Process Level Auditing 2012

0 likes578 views

Process Level Auditing (PLA) involves auditors facilitating managers to assess control strengths and weaknesses within related business activities. The auditor and managers work together to develop improvement plans where needed. With PLA, all existing controls are reviewed by managers and auditors to determine how to improve efficiency. The internal audit acts as a consultant to enhance department operations. PLA improves the organization by incorporating manager operational knowledge, assessing processes as continuous flows, helping managers understand impact across activities, and applying controls for maximum efficiency and effectiveness.

1 of 8

Downloaded 11 times

Ad

Recommended

Control Self Assessment

Control Self AssessmentManoj Agarwal

╠²

The document provides an overview of control self-assessment (CSA). It discusses what CSA is, its goals and benefits, how it is implemented through workshops, and how the results are reported. CSA involves employees assessing risks, controls and weaknesses within their process. Workshops are facilitated to have open discussions, develop recommendations and action plans. The results are anonymously reported to management to address issues.Presentation_20110802213554

Presentation_20110802213554P Karlin Panggalo.SE.MM.Ak.CA.CFA.CCM

╠²

This document provides an overview of operational risk management frameworks and control self-assessment processes. It defines risk management and outlines common risk management frameworks. It then describes a control self-assessment framework that includes setting objectives, assessing risks and controls, analyzing results, and monitoring risks on an ongoing basis. The framework is intended to help managers assess risks and controls in a transparent way and provide regular reporting to senior management.Improve Regulatory Compliance & Risk Management Using Best Practices

Improve Regulatory Compliance & Risk Management Using Best PracticesLavante Inc.

╠²

The document outlines a 2015 webinar focused on improving regulatory compliance and risk management in supplier management through best practices. Key topics include communication gaps, data collection, third-party integration, and effective reporting, as well as specific best practices for managing supplier relationships and automating compliance tasks. The emphasis is on treating supplier management as an ongoing process rather than a one-time project, highlighting the need for automation and effective risk mitigation strategies.PAWS - Pentana Audit Work System software

PAWS - Pentana Audit Work System softwareMantala

╠²

The document discusses PAWS Pentana Audit Work System software and its benefits for risk managers, internal auditors, and other assurance providers. It provides an overview of what these roles do and their reasons for wanting audit management software. Key benefits include automating processes, enabling off-site review, reusing previous work, and coordinating assurance activities across departments to reduce duplication.Managing Regulatory Compliance

Managing Regulatory ComplianceMitchell Manning Sr.

╠²

The document discusses regulatory compliance and the responsibilities for ensuring compliance at all levels of an organization. It states that leadership is responsible and accountable for compliance performance. It also notes that compliance consultants can help organizations by simplifying, eliminating waste from, and accelerating compliance efforts. The document emphasizes that compliance is a performance requirement for the entire organization from executive leadership down to individual employee job functions and tasks.Performance management audit

Performance management auditnickytamo

╠²

This document outlines key aspects for an effective performance management audit. It discusses the importance of internal audit aligning with and focusing on an organization's strategic objectives and risks. It also emphasizes the need for internal audit to continuously improve itself and promote improvement across the organization. Additionally, it notes the importance of internal audit managing relationships effectively and considering value for money in its work to help an organization achieve its strategic goals.Role of internal audit

Role of internal auditMyron Duncan Burton Betshanger

╠²

Internal auditors are responsible for evaluating controls, assessing risks, analyzing operations, and reviewing compliance. They work as an independent advisor to challenge current practices and champion best practices. Their goal is to ensure the organization can achieve its strategic objectives. In contrast, external auditors have a statutory obligation to shareholders and focus on finances and accounting, while internal auditors have a broader scope and focus on the entire organization, departments, functions, and operations.Audit ratings

Audit ratingsKatty Dhankar

╠²

A rating of "satisfactory" means internal controls, governance and risk management are adequately established and functioning well with no significant issues found. A rating of "partially satisfactory" means these processes are generally established and functioning but need some improvement, with one or more issues found. A rating of "unsatisfactory" means these processes are either not established or not functioning well, with significant issues found that require urgent priority to address.Effective control system

Effective control systemAbhi Bhatt

╠²

The document outlines an effective control system (ECS) presentation divided into several sections. It begins with introductions by various presenters and describes the basic steps of establishing standards, measuring performance, comparing to standards, and taking corrective actions. It then discusses designing an integrated strategic and control system that identifies strategic control points. Later sections cover types of control systems, advantages and disadvantages, control areas within an organization, essential elements, and importance of an ECS for making plans effective, ensuring consistency, aiding decision making and providing feedback.The System and Process of Controlling

The System and Process of ControllingMahamid Rahman

╠²

The document discusses various aspects of controlling in management. It begins by defining controlling as the process of monitoring, comparing, and correcting work performance. It then describes the importance of controlling and outlines the typical control process, which involves setting standards, measuring actual performance, comparing to standards, and responding to deviations. The document also discusses different types of control systems like bureaucratic control and clan control. Finally, it notes some key requirements for effective controls, such as tailoring controls to plans/positions and individuals, designing controls to point up exceptions, and ensuring flexibility and quick corrective action.Control self assessment (csa)

Control self assessment (csa)Idear S. Wanichkul

╠²

Control Self-Assessment (CSA) allows managers and employees to directly assess an organization's risk management and internal controls. CSA helps clarify business objectives, identify risks to achieving objectives, and ensure controls and regulations are followed. The CSA process involves employees self-evaluating controls and processes through activities like risk identification, control assessment, and action planning. Benefits of CSA include improved understanding and responsibility for controls, more effective corrective actions, and increased awareness of objectives. However, CSA may face resistance to change and requires open and honest participation to provide accurate results.Performance Audit

Performance Auditmounika ramachandruni

╠²

A performance audit examines the effectiveness, economy, and efficiency of a government program or agency. It assesses if resources are being managed properly and accountability requirements are met. A performance audit reviews employee performance against goals, measures efficiency, effectiveness, and economy, and identifies what is and is not working. The process involves project selection, planning, conducting the audit, reporting findings, and follow up to ensure recommendations are implemented.Practical approach to Risk Based Internal Audit

Practical approach to Risk Based Internal AuditManoj Agarwal

╠²

The document provides an overview of risk based internal auditing. It discusses key concepts like the definition of risk, COSO ERM framework, three lines of defense model, definition of internal audit, and risk based internal audit approach. The approach involves identifying the audit universe and processes, risk identification and assessment, risk scoring and heat mapping, developing the risk based internal audit plan, and executing the plan. Various tools for risk based auditing like the audit tracker, audit report templates, and resources are also outlined.Man101 Chapter13

Man101 Chapter13JonathanHindi

╠²

Control involves monitoring activities to ensure they are accomplished as planned and correcting deviations to attain organizational goals. The control process includes measuring performance, comparing to standards, and taking action to correct deviations. There are different types of control including feedforward, concurrent, and feedback control. An effective control system has qualities like accuracy, timeliness, flexibility, and reasonable criteria. Contingency factors like organization size and culture affect control system design.Model i best practice evaluation worksheet for ia

Model i best practice evaluation worksheet for iaRajeswaran Muthu Venkatachalam

╠²

The document outlines best practices for internal audit departments across five key areas: roles and structure, people, process, technology, and knowledge. It provides examples of best practice features for each area and a template for departments to evaluate the evidence of these features in their own practices. The template can be used to assess areas as low, medium, or high and identify opportunities for improvement. The document aims to help internal audit departments evaluate their practices against industry standards and enhance their ability to add value through continuous improvement.Governance, Risk, and Control Knowledge Elements

Governance, Risk, and Control Knowledge ElementsIyad Mourtada, CMA, CIA, CFE, CCSA, CRMA, CPLP

╠²

This document discusses key concepts in governance, risk management, and internal controls including:

- The role of internal auditing in evaluating risk management and governance processes

- Components of enterprise risk management and the COSO framework

- Types of internal controls and the responsibility of management and auditors

- Governance structures and the role of internal auditing in ensuring effective governanceControl

ControlProf. Chhaya Sachin Patel

╠²

1. The document discusses the concept of control in management and outlines its nature, importance, relationship to planning, types, resistance to control, and effective control systems.

2. It describes control as a process that minimizes deviations from goals and standards through setting performance measures and correcting deviations.

3. Effective control systems focus on critical areas, operate at multiple levels of the organization, and concentrate on exceptions rather than all activities.Turning risk into opportunities

Turning risk into opportunitiesManoj Agarwal

╠²

The presentation discusses the concept of risk as a mix of danger and opportunity, emphasizing that effective risk management is crucial for navigating uncertainties and achieving sustainable growth. It provides various examples of how companies can turn potential risks, such as supply chain issues and compliance liabilities, into opportunities for cost savings, market share preservation, and knowledge retention. Additionally, it highlights the importance of innovation and proactive strategies in overcoming challenges and transforming risks into competitive advantages.COSO Framework Model

COSO Framework ModelTownofAddison

╠²

The document outlines the control environment and risk assessment framework adopted by the Town of Addison, detailing how it identifies, analyzes, and manages risks to achieve organizational objectives. It emphasizes governance oversight, communication, continuous monitoring, and various planned actions to enhance internal controls, financial management, and compliance with audit standards. The framework is structured around the COSO model and includes specific initiatives for training, policies, and evaluations to ensure effective risk management practices.The nature and significance of control

The nature and significance of controlPranav Kumar Ojha

╠²

The document discusses different aspects of control as a management function. It defines control as verifying performance against plans and standards to identify errors and ensure objectives are met. Control involves measuring performance, comparing it to standards, and taking actions to correct deviations. It discusses different control techniques like personal observation, reports, and adjusting standards or employee performance to bring results in line with goals. The key aspects of an effective control system are outlined.Chapter 10 controlling

Chapter 10 controllingArgon David

╠²

The document defines control as the measurement and correction of subordinate performance to ensure organizational objectives are achieved. It discusses the elements, essentials, functions, techniques, benefits, and limitations of control, including budgetary and non-budgetary controls. Key aspects of an effective control system include suitability, prompt reporting, flexibility, focusing on strategic points, and facilitating remedial action.POSITION OF INTERNAL AUDIT IN THE CORPORATE FRAMEWORK

POSITION OF INTERNAL AUDIT IN THE CORPORATE FRAMEWORKHaresh Lalwani

╠²

The document discusses the evolving role of internal audit within corporate governance frameworks, highlighting its importance in risk management and decision-making processes. It emphasizes the shift from compliance-focused audits to a strategic, risk-based approach that adds value to organizations by leveraging technology and adapting to a changing business environment. Key themes include the necessity for internal audit to identify emerging risks, support organizational goals, and provide critical insights to enhance operational effectiveness.Business continuity - 5 key steps to effective business impact analysis

Business continuity - 5 key steps to effective business impact analysismoranjustin

╠²

This document discusses the importance of business impact analysis for developing an effective business continuity and IT disaster recovery plan. It outlines that RCU engagements in 2014 found incomplete BCPs and lack of testing. Failure to have a formal BCP can disrupt member services, make business-critical information unavailable, and result in insufficient IT system resilience. The document then provides the top 5 key steps to conducting a business impact analysis to properly prioritize processes, identify resource dependencies, determine acceptable downtimes, prioritize restoration, and inform recovery strategies. It also includes a sample classification system to categorize systems as critical, vital, sensitive, or non-critical.Functional Audit

Functional AuditManoj Agarwal

╠²

A functional audit verifies that the functions within an organization or business process are meeting requirements. The presentation discusses functional audits, provides examples of what could be audited (e.g. a payroll function), and defines a functional audit as verifying requirements are met. The presentation also includes four case studies that provide examples of issues a functional auditor may find, such as duplicate records, unused features, and logic flaws. The recap emphasizes getting full value from systems by ensuring functionality meets business needs.Principles of management ŌĆō mgt101

Principles of management ŌĆō mgt101Fallahchay Ali

╠²

The document outlines principles of management, focusing on the controlling process which includes establishing standards, measuring performance, and correcting deviations. It discusses various control mechanisms like feedback and feed-forward systems, as well as benchmarking for goal setting. Additionally, it highlights the importance of operations management, encompassing production design, layout, and information systems in enhancing efficiency and effectiveness.Management Control System

Management Control SystemDrishay Gupta

╠²

The document discusses management control systems (MCS), defining them as a set of formal and informal mechanisms for resource management to achieve organizational goals. It outlines various types of controls, including formal and informal systems, and explains their applications through traditional and modern techniques such as budgeting, observation, and management audits. Additionally, it highlights the importance of MCS within different levels of management to ensure efficient utilization of resources and alignment with organizational objectives.Managerial control

Managerial controlParul Tandan

╠²

Control systems are used to ensure activities achieve desired results. They involve setting targets, measuring performance, and making corrections. Effective control requires trust in people and an assumption of ethical behavior. Control can happen at different levels within an organization between controllers and those they control. Control aims to avoid surprises and ensure accountability. Both facilitative and protective controls are important, with the former focusing on communication and the latter on authorization, segregation of duties, and safeguarding of assets.8 moves to becoming an agile internal audit

8 moves to becoming an agile internal auditSALIH AHMED ISLAM

╠²

Transitioning to an agile auditing methodology over time can help effectively manage change and gain support. Starting small with key agile concepts like shorter planning horizons and more frequent communication allows flexibility to focus on effective approaches. Gaining executive and board support is also critical by discussing goals and changes to expect in reporting and collaboration. An agile approach simplifies risk assessment by focusing on the most significant risks and opportunities through collaboration with management.Process Level Auditing Presentation

Process Level Auditing PresentationVernon Benjamin

╠²

Process level auditing involves auditors facilitating managers' assessment of control strengths and weaknesses across related activities. The auditors and managers work together to develop improvement plans where needed. Under this approach, all existing controls are reviewed by managers and auditors to determine how efficiency can be improved. The auditors act as consultants to help enhance department operations.Management audit

Management auditPrashantu mer

╠²

This document provides an overview of a management audit assignment submitted by a student. It defines management audit as an independent evaluation of a company's overall performance to assess efficiency and identify areas for improvement. The document outlines the objectives, scope, qualifications of auditors, techniques used, and components of a management audit report. It also compares management audits to financial audits.More Related Content

What's hot (20)

Effective control system

Effective control systemAbhi Bhatt

╠²

The document outlines an effective control system (ECS) presentation divided into several sections. It begins with introductions by various presenters and describes the basic steps of establishing standards, measuring performance, comparing to standards, and taking corrective actions. It then discusses designing an integrated strategic and control system that identifies strategic control points. Later sections cover types of control systems, advantages and disadvantages, control areas within an organization, essential elements, and importance of an ECS for making plans effective, ensuring consistency, aiding decision making and providing feedback.The System and Process of Controlling

The System and Process of ControllingMahamid Rahman

╠²

The document discusses various aspects of controlling in management. It begins by defining controlling as the process of monitoring, comparing, and correcting work performance. It then describes the importance of controlling and outlines the typical control process, which involves setting standards, measuring actual performance, comparing to standards, and responding to deviations. The document also discusses different types of control systems like bureaucratic control and clan control. Finally, it notes some key requirements for effective controls, such as tailoring controls to plans/positions and individuals, designing controls to point up exceptions, and ensuring flexibility and quick corrective action.Control self assessment (csa)

Control self assessment (csa)Idear S. Wanichkul

╠²

Control Self-Assessment (CSA) allows managers and employees to directly assess an organization's risk management and internal controls. CSA helps clarify business objectives, identify risks to achieving objectives, and ensure controls and regulations are followed. The CSA process involves employees self-evaluating controls and processes through activities like risk identification, control assessment, and action planning. Benefits of CSA include improved understanding and responsibility for controls, more effective corrective actions, and increased awareness of objectives. However, CSA may face resistance to change and requires open and honest participation to provide accurate results.Performance Audit

Performance Auditmounika ramachandruni

╠²

A performance audit examines the effectiveness, economy, and efficiency of a government program or agency. It assesses if resources are being managed properly and accountability requirements are met. A performance audit reviews employee performance against goals, measures efficiency, effectiveness, and economy, and identifies what is and is not working. The process involves project selection, planning, conducting the audit, reporting findings, and follow up to ensure recommendations are implemented.Practical approach to Risk Based Internal Audit

Practical approach to Risk Based Internal AuditManoj Agarwal

╠²

The document provides an overview of risk based internal auditing. It discusses key concepts like the definition of risk, COSO ERM framework, three lines of defense model, definition of internal audit, and risk based internal audit approach. The approach involves identifying the audit universe and processes, risk identification and assessment, risk scoring and heat mapping, developing the risk based internal audit plan, and executing the plan. Various tools for risk based auditing like the audit tracker, audit report templates, and resources are also outlined.Man101 Chapter13

Man101 Chapter13JonathanHindi

╠²

Control involves monitoring activities to ensure they are accomplished as planned and correcting deviations to attain organizational goals. The control process includes measuring performance, comparing to standards, and taking action to correct deviations. There are different types of control including feedforward, concurrent, and feedback control. An effective control system has qualities like accuracy, timeliness, flexibility, and reasonable criteria. Contingency factors like organization size and culture affect control system design.Model i best practice evaluation worksheet for ia

Model i best practice evaluation worksheet for iaRajeswaran Muthu Venkatachalam

╠²

The document outlines best practices for internal audit departments across five key areas: roles and structure, people, process, technology, and knowledge. It provides examples of best practice features for each area and a template for departments to evaluate the evidence of these features in their own practices. The template can be used to assess areas as low, medium, or high and identify opportunities for improvement. The document aims to help internal audit departments evaluate their practices against industry standards and enhance their ability to add value through continuous improvement.Governance, Risk, and Control Knowledge Elements

Governance, Risk, and Control Knowledge ElementsIyad Mourtada, CMA, CIA, CFE, CCSA, CRMA, CPLP

╠²

This document discusses key concepts in governance, risk management, and internal controls including:

- The role of internal auditing in evaluating risk management and governance processes

- Components of enterprise risk management and the COSO framework

- Types of internal controls and the responsibility of management and auditors

- Governance structures and the role of internal auditing in ensuring effective governanceControl

ControlProf. Chhaya Sachin Patel

╠²

1. The document discusses the concept of control in management and outlines its nature, importance, relationship to planning, types, resistance to control, and effective control systems.

2. It describes control as a process that minimizes deviations from goals and standards through setting performance measures and correcting deviations.

3. Effective control systems focus on critical areas, operate at multiple levels of the organization, and concentrate on exceptions rather than all activities.Turning risk into opportunities

Turning risk into opportunitiesManoj Agarwal

╠²

The presentation discusses the concept of risk as a mix of danger and opportunity, emphasizing that effective risk management is crucial for navigating uncertainties and achieving sustainable growth. It provides various examples of how companies can turn potential risks, such as supply chain issues and compliance liabilities, into opportunities for cost savings, market share preservation, and knowledge retention. Additionally, it highlights the importance of innovation and proactive strategies in overcoming challenges and transforming risks into competitive advantages.COSO Framework Model

COSO Framework ModelTownofAddison

╠²

The document outlines the control environment and risk assessment framework adopted by the Town of Addison, detailing how it identifies, analyzes, and manages risks to achieve organizational objectives. It emphasizes governance oversight, communication, continuous monitoring, and various planned actions to enhance internal controls, financial management, and compliance with audit standards. The framework is structured around the COSO model and includes specific initiatives for training, policies, and evaluations to ensure effective risk management practices.The nature and significance of control

The nature and significance of controlPranav Kumar Ojha

╠²

The document discusses different aspects of control as a management function. It defines control as verifying performance against plans and standards to identify errors and ensure objectives are met. Control involves measuring performance, comparing it to standards, and taking actions to correct deviations. It discusses different control techniques like personal observation, reports, and adjusting standards or employee performance to bring results in line with goals. The key aspects of an effective control system are outlined.Chapter 10 controlling

Chapter 10 controllingArgon David

╠²

The document defines control as the measurement and correction of subordinate performance to ensure organizational objectives are achieved. It discusses the elements, essentials, functions, techniques, benefits, and limitations of control, including budgetary and non-budgetary controls. Key aspects of an effective control system include suitability, prompt reporting, flexibility, focusing on strategic points, and facilitating remedial action.POSITION OF INTERNAL AUDIT IN THE CORPORATE FRAMEWORK

POSITION OF INTERNAL AUDIT IN THE CORPORATE FRAMEWORKHaresh Lalwani

╠²

The document discusses the evolving role of internal audit within corporate governance frameworks, highlighting its importance in risk management and decision-making processes. It emphasizes the shift from compliance-focused audits to a strategic, risk-based approach that adds value to organizations by leveraging technology and adapting to a changing business environment. Key themes include the necessity for internal audit to identify emerging risks, support organizational goals, and provide critical insights to enhance operational effectiveness.Business continuity - 5 key steps to effective business impact analysis

Business continuity - 5 key steps to effective business impact analysismoranjustin

╠²

This document discusses the importance of business impact analysis for developing an effective business continuity and IT disaster recovery plan. It outlines that RCU engagements in 2014 found incomplete BCPs and lack of testing. Failure to have a formal BCP can disrupt member services, make business-critical information unavailable, and result in insufficient IT system resilience. The document then provides the top 5 key steps to conducting a business impact analysis to properly prioritize processes, identify resource dependencies, determine acceptable downtimes, prioritize restoration, and inform recovery strategies. It also includes a sample classification system to categorize systems as critical, vital, sensitive, or non-critical.Functional Audit

Functional AuditManoj Agarwal

╠²

A functional audit verifies that the functions within an organization or business process are meeting requirements. The presentation discusses functional audits, provides examples of what could be audited (e.g. a payroll function), and defines a functional audit as verifying requirements are met. The presentation also includes four case studies that provide examples of issues a functional auditor may find, such as duplicate records, unused features, and logic flaws. The recap emphasizes getting full value from systems by ensuring functionality meets business needs.Principles of management ŌĆō mgt101

Principles of management ŌĆō mgt101Fallahchay Ali

╠²

The document outlines principles of management, focusing on the controlling process which includes establishing standards, measuring performance, and correcting deviations. It discusses various control mechanisms like feedback and feed-forward systems, as well as benchmarking for goal setting. Additionally, it highlights the importance of operations management, encompassing production design, layout, and information systems in enhancing efficiency and effectiveness.Management Control System

Management Control SystemDrishay Gupta

╠²

The document discusses management control systems (MCS), defining them as a set of formal and informal mechanisms for resource management to achieve organizational goals. It outlines various types of controls, including formal and informal systems, and explains their applications through traditional and modern techniques such as budgeting, observation, and management audits. Additionally, it highlights the importance of MCS within different levels of management to ensure efficient utilization of resources and alignment with organizational objectives.Managerial control

Managerial controlParul Tandan

╠²

Control systems are used to ensure activities achieve desired results. They involve setting targets, measuring performance, and making corrections. Effective control requires trust in people and an assumption of ethical behavior. Control can happen at different levels within an organization between controllers and those they control. Control aims to avoid surprises and ensure accountability. Both facilitative and protective controls are important, with the former focusing on communication and the latter on authorization, segregation of duties, and safeguarding of assets.8 moves to becoming an agile internal audit

8 moves to becoming an agile internal auditSALIH AHMED ISLAM

╠²

Transitioning to an agile auditing methodology over time can help effectively manage change and gain support. Starting small with key agile concepts like shorter planning horizons and more frequent communication allows flexibility to focus on effective approaches. Gaining executive and board support is also critical by discussing goals and changes to expect in reporting and collaboration. An agile approach simplifies risk assessment by focusing on the most significant risks and opportunities through collaboration with management.Similar to Process Level Auditing 2012 (20)

Process Level Auditing Presentation

Process Level Auditing PresentationVernon Benjamin

╠²

Process level auditing involves auditors facilitating managers' assessment of control strengths and weaknesses across related activities. The auditors and managers work together to develop improvement plans where needed. Under this approach, all existing controls are reviewed by managers and auditors to determine how efficiency can be improved. The auditors act as consultants to help enhance department operations.Management audit

Management auditPrashantu mer

╠²

This document provides an overview of a management audit assignment submitted by a student. It defines management audit as an independent evaluation of a company's overall performance to assess efficiency and identify areas for improvement. The document outlines the objectives, scope, qualifications of auditors, techniques used, and components of a management audit report. It also compares management audits to financial audits.Risk Assessment Framework

Risk Assessment FrameworkJhurt7103

╠²

The document proposes an integrated risk assessment process that is robust, transparent, and based on COSO and Six Sigma frameworks. It involves using a Risk and Frequency Matrix to assess risks at the process level and validate resource allocation. A Risk Profile Analysis further examines inherent, business, and technology risks. Control assessments are also made. Cause and Effect Matrices are used to link key risks to process functions. Failure Mode and Effects Analyses identify potential process weaknesses. Preventive and detective controls are categorized by type and sub-type. The process aims to identify, prioritize, and reduce risks across the organization.Risk Assessment For Internal Auditors

Risk Assessment For Internal Auditorsminkhollow

╠²

This document discusses risk assessments and their importance for audit planning. It provides definitions for risk and risk assessment, and explains how risk assessments allow entities to understand potential impacts on objectives. Risk assessments employ both qualitative and quantitative methods, relate risks to time horizons and objectives, and assess inherent and residual risks. The document also discusses how internal auditors can add value through risk-based audit planning and evaluating management's risk assessments and controls. Key components of risk assessments are outlined.Evaluation and control in strategic management

Evaluation and control in strategic managementMeenakshi1994

╠²

The document discusses strategic evaluation and control in businesses. Strategic evaluation allows companies to assess their health, productivity, and future plans beyond short-term factors. It is performed by various stakeholders to test strategy effectiveness, set objectives, and determine if the organization is moving in the right direction. Strategic control monitors strategies adopted by the organization to ensure alignment with internal and external environments. It involves determining what to control, setting standards, measuring performance, comparing to standards, identifying deviations, and taking corrective action.Spire Brief - Risk Consulting

Spire Brief - Risk ConsultingPrashant Jain

╠²

The document provides information about Spire Advisors Pvt Ltd, a risk management firm. It discusses Spire's risk management solutions which include risk-based internal audits, compliance audits, internal financial controls, IT audits, and standard operating procedures. It then goes into further detail about Spire's approach to risk-based internal audits, compliance audits, and internal financial controls. The document emphasizes the importance of these risk management processes and Spire's role in providing professional services around them.CONTROL AND PERFORMANCE MANAGEMENT DOCUMENT

CONTROL AND PERFORMANCE MANAGEMENT DOCUMENTvini henry

╠²

The document discusses the importance of the control process in management, which ensures organizational activities align with set goals through systematic steps such as establishing objectives, measuring performance, and taking corrective action. It outlines three types of control: financial, operational, and strategic, each with its own objectives, advantages, and challenges. Additionally, it emphasizes performance measurement and evaluation as critical for organizational accountability, strategic alignment, and continuous improvement.The Internal Audit Framework

The Internal Audit FrameworkAhmad Tariq Bhatti

╠²

The document outlines the internal audit framework which serves as a systematic approach for organizations to evaluate and improve risk management, control, and governance processes. It details the roles and responsibilities of internal auditors, the types of audits, and emphasizes the importance of independence and objectivity. Additionally, it includes guidance on risk management processes, audit planning, and how the internal audit team contributes to the overall governance structure of the organization.Strategic evaluation

Strategic evaluationShahidAli433

╠²

The document discusses strategic evaluation and its importance. Strategic evaluation involves collecting information to assess how well a strategic plan is progressing against its goals. It examines the bases of a firm's strategy, compares expected to actual results, and identifies corrective actions. Strategic evaluation is beneficial for organizations of all sizes as it provides feedback for future decisions and assesses performance relative to goals. Common techniques for strategic evaluation include gap analysis, SWOT analysis, PEST analysis, and benchmarking.control technique's

control technique'schetan birla

╠²

This document discusses various control techniques that managers can use to effectively control organizational activities. It categorizes control techniques into general, special, and advanced techniques. Some general techniques discussed include personal observation, written communication, records and reports, standard costing, break even analysis, statistical data, self control, and return on investment. Special techniques include budgeting control, quality control, marketing control, human resource control, and financial statement control. Advanced techniques discussed are management information systems, PERT and CPM, zero base budgeting, and management audits.Performance audit adding value

Performance audit adding valueicgfmconference

╠²

This document provides a summary of a presentation on performance auditing. The presentation objectives are to understand the landscape of internal auditing, increase ability to work with management, analyze risks, and learn value-for-money approaches. The presentation covers the definition of internal auditing, performance audits, management functions, performance measures, and the International Standards for internal auditing. The benefits of performance audits are that they are relevant, flexible, improve organizational performance, and strengthen governance.Chapter 4 - Risk and Internal Control.ppt

Chapter 4 - Risk and Internal Control.pptHairizalHarun1

╠²

An internal control system is essential for organizations to manage risks and achieve goals, as defined by both Bursa Malaysia and COSO. It encompasses various components such as control environment, risk assessment, and control activities, which are vital for maintaining operational integrity and compliance with laws. Types of controls include preventive measures to avoid errors and detective measures to identify and address issues after they occur.Xybion - best practices for audit management - final

Xybion - best practices for audit management - finalXybion Corporation

╠²

The document outlines best practices for audit management, emphasizing the integration of risk management and auditing processes to enhance organizational efficiency and compliance. It discusses various types of audits, the importance of adapting to evolving organizational needs, and the necessity of using technology to streamline audit processes. Key recommendations include developing a strategic audit plan, improving communication, and utilizing performance metrics to foster continuous improvement in audit functions.Unit 07

Unit 07Sagar Tripathi

╠²

This document discusses the controlling function of management. Controlling involves verifying whether organizational goals are achieved according to standards by comparing actual and standard performance and taking corrective actions. It helps management minimize deviations and achieve goals efficiently. The effectiveness of controlling depends on the efficiency of planning, as planning defines goals and objectives while controlling monitors their accomplishment. Controlling guides managers to monitor subordinates' performance and provide feedback to improve it.Risk based auditing

Risk based auditingTunde Elijah Kelani

╠²

The document discusses risk-based auditing (RBIA) and its key concepts. RBIA requires internal audit to be strategically linked to an organization's risk management and assurance frameworks. It also discusses applying RBIA methodology to internal audit assignments and linking an organization's risk framework to the stages of RBIA. The document provides information on introducing RBIA to an organization and adapting it based on the organization's structures, processes and risk maturity.Internal Audit And Internal Control Presentation Leo Wachira

Internal Audit And Internal Control Presentation Leo WachiraJenard Wachira

╠²

Internal auditing and internal controls are important functions for oversight and governance. Internal auditing provides independent assurance to help an organization accomplish its objectives. It evaluates risk management, controls, and governance processes. Internal controls consist of control environment, risk assessment, information and communication, monitoring, and control activities. The purpose is to help an organization achieve its goals. Common weaknesses include human error, deliberate circumvention, management override, and cost considerations.Controlling,Process,Types & Techniques.pptx

Controlling,Process,Types & Techniques.pptxParthGupta524776

╠²

The document discusses the controlling function in management, emphasizing the importance of comparing actual performance to set standards and taking corrective actions. It outlines various traditional and modern techniques of control, including budgetary control, responsibility accounting, management audits, and the use of technology for real-time monitoring and analysis. Additionally, it addresses challenges posed by IT as a control tool, such as cybersecurity threats, data privacy concerns, and the need for effective change management.Performance management

Performance managementAbhiram Sadhu

╠²

Performance management is used to align employee performance with organizational goals through establishing frameworks to direct, monitor, evaluate, and reward individual performance. It is widely used and has both strategic and individual importance, but can be difficult for managers. Effective performance management systems include setting objectives, reviewing performance against objectives, identifying development needs, and linking individual and team objectives. Key aspects include conducting appraisal interviews with open questions, active listening, providing evidence-based feedback, and ending positively with agreed action plans.Strategy Evaluation

Strategy Evaluation Taher Ahmed

╠²

The document outlines the process of strategy evaluation, which includes assessing the effectiveness of strategic plans through activities like comparing actual results with expectations, and identifying the need for corrective actions. It discusses the importance of timely and adequate information, challenges in conducting evaluations, and various techniques such as gap analysis, SWOT, and benchmarking. Ultimately, the evaluation process is presented as crucial for aligning strategies with organizational objectives, ensuring resources are used effectively, and maintaining competitive advantage.Pm

Pm AKSHAYA0000

╠²

Performance appraisal involves evaluating an employee's overall contribution in the past, while performance management is an ongoing process of planning, monitoring, and evaluating employee objectives and contributions. Performance appraisal focuses on individual performance and mistakes, has an individualistic perspective, and is rigid, while performance management focuses on growth, has a holistic perspective, and is flexible.

An unsuccessful performance management system lacks structure, communication, and recognition/rewards. Goals are not considered and recent performances are overemphasized. It relies solely on annual evaluations. A successful system is accurate, fair, efficient, elevates performance, uses multiple data sources, includes coaching skills development, and links compensation decisions to performance rather than using them as the main purposeAd

More from Vernon Benjamin (8)

AOP Template

AOP TemplateVernon Benjamin

╠²

The document describes the audit process used by the Department of Audit Services at Montefiore Medical Center, including selecting audit areas, notifying the auditee, conducting an entrance conference, performing fieldwork to review processes and transactions, having an exit conference to discuss findings, and issuing an audit report with any recommendations. The goal is to work with management to evaluate controls and processes, identify risks, and recommend improvements through an objective review.IAD Introduction - 1-2010

IAD Introduction - 1-2010Vernon Benjamin

╠²

The document provides an introduction to internal auditing at Morris Heights Health Center. It discusses that the purpose of internal auditing is to independently evaluate an organization's activities as a service to help management meet goals, assess and monitor risks, and ensure compliance. The internal audit process involves planning, performing fieldwork and testing, documenting results in a report. It describes how internal audit can help by objectively assessing operations and sharing best practices to improve controls, processes and risk management. Finally, it notes that building trust with auditees is important by keeping commitments and through collaboration.IAD Introduction to Lexington - 5-2011

IAD Introduction to Lexington - 5-2011Vernon Benjamin

╠²

Internal auditing is an independent function that examines and evaluates an organization's activities to help the organization meet its goals and comply with regulations. The objective of internal auditing is to assess risks, monitor controls, and promote effective internal controls. Internal auditing provides assessments, analyses, advice, and assistance through an objective review of operations, identification of best practices, and recommendations for improving processes and managing risks. The internal audit process involves planning, performing, and reporting audits to research, assess risks, develop audit programs, perform fieldwork, and document findings.2012 Automating The Audit Function Presentation

2012 Automating The Audit Function PresentationVernon Benjamin

╠²

The document outlines a vision for automating the audit process through a fully integrated, multi-dimensional automated audit system that provides a single point of entry. The system would be a Windows-based tool that supports mobile teams, enhances productivity, and enables effective teamwork through components like regulatory compliance, risk assessment, audit planning, workpaper and comment tracking. The system aims to streamline the audit process, provide centralized management of audits, and allow sharing and reviewing of audit information from any location.Basic Internal Auditing Presentation

Basic Internal Auditing PresentationVernon Benjamin

╠²

The document discusses the purpose and role of internal auditing. It describes internal auditing as an independent function that examines and evaluates an organization's activities to help management discharge their responsibilities effectively. The objective is to promote control within the organization at a reasonable cost. The document outlines the audit process, including planning, performing, reporting, and following up on corrective actions. It provides best practices for tasks like risk assessment, test design, documentation, reporting findings, and building trust with auditees.Basic Internal Auditing Presentation

Basic Internal Auditing PresentationVernon Benjamin

╠²

The document provides an overview of internal auditing basics and best practices. It discusses the purpose and objectives of internal auditing, which includes independently evaluating activities within an organization to examine controls and ensure responsibilities are carried out effectively and efficiently. The document also outlines the audit process, including planning, performing, and reporting phases. It describes establishing objectives and scope, assessing risks, designing tests, documenting work, summarizing results, and following up on corrective actions. The overall goal is to help organizations achieve their objectives and promote continuous improvement.Automating The Audit Function Presentation

Automating The Audit Function Presentation Vernon Benjamin

╠²

The document discusses automating the internal audit process through a centralized automated audit system. The system would integrate planning, workpapers, tracking, tools, and other audit components. It would provide mobility, enable teamwork, and enhance productivity. The system would integrate with other applications and provide connectivity across locations. Its goals are to streamline the audit process, use a risk-based approach, provide centralized management, electronic sharing of information, and tracking of issues from start to resolution.Automating The Audit Function Presentation

Automating The Audit Function PresentationVernon Benjamin

╠²

The document discusses automating the audit process through a fully integrated automated audit system. The system is a Windows-based tool that supports mobile teams, enhances productivity, and enables more effective teamwork. It has components for audit tracking, comment tracking, regulatory compliance, workpapers, time keeping, and audit planning and risk assessment. The system integrates with applications like Lotus Notes, Microsoft Office, and Flowcharter, and connects to mainframes, databases, workstations, and remote locations. It streamlines the audit process, uses a risk-based approach, provides centralized management of audits, and allows sharing and reviewing of information from any location.Ad

Process Level Auditing 2012

- 2. What is Process Level Auditing (PLA)? ’ü« PLA means the auditor acts as a facilitator to help the managers of a group of related activities assess the control strengths and weakness. Together, we develop action plans for improvement, where necessary.

- 3. In a PLA Environment: ’ü« All existing controls and procedures are reviewed by managers and auditors to determine what is needed for improved efficiency. ’ü« Internal Audit, in the capacity of in-house consultant, works with the "client" to enhance the operations of the various departments.

- 4. How Will Process Level Auditing Improve the Organization? ’āśThe managers' operational knowledge of the process becomes part of the audit. ’āśEach segment of the process is summed into one continuous flow. ’āśThe managers gain an understanding of how the activities in their segment impact the process. ’āśThe risks factors are assessed for potential impact to the process, and controls are applied for maximum efficiency and effectiveness.

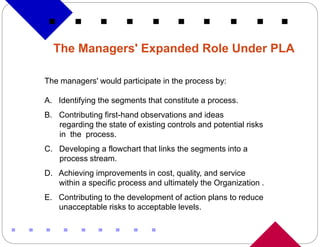

- 5. The Managers' Expanded Role Under PLA The managers' would participate in the process by: A. Identifying the segments that constitute a process. B. Contributing first-hand observations and ideas regarding the state of existing controls and potential risks in the process. C. Developing a flowchart that links the segments into a process stream. D. Achieving improvements in cost, quality, and service within a specific process and ultimately the Organization . E. Contributing to the development of action plans to reduce unacceptable risks to acceptable levels.

- 6. Tools used in a PLA Environment

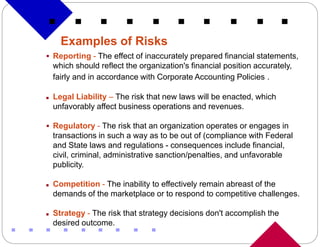

- 7. Examples of Risks ’é¦ Reporting - The effect of inaccurately prepared financial statements, which should reflect the organization's financial position accurately, fairly and in accordance with Corporate Accounting Policies . ’ü« Legal Liability ŌĆō The risk that new laws will be enacted, which unfavorably affect business operations and revenues. ’é¦ Regulatory - The risk that an organization operates or engages in transactions in such a way as to be out of (compliance with Federal and State laws and regulations - consequences include financial, civil, criminal, administrative sanction/penalties, and unfavorable publicity. ’ü« Competition - The inability to effectively remain abreast of the demands of the marketplace or to respond to competitive challenges. ’ü« Strategy - The risk that strategy decisions don't accomplish the desired outcome.

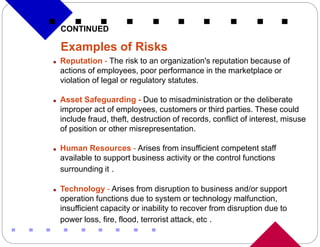

- 8. CONTINUED Examples of Risks ’ü« Reputation - The risk to an organization's reputation because of actions of employees, poor performance in the marketplace or violation of legal or regulatory statutes. ’ü« Asset Safeguarding - Due to misadministration or the deliberate improper act of employees, customers or third parties. These could include fraud, theft, destruction of records, conflict of interest, misuse of position or other misrepresentation. ’ü« Human Resources - Arises from insufficient competent staff available to support business activity or the control functions surrounding it . ’ü« Technology - Arises from disruption to business and/or support operation functions due to system or technology malfunction, insufficient capacity or inability to recover from disruption due to power loss, fire, flood, terrorist attack, etc .