less 10% cash discount. He paid with cash. Sept 29 Paid wages $10,000 by cheque. Sept 30 Received goods from N. Kidman: 1 doz B Sept 30 Cash Sales 3 doz A @ $1, 815 each 1 doz B @ $ 800 each 4 boxes C @ $3, 000 each 2 doz D @ $1, 400 each

- 50. Task 1 Write up ALL Subsidiary Books and then post the transactions to the ledgers. Please ensure that you distinguish between, General Ledger, Sales Ledger and Purchases Ledger. Show the opening entries in the General Journal at September 1, 2011. Task 2 Prepare ABC Enterprise Trial Balance as at September 30, 2011 Task 3 Using the FIFO method of stock valuation, determine the closing stock. Task 4 Design a logo and slogan for your business and provide the relevant information on the business entity Prepare ABC Enterprise Trading, Profit and Loss Account for the month ending September 30, 2011 and a Balance Sheet as at that date, after taking into account the following: a) Insurance expense was paid in advance, $1000. b) Electricity was outstanding by $1, 200 c) Machinery is to be depreciated at 10 % annually using the straight line method (show the depreciation for the month). Show adjustment to the above information in the ledgers. Task 5 Prepare the Bank Reconciliation Statement using the Bank Statement below

- 51. Bank Statement DR CR Balance $ $ $ Sept 1 Balance 364 000 Sept 1 Burke’s (Machinery) 48 000 316 000 Sept 2 SNPN Ltd (Cash) 50 000 266 000 Sept 8 Wages 10 000 256 000 Sept 11 NWC (Rates) 2 600 253 400 Sept 20 Wages 10 000 243 400 Sept 24 Credit transfer (Q Smith) 4 200 247 600 Sept 29 Wages 10 000 237 600 Sept 29 Standing Order 15 000 222 600 Sept 29 Bank Charges 65 222 535 Task 6 Prepare cheques, invoices, cash receipts, debit and credit notes (Appendices). Task 7 Analyse the results of the operations of ABC Enterprise over the relevant period. In your analysis you should highlight strengths/weaknesses and comment on ways in which the efficiency of the firm may be improved. Accounting Ratios, graphs, tables, charts and diagrams are tools that when used will strengthen/enhance you analysis and presentation. Comparisons may be made between the results of ABC Enterprise and those of the industry.

- 52. Task 8 Complete S.B.A. making reference to the due dates. Due Dates: Subsidiary Books - June 12th 2012 Trial Balance and Stock Valuation - September 29th 2012 Trading, Profit and Loss and Balance Sheet - September 29th 2012 Bank Recon. Statement - October 16th 2012 First Draft (completed) - November 17th 2012 Final Draft (completed)- December12th 2012