1 of 7

Download to read offline

Ad

Recommended

SLR.pptx

SLR.pptxdefault default

?

The statutory liquidity ratio (SLR) refers to the proportion of deposits that commercial banks must maintain as liquid assets, such as government bonds and cash, as determined by the central bank. The SLR is used to control bank credit levels, ensure bank solvency, and compel banks to invest in government securities. If banks do not maintain the required SLR percentage, they are charged penalties. The SLR helps the government sell securities and supports the central bank's monetary policy objectives.Slr(Statutory Liquidity Ratio)

Slr(Statutory Liquidity Ratio)anant agarwal

?

The document discusses the statutory liquidity ratio (SLR) maintained by commercial banks in India at the direction of the Reserve Bank of India (RBI). The SLR is the percentage of total deposits and liabilities that banks must hold as cash, gold, or approved government securities. Adjusting the SLR allows RBI to expand or contract the money supply and control inflation or recession. A higher SLR decreases bank lending capacity, while a lower SLR increases lending. RBI modifies the SLR between 24-40% to influence aggregate demand and prices depending on economic conditions.Fshhsgygsggsgsgggsgsgsgsghh(2021031.pptx

Fshhsgygsggsgsgggsgsgsgsghh(2021031.pptxsarathisarathimajor

?

The Statutory Liquidity Ratio (SLR) is the minimum percentage of deposits that commercial banks must maintain in liquid assets like cash, gold, or securities, regulated by the Reserve Bank of India (RBI). SLR impacts the economy by controlling inflation, stabilizing the banking system, and ensuring solvency, with penalties for banks that fail to comply. The RBI can adjust the SLR to influence credit availability during inflation or recession.Dipak

DipakJay Shah

?

SLR refers to the statutory liquidity ratio, which is the minimum ratio of liquid assets like cash, gold, and approved securities that banks must maintain as a proportion of their net demand and time liabilities. The ratio is set by the central bank, currently the Reserve Bank of India, and can range between 25-40%. CRR refers to the cash reserve ratio, which is the minimum amount of total deposits that banks must maintain as cash reserves with the central bank. This ratio is also set by the central bank and is currently 5.75% in India. PLR refers to prime lending rates, which are interest rates charged to banks' most creditworthy corporate customers.What is CRR SLR Lares Algotech Broker Company

What is CRR SLR Lares Algotech Broker Companyrohanptx

?

In the complex framework of Indian banking and monetary policy, two terms often arise when discussing regulatory controls over liquidity and inflation: CRR (Cash Reserve Ratio) and SLR (Statutory Liquidity Ratio). These are monetary tools mandated by the Reserve Bank of India (RBI) that directly influence the economyˇŻs money supply, credit availability, interest rates, and overall financial stability. Understanding CRR and SLR is essential not only for economists and bankers but also for students, investors, and anyone interested in how a country manages its financial system.Crr and slr

Crr and slrShyamendra Verma

?

The document discusses the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) requirements for banks in India. It defines CRR as the minimum proportion of demand and time liabilities that scheduled commercial banks must maintain as reserves with the Reserve Bank of India. Similarly, SLR is the minimum level of liquid assets like cash, gold, and government securities that banks must hold as a percentage of their net demand and time liabilities. The document outlines the calculation processes for CRR and SLR, categories included and exempted from the ratios, and how the ratios provide RBI tools to control liquidity in the banking system. It also reviews how CRR and SLR have changed over time and perspectivesRbi(alok singh kanpur)

Rbi(alok singh kanpur)Alok Singh

?

The Reserve Bank of India was established in 1935 under the Reserve Bank of India Act. It is headquartered in Mumbai and led by a Governor and up to four Deputy Governors. The RBI sets the cash reserve ratio (CRR) and statutory liquidity ratio (SLR), requiring banks to hold certain percentages of deposits in cash reserves and government securities. This ensures banks maintain enough liquid funds to meet depositor withdrawals and allows the RBI to control monetary policy by managing liquidity levels in the economy.Monetary Terms

Monetary Terms Fine Advice Private Limited

?

This document discusses two key monetary policy tools used by the Reserve Bank of India (RBI): the repo rate and statutory liquidity ratio (SLR). The repo rate is the rate at which banks borrow funds from RBI, and cutting this rate makes borrowing cheaper for banks. The SLR is the minimum reserve of liquid assets like cash or government bonds that banks must hold, and cutting the SLR frees up more funds for banks to lend. Recently, RBI cut the repo rate by 150 basis points to 7.5% and the SLR by 100 basis points to 24% to make borrowing cheaper for banks and allow them to lend more.PERFORMANCE EVALUATION OF BANKS.ppt To tu tu to

PERFORMANCE EVALUATION OF BANKS.ppt To tu tu tomanoravichandran10

?

The document discusses the performance evaluation of banks, focusing on the deployment of funds, treasury operations, and liquidity management. It outlines the roles and functions of the treasury department, including the management of cash flow, investments, and compliance with statutory liquidity ratios (SLR) and cash reserve ratios (CRR). Additionally, it covers banking products and liquidity adjustment mechanisms, detailing the processes for borrowing and lending within the banking system.CRR AND SLR

CRR AND SLRRAJEEV MISHRA

?

Cash Reserve Ratio (CRR) requires scheduled commercial banks to maintain 4.75% of their total net demand and time liabilities as reserves with the RBI without interest to ensure liquidity and solvency. Statutory Liquidity Ratio (SLR) requires banks to maintain a minimum of 23% of their net demand and time liabilities as liquid assets such as cash, gold or approved government securities. Non-compliance with CRR and SLR requirements results in penal interest rates being charged to banks by the RBI. Together, CRR and SLR comprise the liquidity reserves that banks must maintain.Treasury Management

Treasury ManagementKalpesh Arvind Shah

?

1) Non-SLR securities are investments made by banks that are not mandated by statutory liquidity ratio requirements. They include investments in stocks, bonds, mutual funds, commercial paper, and other capital market instruments.

2) These investments carry more risk than SLR investments in government securities but can provide higher returns. Risks include security selection, credit risk, market risk, liquidity risk, and more.

3) Guidelines from the RBI specify limits on non-SLR investments and criteria for eligible securities. Banks must also comply with prudential norms on income recognition, asset classification, and provisioning for these investments.Monetary policy of india 2013

Monetary policy of india 2013ARJUN RAJAN KAUL

?

Monetary policy in India, governed by the Reserve Bank of India (RBI), aims to control the money supply to maintain price stability and support economic growth. Key components include measures of money stock (M1, M2, M3, M4), the statutory liquidity ratio (SLR), cash reserve ratio (CRR), and the repo and reverse repo rates, which influence liquidity and borrowing costs. Current rates and ratios indicate the RBI's strategies to manage inflation and stimulate or restrict economic activity.Treasury Management

Treasury ManagementKalpesh Arvind Shah

?

The document discusses the concept of non-statutory liquidity ratio (SLR) investments and the associated risks, contrasting them with statutory liquidity ratio requirements for banks in India. It explains various forms of non-SLR investments such as corporate bonds, mutual funds, and equities, emphasizing that these investments are market-driven and carry higher risk compared to SLR investments, which are considered safer. Additionally, it outlines regulatory frameworks, investment guidelines, and the risk factors involved in non-SLR investments.QUANTITATIVE TOOLS OF MONETARY POLICY

QUANTITATIVE TOOLS OF MONETARY POLICYAjaySatheesan

?

The Reserve Bank of India lowered its benchmark repo rate by 25 basis points to 5.75% to boost economic growth amid a slowdown. This was the third consecutive rate cut by the RBI in 2019 and changed its policy stance to accommodative from neutral. The rate cut comes as India's GDP growth forecast was reduced to 7% for fiscal year 2020 due to weaker investment and consumption growth. Inflation projections were also increased slightly but price stability remains a key objective along with supporting growth. Other measures announced included waiving digital transaction fees and setting up panels to review ATM charges and small finance bank licensing.Four monetary terms part 1

Four monetary terms part 1Tata Mutual Fund

?

The document provides an overview of two key Indian monetary policy terms: the repo rate and statutory liquidity ratio (SLR). The repo rate is the interest rate at which commercial banks borrow funds from the Reserve Bank of India. A reduction in the repo rate will allow banks to borrow funds at a cheaper rate. The SLR is the minimum amount of funds that commercial banks must hold in government approved securities. The SLR is set by the RBI and helps control the expansion of bank credit. The SLR has recently been reduced by 100 basis points to 24% of deposits, freeing up more cash for banks to lend.REPO Rate and Reverse REPO Rate

REPO Rate and Reverse REPO Rateramrag2001

?

The document provides an overview of two key Indian monetary policy terms: the repo rate and statutory liquidity ratio (SLR). The repo rate is the interest rate at which commercial banks borrow funds from the Reserve Bank of India. A reduction in the repo rate will allow banks to borrow funds at a cheaper rate. The SLR is the minimum amount of funds that commercial banks must hold in government approved securities. The SLR is set by the RBI and helps control the expansion of bank credit. The SLR has recently been reduced by 100 basis points to 24% of deposits, freeing up more cash for banks to lend.CRR & SLR

CRR & SLRBhavana Nandu

?

The document discusses the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) requirements for banks in India. It notes that the RBI sets the minimum and maximum ratios for CRR (currently between 3-15%) and SLR (currently between 20-40%). It provides the current CRR and SLR rates, and explains how the ratios are calculated based on banks' net demand and time liabilities. It also discusses the impacts of increasing or decreasing these ratios, such as how a reduction in CRR or SLR increases banks' lending capacity.Financial Inclusion and All Rates

Financial Inclusion and All RatesAman Singh (???)

?

This document provides information on various key terms related to financial inclusion and interest rates in India. It defines financial inclusion as ensuring access to appropriate financial products and services for all sections of society, especially vulnerable groups, at an affordable cost. It discusses the Reserve Bank of India's role in promoting financial inclusion through various initiatives like no-frills accounts, business correspondent models, and financial literacy programs. The document also explains terms like repo rate, reverse repo rate, cash reserve ratio, statutory liquidity ratio, base rate, and call rates which are tools used by RBI to regulate monetary policy and liquidity in the banking system.Macro economics

Macro economicsAaryendr

?

The document discusses several key concepts in monetary policy and macroeconomics:

1) Monetary policy aims to control money supply and borrowing costs in the economy to manage inflation and is implemented by the Reserve Bank of India (RBI).

2) Fiscal policy uses government spending and taxation to achieve macroeconomic objectives like economic growth.

3) GDP, a measure of economic growth, is calculated as the total of consumption, investment, government spending, and net exports in an economy.

4) The RBI uses various tools like the cash reserve ratio (CRR), repo rate, reverse repo rate, and statutory liquidity ratio (SLR) to control money supply and influence lending behavior of commercialBank gk

Bank gkjesseanbu

?

The Reserve Bank of India (RBI) is India's central bank. It has sole authority to issue currency and regulates banking operations. The current governor is Duvvuri Subbarao, with four deputy governors. RBI maintains monetary policy and ensures adequate credit flows. It regulates the financial system, sets parameters for banking, and addresses customer complaints. RBI also manages foreign exchange and issues currency. Key tools include repo rate, reverse repo rate, statutory liquidity ratio, and cash reserve ratio.Monetry Policy (India)

Monetry Policy (India)NAITIK KASAVALA

?

The document discusses various tools used by the Reserve Bank of India (RBI) to control inflation, including monetary policy, statutory liquidity ratio (SLR), bank rate, cash reserve ratio (CRR), repo and reverse repo rates, and marginal standing facility (MSF). Each tool is defined with its features and importance, such as how CRR helps in maintaining liquidity and controlling inflation. Additionally, the document provides historical data on SLR, bank rate, CRR, and other monetary policy tools over the last 10 years.Crr and slr management

Crr and slr managementAnanya Jain

?

The document discusses the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR), explaining their definitions, significance in monetary policy, and current rates. It outlines how CRR is a requirement for banks to hold a fraction of deposits in cash, while SLR mandates the maintenance of liquid assets. Additionally, it covers the different types of financial institutions and methods of valuation relevant to investment analysis.Monetry policy

Monetry policyaman sharma

?

This document discusses monetary policy in India. It defines monetary policy as the central government's policy with respect to the quantity of money in the economy, interest rates, and exchange rates, as executed by the Reserve Bank of India. The objectives of monetary policy are maintaining price stability, ensuring adequate credit flows to support growth, rapid economic growth, full employment, and equal income distribution. The methods used to achieve these objectives include both qualitative methods like directing lending to priority sectors, and quantitative methods like required reserve ratios, statutory liquidity ratios, and repo and reverse repo rates which the central bank uses to control money flows.RBI Credit Control

RBI Credit ControlWaqas Syed

?

The RBI is responsible for controlling inflation through various credit control measures including quantitative and qualitative methods such as bank rates, cash reserve ratio (CRR), and statutory liquidity ratio (SLR). It employs open market operations and selective credit controls to influence credit availability and ensure resources flow into essential sectors. Additionally, the RBI plays a pivotal role in the development of commercial banks, agricultural and industrial finance, and in promoting exports to enhance trade balance.Instruments of monetary control

Instruments of monetary controlAdarsh Jamwal

?

The Reserve Bank of India (RBI) uses various instruments of monetary policy to control the supply of money in the economy and maintain price stability. These include direct tools like the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR), which require banks to hold certain percentages of deposits as cash reserves and government securities. Indirect tools include the repo rate and reverse repo rate, which are the interest rates at which the RBI lends to and borrows from commercial banks. By adjusting these rates, the RBI can increase or decrease the availability of funds in the economy in order to manage inflation and economic growth.RBI Terms

RBI TermsSukhdeep Singh Brar

?

This document discusses several key monetary policy tools used by the Reserve Bank of India (RBI) to regulate the money supply and control inflation in India. It explains that the bank rate is the rate at which RBI lends to other banks, and an increase in bank rate will likely lead to an increase in other lending rates. It also discusses the cash reserve ratio (CRR), which is the amount of funds banks must keep with RBI, and how increasing the CRR drains excess liquidity from banks. The statutory liquidity ratio (SLR) requires banks to maintain a minimum level of liquid assets. Other tools covered include the repo rate, reverse repo rate, prime lending rate, and base rate. The documentQuantitative tools of monetary policy

Quantitative tools of monetary policyParveen Kumar

?

This document discusses monetary policy and its instruments. It defines monetary policy as the process by which a central bank controls the supply of money in order to promote economic growth and stability. The key instruments of monetary policy discussed are: open market operations, bank rate/discount rate, cash reserve ratio, statutory liquidity ratio. Quantitative measures include open market operations, bank rate, cash reserve ratio while qualitative measures comprise selective credit controls. The effectiveness of these tools depends on the level of monetization and development of the capital market in an economy.TOOLS OF MONETARY POLICY

TOOLS OF MONETARY POLICYKartik Parashar

?

The document discusses various tools of monetary policy used in India, including cash reserve ratio (CRR), statutory liquidity ratio (SLR), repo rate, reverse repo rate, bank rate, and prime lending rate. CRR is the minimum amount of deposits that banks must maintain as reserves with the central bank. SLR is the minimum amount of deposits that must be maintained as approved securities like cash or gold. Repo and reverse repo rates are the interest rates at which the central bank lends to and borrows from commercial banks. The bank rate is the interest rate at which the central bank lends to commercial banks without collateral.×îĐ°ćĂŔąúĐÝËą¶Ů´óѧ±Ďҵ֤Ł¨±«±á±Ďҵ֤Ę飩԰涨ÖĆ

×îĐ°ćĂŔąúĐÝËą¶Ů´óѧ±Ďҵ֤Ł¨±«±á±Ďҵ֤Ę飩԰涨ÖĆTaqyea

?

ĽřÓÚ´ËŁ¬¶¨ÖĆĐÝËą¶Ů´óѧѧλ֤ĘéĚáÉýÂÄŔúˇľqޱ1954292140ˇżÔ°ć¸ß·ÂĐÝËą¶Ů´óѧ±Ďҵ֤(UH±Ďҵ֤Ęé)żÉĎČż´łÉĆ·Ńů±ľˇľqޱ1954292140ˇż°ďÄú˝âľöÔÚĂŔąúĐÝËą¶Ů´óѧδ±ĎҵÄŃĚ⣬ĂŔąú±Ďҵ֤ąşÂňŁ¬ĂŔąúÎÄĆľąşÂňŁ¬ˇľq΢1954292140ˇżĂŔąúÎÄĆľąşÂňŁ¬ĂŔąúÎÄĆľ¶¨ÖĆŁ¬ĂŔąúÎÄĆľ˛ą°ěˇŁ×¨ŇµÔÚĎ߶¨ÖĆĂŔąú´óѧÎÄĆľŁ¬¶¨×öĂŔąú±ľżĆÎÄĆľŁ¬ˇľq΢1954292140ˇż¸´ÖĆĂŔąúThe University of Houston completion letterˇŁÔÚĎßżěËٲą°ěĂŔąú±ľżĆ±Ďҵ֤ˇ˘Ë¶ĘżÎÄĆľÖ¤Ę飬ąşÂňĂŔąúѧλ֤ˇ˘ĐÝËą¶Ů´óѧOfferŁ¬ĂŔąú´óѧÎÄĆľÔÚĎßąşÂňˇŁ

ČçąűÄú´¦ÓÚŇÔĎÂĽ¸ÖÖÇéżöŁş

ˇóÔÚĐŁĆڼ䣬Ňň¸÷ÖÖÔŇňδÄÜËłŔű±ĎҵˇˇÄò»µ˝ąŮ·˝±Ďҵ֤

ˇóĂć¶Ô¸¸Ä¸µÄŃąÁ¦Ł¬ĎŁÍűľˇżěÄõ˝Ł»

ˇó˛»ÇĺłţČĎÖ¤Á÷łĚŇÔĽ°˛ÄÁϸĂČçşÎ׼±¸Ł»

ˇó»ŘąúʱĽäşÜł¤Ł¬ÍüĽÇ°ěŔíŁ»

ˇó»ŘąúÂíÉĎľÍŇŞŐŇą¤×÷Ł¬°ě¸řÓĂČ˵ĄÎ»ż´Ł»

ˇóĆóĘÂҵµĄÎ»±ŘĐëŇŞÇó°ěŔíµÄ

ˇóĐčŇŞ±¨żĽą«ÎńÔ±ˇ˘ąşÂňĂâË°łµˇ˘Âäת»§żÚ

ˇóÉęÇëÁôѧÉú´´Ňµ»ů˝đ

ˇľ¸´żĚŇ»Ě×ĐÝËą¶Ů´óѧ±Ďҵ֤łÉĽ¨µĄĐĹ·âµČ˛ÄÁĎ×îÇżąĄÂÔ,Buy The University of Houston Transcriptsˇż

ąşÂňČŐş«łÉĽ¨µĄˇ˘Ó˘ąú´óѧłÉĽ¨µĄˇ˘ĂŔąú´óѧłÉĽ¨µĄˇ˘°ÄÖŢ´óѧłÉĽ¨µĄˇ˘ĽÓÄĂ´ó´óѧłÉĽ¨µĄŁ¨q΢1954292140Ł©ĐÂĽÓĆ´óѧłÉĽ¨µĄˇ˘ĐÂÎ÷ŔĽ´óѧłÉĽ¨µĄˇ˘°®¶űŔĽłÉĽ¨µĄˇ˘Î÷°ŕŃŔłÉĽ¨µĄˇ˘µÂąúłÉĽ¨µĄˇŁłÉĽ¨µĄµÄŇâŇĺÖ÷ŇŞĚĺĎÖÔÚÖ¤Ă÷ѧϰÄÜÁ¦ˇ˘ĆŔąŔѧĘő±łľ°ˇ˘ŐąĘľ×ŰşĎËŘÖʡ˘Ěá¸ß¼ȡÂĘŁ¬ŇÔĽ°ĘÇ×÷ÎŞÁôĐĹČĎÖ¤ÉęÇë˛ÄÁϵÄŇ»˛ż·ÖˇŁ

ĐÝËą¶Ů´óѧłÉĽ¨µĄÄÜą»ĚĺĎÖÄúµÄµÄѧϰÄÜÁ¦Ł¬°üŔ¨ĐÝËą¶Ů´óѧżÎłĚłÉĽ¨ˇ˘×¨ŇµÄÜÁ¦ˇ˘ŃĐľżÄÜÁ¦ˇŁŁ¨q΢1954292140Ł©ľßĚĺŔ´ËµŁ¬łÉĽ¨±¨¸ćµĄÍ¨łŁ°üş¬Ń§ÉúµÄѧϰĽĽÄÜÓëĎ°ąßˇ˘¸÷żĆłÉĽ¨ŇÔĽ°ŔĎʦĆŔÓďµČ˛ż·ÖŁ¬Ňň´ËŁ¬łÉĽ¨µĄ˛»˝öĘÇѧÉúѧĘőÄÜÁ¦µÄÖ¤Ă÷Ł¬Ň˛ĘÇĆŔąŔѧÉúĘÇ·ńĘĘşĎÄł¸ö˝ĚÓýĎîÄżµÄÖŘŇŞŇŔľÝŁˇMore Related Content

Similar to SLR_Presentation.pptx okay SLRSLRSLRSLRSLR (20)

PERFORMANCE EVALUATION OF BANKS.ppt To tu tu to

PERFORMANCE EVALUATION OF BANKS.ppt To tu tu tomanoravichandran10

?

The document discusses the performance evaluation of banks, focusing on the deployment of funds, treasury operations, and liquidity management. It outlines the roles and functions of the treasury department, including the management of cash flow, investments, and compliance with statutory liquidity ratios (SLR) and cash reserve ratios (CRR). Additionally, it covers banking products and liquidity adjustment mechanisms, detailing the processes for borrowing and lending within the banking system.CRR AND SLR

CRR AND SLRRAJEEV MISHRA

?

Cash Reserve Ratio (CRR) requires scheduled commercial banks to maintain 4.75% of their total net demand and time liabilities as reserves with the RBI without interest to ensure liquidity and solvency. Statutory Liquidity Ratio (SLR) requires banks to maintain a minimum of 23% of their net demand and time liabilities as liquid assets such as cash, gold or approved government securities. Non-compliance with CRR and SLR requirements results in penal interest rates being charged to banks by the RBI. Together, CRR and SLR comprise the liquidity reserves that banks must maintain.Treasury Management

Treasury ManagementKalpesh Arvind Shah

?

1) Non-SLR securities are investments made by banks that are not mandated by statutory liquidity ratio requirements. They include investments in stocks, bonds, mutual funds, commercial paper, and other capital market instruments.

2) These investments carry more risk than SLR investments in government securities but can provide higher returns. Risks include security selection, credit risk, market risk, liquidity risk, and more.

3) Guidelines from the RBI specify limits on non-SLR investments and criteria for eligible securities. Banks must also comply with prudential norms on income recognition, asset classification, and provisioning for these investments.Monetary policy of india 2013

Monetary policy of india 2013ARJUN RAJAN KAUL

?

Monetary policy in India, governed by the Reserve Bank of India (RBI), aims to control the money supply to maintain price stability and support economic growth. Key components include measures of money stock (M1, M2, M3, M4), the statutory liquidity ratio (SLR), cash reserve ratio (CRR), and the repo and reverse repo rates, which influence liquidity and borrowing costs. Current rates and ratios indicate the RBI's strategies to manage inflation and stimulate or restrict economic activity.Treasury Management

Treasury ManagementKalpesh Arvind Shah

?

The document discusses the concept of non-statutory liquidity ratio (SLR) investments and the associated risks, contrasting them with statutory liquidity ratio requirements for banks in India. It explains various forms of non-SLR investments such as corporate bonds, mutual funds, and equities, emphasizing that these investments are market-driven and carry higher risk compared to SLR investments, which are considered safer. Additionally, it outlines regulatory frameworks, investment guidelines, and the risk factors involved in non-SLR investments.QUANTITATIVE TOOLS OF MONETARY POLICY

QUANTITATIVE TOOLS OF MONETARY POLICYAjaySatheesan

?

The Reserve Bank of India lowered its benchmark repo rate by 25 basis points to 5.75% to boost economic growth amid a slowdown. This was the third consecutive rate cut by the RBI in 2019 and changed its policy stance to accommodative from neutral. The rate cut comes as India's GDP growth forecast was reduced to 7% for fiscal year 2020 due to weaker investment and consumption growth. Inflation projections were also increased slightly but price stability remains a key objective along with supporting growth. Other measures announced included waiving digital transaction fees and setting up panels to review ATM charges and small finance bank licensing.Four monetary terms part 1

Four monetary terms part 1Tata Mutual Fund

?

The document provides an overview of two key Indian monetary policy terms: the repo rate and statutory liquidity ratio (SLR). The repo rate is the interest rate at which commercial banks borrow funds from the Reserve Bank of India. A reduction in the repo rate will allow banks to borrow funds at a cheaper rate. The SLR is the minimum amount of funds that commercial banks must hold in government approved securities. The SLR is set by the RBI and helps control the expansion of bank credit. The SLR has recently been reduced by 100 basis points to 24% of deposits, freeing up more cash for banks to lend.REPO Rate and Reverse REPO Rate

REPO Rate and Reverse REPO Rateramrag2001

?

The document provides an overview of two key Indian monetary policy terms: the repo rate and statutory liquidity ratio (SLR). The repo rate is the interest rate at which commercial banks borrow funds from the Reserve Bank of India. A reduction in the repo rate will allow banks to borrow funds at a cheaper rate. The SLR is the minimum amount of funds that commercial banks must hold in government approved securities. The SLR is set by the RBI and helps control the expansion of bank credit. The SLR has recently been reduced by 100 basis points to 24% of deposits, freeing up more cash for banks to lend.CRR & SLR

CRR & SLRBhavana Nandu

?

The document discusses the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) requirements for banks in India. It notes that the RBI sets the minimum and maximum ratios for CRR (currently between 3-15%) and SLR (currently between 20-40%). It provides the current CRR and SLR rates, and explains how the ratios are calculated based on banks' net demand and time liabilities. It also discusses the impacts of increasing or decreasing these ratios, such as how a reduction in CRR or SLR increases banks' lending capacity.Financial Inclusion and All Rates

Financial Inclusion and All RatesAman Singh (???)

?

This document provides information on various key terms related to financial inclusion and interest rates in India. It defines financial inclusion as ensuring access to appropriate financial products and services for all sections of society, especially vulnerable groups, at an affordable cost. It discusses the Reserve Bank of India's role in promoting financial inclusion through various initiatives like no-frills accounts, business correspondent models, and financial literacy programs. The document also explains terms like repo rate, reverse repo rate, cash reserve ratio, statutory liquidity ratio, base rate, and call rates which are tools used by RBI to regulate monetary policy and liquidity in the banking system.Macro economics

Macro economicsAaryendr

?

The document discusses several key concepts in monetary policy and macroeconomics:

1) Monetary policy aims to control money supply and borrowing costs in the economy to manage inflation and is implemented by the Reserve Bank of India (RBI).

2) Fiscal policy uses government spending and taxation to achieve macroeconomic objectives like economic growth.

3) GDP, a measure of economic growth, is calculated as the total of consumption, investment, government spending, and net exports in an economy.

4) The RBI uses various tools like the cash reserve ratio (CRR), repo rate, reverse repo rate, and statutory liquidity ratio (SLR) to control money supply and influence lending behavior of commercialBank gk

Bank gkjesseanbu

?

The Reserve Bank of India (RBI) is India's central bank. It has sole authority to issue currency and regulates banking operations. The current governor is Duvvuri Subbarao, with four deputy governors. RBI maintains monetary policy and ensures adequate credit flows. It regulates the financial system, sets parameters for banking, and addresses customer complaints. RBI also manages foreign exchange and issues currency. Key tools include repo rate, reverse repo rate, statutory liquidity ratio, and cash reserve ratio.Monetry Policy (India)

Monetry Policy (India)NAITIK KASAVALA

?

The document discusses various tools used by the Reserve Bank of India (RBI) to control inflation, including monetary policy, statutory liquidity ratio (SLR), bank rate, cash reserve ratio (CRR), repo and reverse repo rates, and marginal standing facility (MSF). Each tool is defined with its features and importance, such as how CRR helps in maintaining liquidity and controlling inflation. Additionally, the document provides historical data on SLR, bank rate, CRR, and other monetary policy tools over the last 10 years.Crr and slr management

Crr and slr managementAnanya Jain

?

The document discusses the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR), explaining their definitions, significance in monetary policy, and current rates. It outlines how CRR is a requirement for banks to hold a fraction of deposits in cash, while SLR mandates the maintenance of liquid assets. Additionally, it covers the different types of financial institutions and methods of valuation relevant to investment analysis.Monetry policy

Monetry policyaman sharma

?

This document discusses monetary policy in India. It defines monetary policy as the central government's policy with respect to the quantity of money in the economy, interest rates, and exchange rates, as executed by the Reserve Bank of India. The objectives of monetary policy are maintaining price stability, ensuring adequate credit flows to support growth, rapid economic growth, full employment, and equal income distribution. The methods used to achieve these objectives include both qualitative methods like directing lending to priority sectors, and quantitative methods like required reserve ratios, statutory liquidity ratios, and repo and reverse repo rates which the central bank uses to control money flows.RBI Credit Control

RBI Credit ControlWaqas Syed

?

The RBI is responsible for controlling inflation through various credit control measures including quantitative and qualitative methods such as bank rates, cash reserve ratio (CRR), and statutory liquidity ratio (SLR). It employs open market operations and selective credit controls to influence credit availability and ensure resources flow into essential sectors. Additionally, the RBI plays a pivotal role in the development of commercial banks, agricultural and industrial finance, and in promoting exports to enhance trade balance.Instruments of monetary control

Instruments of monetary controlAdarsh Jamwal

?

The Reserve Bank of India (RBI) uses various instruments of monetary policy to control the supply of money in the economy and maintain price stability. These include direct tools like the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR), which require banks to hold certain percentages of deposits as cash reserves and government securities. Indirect tools include the repo rate and reverse repo rate, which are the interest rates at which the RBI lends to and borrows from commercial banks. By adjusting these rates, the RBI can increase or decrease the availability of funds in the economy in order to manage inflation and economic growth.RBI Terms

RBI TermsSukhdeep Singh Brar

?

This document discusses several key monetary policy tools used by the Reserve Bank of India (RBI) to regulate the money supply and control inflation in India. It explains that the bank rate is the rate at which RBI lends to other banks, and an increase in bank rate will likely lead to an increase in other lending rates. It also discusses the cash reserve ratio (CRR), which is the amount of funds banks must keep with RBI, and how increasing the CRR drains excess liquidity from banks. The statutory liquidity ratio (SLR) requires banks to maintain a minimum level of liquid assets. Other tools covered include the repo rate, reverse repo rate, prime lending rate, and base rate. The documentQuantitative tools of monetary policy

Quantitative tools of monetary policyParveen Kumar

?

This document discusses monetary policy and its instruments. It defines monetary policy as the process by which a central bank controls the supply of money in order to promote economic growth and stability. The key instruments of monetary policy discussed are: open market operations, bank rate/discount rate, cash reserve ratio, statutory liquidity ratio. Quantitative measures include open market operations, bank rate, cash reserve ratio while qualitative measures comprise selective credit controls. The effectiveness of these tools depends on the level of monetization and development of the capital market in an economy.TOOLS OF MONETARY POLICY

TOOLS OF MONETARY POLICYKartik Parashar

?

The document discusses various tools of monetary policy used in India, including cash reserve ratio (CRR), statutory liquidity ratio (SLR), repo rate, reverse repo rate, bank rate, and prime lending rate. CRR is the minimum amount of deposits that banks must maintain as reserves with the central bank. SLR is the minimum amount of deposits that must be maintained as approved securities like cash or gold. Repo and reverse repo rates are the interest rates at which the central bank lends to and borrows from commercial banks. The bank rate is the interest rate at which the central bank lends to commercial banks without collateral.Recently uploaded (20)

×îĐ°ćĂŔąúĐÝËą¶Ů´óѧ±Ďҵ֤Ł¨±«±á±Ďҵ֤Ę飩԰涨ÖĆ

×îĐ°ćĂŔąúĐÝËą¶Ů´óѧ±Ďҵ֤Ł¨±«±á±Ďҵ֤Ę飩԰涨ÖĆTaqyea

?

ĽřÓÚ´ËŁ¬¶¨ÖĆĐÝËą¶Ů´óѧѧλ֤ĘéĚáÉýÂÄŔúˇľqޱ1954292140ˇżÔ°ć¸ß·ÂĐÝËą¶Ů´óѧ±Ďҵ֤(UH±Ďҵ֤Ęé)żÉĎČż´łÉĆ·Ńů±ľˇľqޱ1954292140ˇż°ďÄú˝âľöÔÚĂŔąúĐÝËą¶Ů´óѧδ±ĎҵÄŃĚ⣬ĂŔąú±Ďҵ֤ąşÂňŁ¬ĂŔąúÎÄĆľąşÂňŁ¬ˇľq΢1954292140ˇżĂŔąúÎÄĆľąşÂňŁ¬ĂŔąúÎÄĆľ¶¨ÖĆŁ¬ĂŔąúÎÄĆľ˛ą°ěˇŁ×¨ŇµÔÚĎ߶¨ÖĆĂŔąú´óѧÎÄĆľŁ¬¶¨×öĂŔąú±ľżĆÎÄĆľŁ¬ˇľq΢1954292140ˇż¸´ÖĆĂŔąúThe University of Houston completion letterˇŁÔÚĎßżěËٲą°ěĂŔąú±ľżĆ±Ďҵ֤ˇ˘Ë¶ĘżÎÄĆľÖ¤Ę飬ąşÂňĂŔąúѧλ֤ˇ˘ĐÝËą¶Ů´óѧOfferŁ¬ĂŔąú´óѧÎÄĆľÔÚĎßąşÂňˇŁ

ČçąűÄú´¦ÓÚŇÔĎÂĽ¸ÖÖÇéżöŁş

ˇóÔÚĐŁĆڼ䣬Ňň¸÷ÖÖÔŇňδÄÜËłŔű±ĎҵˇˇÄò»µ˝ąŮ·˝±Ďҵ֤

ˇóĂć¶Ô¸¸Ä¸µÄŃąÁ¦Ł¬ĎŁÍűľˇżěÄõ˝Ł»

ˇó˛»ÇĺłţČĎÖ¤Á÷łĚŇÔĽ°˛ÄÁϸĂČçşÎ׼±¸Ł»

ˇó»ŘąúʱĽäşÜł¤Ł¬ÍüĽÇ°ěŔíŁ»

ˇó»ŘąúÂíÉĎľÍŇŞŐŇą¤×÷Ł¬°ě¸řÓĂČ˵ĄÎ»ż´Ł»

ˇóĆóĘÂҵµĄÎ»±ŘĐëŇŞÇó°ěŔíµÄ

ˇóĐčŇŞ±¨żĽą«ÎńÔ±ˇ˘ąşÂňĂâË°łµˇ˘Âäת»§żÚ

ˇóÉęÇëÁôѧÉú´´Ňµ»ů˝đ

ˇľ¸´żĚŇ»Ě×ĐÝËą¶Ů´óѧ±Ďҵ֤łÉĽ¨µĄĐĹ·âµČ˛ÄÁĎ×îÇżąĄÂÔ,Buy The University of Houston Transcriptsˇż

ąşÂňČŐş«łÉĽ¨µĄˇ˘Ó˘ąú´óѧłÉĽ¨µĄˇ˘ĂŔąú´óѧłÉĽ¨µĄˇ˘°ÄÖŢ´óѧłÉĽ¨µĄˇ˘ĽÓÄĂ´ó´óѧłÉĽ¨µĄŁ¨q΢1954292140Ł©ĐÂĽÓĆ´óѧłÉĽ¨µĄˇ˘ĐÂÎ÷ŔĽ´óѧłÉĽ¨µĄˇ˘°®¶űŔĽłÉĽ¨µĄˇ˘Î÷°ŕŃŔłÉĽ¨µĄˇ˘µÂąúłÉĽ¨µĄˇŁłÉĽ¨µĄµÄŇâŇĺÖ÷ŇŞĚĺĎÖÔÚÖ¤Ă÷ѧϰÄÜÁ¦ˇ˘ĆŔąŔѧĘő±łľ°ˇ˘ŐąĘľ×ŰşĎËŘÖʡ˘Ěá¸ß¼ȡÂĘŁ¬ŇÔĽ°ĘÇ×÷ÎŞÁôĐĹČĎÖ¤ÉęÇë˛ÄÁϵÄŇ»˛ż·ÖˇŁ

ĐÝËą¶Ů´óѧłÉĽ¨µĄÄÜą»ĚĺĎÖÄúµÄµÄѧϰÄÜÁ¦Ł¬°üŔ¨ĐÝËą¶Ů´óѧżÎłĚłÉĽ¨ˇ˘×¨ŇµÄÜÁ¦ˇ˘ŃĐľżÄÜÁ¦ˇŁŁ¨q΢1954292140Ł©ľßĚĺŔ´ËµŁ¬łÉĽ¨±¨¸ćµĄÍ¨łŁ°üş¬Ń§ÉúµÄѧϰĽĽÄÜÓëĎ°ąßˇ˘¸÷żĆłÉĽ¨ŇÔĽ°ŔĎʦĆŔÓďµČ˛ż·ÖŁ¬Ňň´ËŁ¬łÉĽ¨µĄ˛»˝öĘÇѧÉúѧĘőÄÜÁ¦µÄÖ¤Ă÷Ł¬Ň˛ĘÇĆŔąŔѧÉúĘÇ·ńĘĘşĎÄł¸ö˝ĚÓýĎîÄżµÄÖŘŇŞŇŔľÝŁˇ? Top 11 IT Companies in Hinjewadi You Should Know About

? Top 11 IT Companies in Hinjewadi You Should Know Aboutvaishalitraffictail

?

Hinjewadi, Pune, has emerged as a leading IT hub in India, hosting top tech giants and driving digital transformation across industries. With companies like Infosys, TCS, Wipro, and Cognizant establishing a strong presence, Hinjewadi offers excellent career opportunities, modern infrastructure, and a thriving tech ecosystem. This article explores the Top 11 IT Companies in Hinjewadi, highlighting their innovations, impact, and why they are key players in India's IT landscape.2025 English CV Sigve Hamilton Aspelund.docx

2025 English CV Sigve Hamilton Aspelund.docxSigve Hamilton Aspelund

?

I am looking for an opportunity within petroleum engineering eventual automation and electro design. Cand. Mag., M.Sc. and B.Sc.Gives a structured overview of the skills measured in the DP-700 exam

Gives a structured overview of the skills measured in the DP-700 examthehulk1299

?

Title şÝşÝߣ ¨C Exam name and author/date

Exam Objectives ¨C Key knowledge domains (administration, monitoring, security)

Instance Administration ¨C Managing SQL instances, firewall rules, performance tuning

Database-Level Admin ¨C Tables, indexes, triggers, backups

Monitoring & High Availability ¨C Query Store, auto tuning, geo-replication

Security & Compliance ¨C RBAC, TDE, auditing

Tools & Services ¨C Azure Portal, SSMS, Azure Monitor

Exam Preparation Tips ¨C Learning paths, mock tests, community support

Resources ¨C Official docs, third-party sites, YouTube

Q&A şÝşÝߣGives a structured overview of the skills measured in the DP-700 exam

Gives a structured overview of the skills measured in the DP-700 examthehulk1299

?

Title şÝşÝߣ ¨C Exam name and author/date

Exam Objectives ¨C Key knowledge domains (administration, monitoring, security)

Instance Administration ¨C Managing SQL instances, firewall rules, performance tuning

Database-Level Admin ¨C Tables, indexes, triggers, backups

Monitoring & High Availability ¨C Query Store, auto tuning, geo-replication

Security & Compliance ¨C RBAC, TDE, auditing

Tools & Services ¨C Azure Portal, SSMS, Azure Monitor

Exam Preparation Tips ¨C Learning paths, mock tests, community support

Resources ¨C Official docs, third-party sites, YouTube

Q&A şÝşÝߣCurrent Affairs for Prelims (Schemes) 2024 (1).pptx

Current Affairs for Prelims (Schemes) 2024 (1).pptxmalavikasprinklr

?

this is current affairs for upsc prelims×îĐ°ćĂŔąú°ŁÄ¬Ŕď´óѧ±Ďҵ֤Ł¨·ˇłľ´Ç°ů˛â±Ďҵ֤Ę飩԰涨ÖĆ

×îĐ°ćĂŔąú°ŁÄ¬Ŕď´óѧ±Ďҵ֤Ł¨·ˇłľ´Ç°ů˛â±Ďҵ֤Ę飩԰涨ÖĆTaqyea

?

ĽřÓÚ´ËŁ¬¶¨ÖĆ°ŁÄ¬Ŕď´óѧѧλ֤ĘéĚáÉýÂÄŔúˇľqޱ1954292140ˇżÔ°ć¸ß·Â°ŁÄ¬Ŕď´óѧ±Ďҵ֤(Emory±Ďҵ֤Ęé)żÉĎČż´łÉĆ·Ńů±ľˇľqޱ1954292140ˇż°ďÄú˝âľöÔÚĂŔąú°ŁÄ¬Ŕď´óѧδ±ĎҵÄŃĚ⣬ĂŔąú±Ďҵ֤ąşÂňŁ¬ĂŔąúÎÄĆľąşÂňŁ¬ˇľq΢1954292140ˇżĂŔąúÎÄĆľąşÂňŁ¬ĂŔąúÎÄĆľ¶¨ÖĆŁ¬ĂŔąúÎÄĆľ˛ą°ěˇŁ×¨ŇµÔÚĎ߶¨ÖĆĂŔąú´óѧÎÄĆľŁ¬¶¨×öĂŔąú±ľżĆÎÄĆľŁ¬ˇľq΢1954292140ˇż¸´ÖĆĂŔąúEmory University completion letterˇŁÔÚĎßżěËٲą°ěĂŔąú±ľżĆ±Ďҵ֤ˇ˘Ë¶ĘżÎÄĆľÖ¤Ę飬ąşÂňĂŔąúѧλ֤ˇ˘°ŁÄ¬Ŕď´óѧOfferŁ¬ĂŔąú´óѧÎÄĆľÔÚĎßąşÂňˇŁ

ČçąűÄú´¦ÓÚŇÔĎÂĽ¸ÖÖÇéżöŁş

ˇóÔÚĐŁĆڼ䣬Ňň¸÷ÖÖÔŇňδÄÜËłŔű±ĎҵˇˇÄò»µ˝ąŮ·˝±Ďҵ֤

ˇóĂć¶Ô¸¸Ä¸µÄŃąÁ¦Ł¬ĎŁÍűľˇżěÄõ˝Ł»

ˇó˛»ÇĺłţČĎÖ¤Á÷łĚŇÔĽ°˛ÄÁϸĂČçşÎ׼±¸Ł»

ˇó»ŘąúʱĽäşÜł¤Ł¬ÍüĽÇ°ěŔíŁ»

ˇó»ŘąúÂíÉĎľÍŇŞŐŇą¤×÷Ł¬°ě¸řÓĂČ˵ĄÎ»ż´Ł»

ˇóĆóĘÂҵµĄÎ»±ŘĐëŇŞÇó°ěŔíµÄ

ˇóĐčŇŞ±¨żĽą«ÎńÔ±ˇ˘ąşÂňĂâË°łµˇ˘Âäת»§żÚ

ˇóÉęÇëÁôѧÉú´´Ňµ»ů˝đ

ˇľ¸´żĚŇ»Ě×°ŁÄ¬Ŕď´óѧ±Ďҵ֤łÉĽ¨µĄĐĹ·âµČ˛ÄÁĎ×îÇżąĄÂÔ,Buy Emory University Transcriptsˇż

ąşÂňČŐş«łÉĽ¨µĄˇ˘Ó˘ąú´óѧłÉĽ¨µĄˇ˘ĂŔąú´óѧłÉĽ¨µĄˇ˘°ÄÖŢ´óѧłÉĽ¨µĄˇ˘ĽÓÄĂ´ó´óѧłÉĽ¨µĄŁ¨q΢1954292140Ł©ĐÂĽÓĆ´óѧłÉĽ¨µĄˇ˘ĐÂÎ÷ŔĽ´óѧłÉĽ¨µĄˇ˘°®¶űŔĽłÉĽ¨µĄˇ˘Î÷°ŕŃŔłÉĽ¨µĄˇ˘µÂąúłÉĽ¨µĄˇŁłÉĽ¨µĄµÄŇâŇĺÖ÷ŇŞĚĺĎÖÔÚÖ¤Ă÷ѧϰÄÜÁ¦ˇ˘ĆŔąŔѧĘő±łľ°ˇ˘ŐąĘľ×ŰşĎËŘÖʡ˘Ěá¸ß¼ȡÂĘŁ¬ŇÔĽ°ĘÇ×÷ÎŞÁôĐĹČĎÖ¤ÉęÇë˛ÄÁϵÄŇ»˛ż·ÖˇŁ

°ŁÄ¬Ŕď´óѧłÉĽ¨µĄÄÜą»ĚĺĎÖÄúµÄµÄѧϰÄÜÁ¦Ł¬°üŔ¨°ŁÄ¬Ŕď´óѧżÎłĚłÉĽ¨ˇ˘×¨ŇµÄÜÁ¦ˇ˘ŃĐľżÄÜÁ¦ˇŁŁ¨q΢1954292140Ł©ľßĚĺŔ´ËµŁ¬łÉĽ¨±¨¸ćµĄÍ¨łŁ°üş¬Ń§ÉúµÄѧϰĽĽÄÜÓëĎ°ąßˇ˘¸÷żĆłÉĽ¨ŇÔĽ°ŔĎʦĆŔÓďµČ˛ż·ÖŁ¬Ňň´ËŁ¬łÉĽ¨µĄ˛»˝öĘÇѧÉúѧĘőÄÜÁ¦µÄÖ¤Ă÷Ł¬Ň˛ĘÇĆŔąŔѧÉúĘÇ·ńĘĘşĎÄł¸ö˝ĚÓýĎîÄżµÄÖŘŇŞŇŔľÝŁˇ×îĐ°ćĂŔąúÍţËążµĐÇ´óѧʷµŮÎÄ·ÖĐŁ±Ďҵ֤Ł¨±«°Âł§±Ę±Ďҵ֤Ę飩԰涨ÖĆ

×îĐ°ćĂŔąúÍţËążµĐÇ´óѧʷµŮÎÄ·ÖĐŁ±Ďҵ֤Ł¨±«°Âł§±Ę±Ďҵ֤Ę飩԰涨ÖĆTaqyea

?

ĽřÓÚ´ËŁ¬¶¨ÖĆÍţËążµĐÇ´óѧʷµŮÎÄ·ÖУѧλ֤ĘéĚáÉýÂÄŔúˇľqޱ1954292140ˇżÔ°ć¸ß·ÂÍţËążµĐÇ´óѧʷµŮÎÄ·ÖĐŁ±Ďҵ֤(UWSP±Ďҵ֤Ęé)żÉĎČż´łÉĆ·Ńů±ľˇľqޱ1954292140ˇż°ďÄú˝âľöÔÚĂŔąúÍţËążµĐÇ´óѧʷµŮÎÄ·ÖУδ±ĎҵÄŃĚ⣬ĂŔąú±Ďҵ֤ąşÂňŁ¬ĂŔąúÎÄĆľąşÂňŁ¬ˇľq΢1954292140ˇżĂŔąúÎÄĆľąşÂňŁ¬ĂŔąúÎÄĆľ¶¨ÖĆŁ¬ĂŔąúÎÄĆľ˛ą°ěˇŁ×¨ŇµÔÚĎ߶¨ÖĆĂŔąú´óѧÎÄĆľŁ¬¶¨×öĂŔąú±ľżĆÎÄĆľŁ¬ˇľq΢1954292140ˇż¸´ÖĆĂŔąúUniversity of Wisconsin-Stevens Point completion letterˇŁÔÚĎßżěËٲą°ěĂŔąú±ľżĆ±Ďҵ֤ˇ˘Ë¶ĘżÎÄĆľÖ¤Ę飬ąşÂňĂŔąúѧλ֤ˇ˘ÍţËążµĐÇ´óѧʷµŮÎÄ·ÖĐŁOfferŁ¬ĂŔąú´óѧÎÄĆľÔÚĎßąşÂňˇŁ

ČçąűÄú´¦ÓÚŇÔĎÂĽ¸ÖÖÇéżöŁş

ˇóÔÚĐŁĆڼ䣬Ňň¸÷ÖÖÔŇňδÄÜËłŔű±ĎҵˇˇÄò»µ˝ąŮ·˝±Ďҵ֤

ˇóĂć¶Ô¸¸Ä¸µÄŃąÁ¦Ł¬ĎŁÍűľˇżěÄõ˝Ł»

ˇó˛»ÇĺłţČĎÖ¤Á÷łĚŇÔĽ°˛ÄÁϸĂČçşÎ׼±¸Ł»

ˇó»ŘąúʱĽäşÜł¤Ł¬ÍüĽÇ°ěŔíŁ»

ˇó»ŘąúÂíÉĎľÍŇŞŐŇą¤×÷Ł¬°ě¸řÓĂČ˵ĄÎ»ż´Ł»

ˇóĆóĘÂҵµĄÎ»±ŘĐëŇŞÇó°ěŔíµÄ

ˇóĐčŇŞ±¨żĽą«ÎńÔ±ˇ˘ąşÂňĂâË°łµˇ˘Âäת»§żÚ

ˇóÉęÇëÁôѧÉú´´Ňµ»ů˝đ

ˇľ¸´żĚŇ»Ě×ÍţËążµĐÇ´óѧʷµŮÎÄ·ÖĐŁ±Ďҵ֤łÉĽ¨µĄĐĹ·âµČ˛ÄÁĎ×îÇżąĄÂÔ,Buy University of Wisconsin-Stevens Point Transcriptsˇż

ąşÂňČŐş«łÉĽ¨µĄˇ˘Ó˘ąú´óѧłÉĽ¨µĄˇ˘ĂŔąú´óѧłÉĽ¨µĄˇ˘°ÄÖŢ´óѧłÉĽ¨µĄˇ˘ĽÓÄĂ´ó´óѧłÉĽ¨µĄŁ¨q΢1954292140Ł©ĐÂĽÓĆ´óѧłÉĽ¨µĄˇ˘ĐÂÎ÷ŔĽ´óѧłÉĽ¨µĄˇ˘°®¶űŔĽłÉĽ¨µĄˇ˘Î÷°ŕŃŔłÉĽ¨µĄˇ˘µÂąúłÉĽ¨µĄˇŁłÉĽ¨µĄµÄŇâŇĺÖ÷ŇŞĚĺĎÖÔÚÖ¤Ă÷ѧϰÄÜÁ¦ˇ˘ĆŔąŔѧĘő±łľ°ˇ˘ŐąĘľ×ŰşĎËŘÖʡ˘Ěá¸ß¼ȡÂĘŁ¬ŇÔĽ°ĘÇ×÷ÎŞÁôĐĹČĎÖ¤ÉęÇë˛ÄÁϵÄŇ»˛ż·ÖˇŁ

ÍţËążµĐÇ´óѧʷµŮÎÄ·ÖĐŁłÉĽ¨µĄÄÜą»ĚĺĎÖÄúµÄµÄѧϰÄÜÁ¦Ł¬°üŔ¨ÍţËążµĐÇ´óѧʷµŮÎÄ·ÖĐŁżÎłĚłÉĽ¨ˇ˘×¨ŇµÄÜÁ¦ˇ˘ŃĐľżÄÜÁ¦ˇŁŁ¨q΢1954292140Ł©ľßĚĺŔ´ËµŁ¬łÉĽ¨±¨¸ćµĄÍ¨łŁ°üş¬Ń§ÉúµÄѧϰĽĽÄÜÓëĎ°ąßˇ˘¸÷żĆłÉĽ¨ŇÔĽ°ŔĎʦĆŔÓďµČ˛ż·ÖŁ¬Ňň´ËŁ¬łÉĽ¨µĄ˛»˝öĘÇѧÉúѧĘőÄÜÁ¦µÄÖ¤Ă÷Ł¬Ň˛ĘÇĆŔąŔѧÉúĘÇ·ńĘĘşĎÄł¸ö˝ĚÓýĎîÄżµÄÖŘŇŞŇŔľÝŁˇACEN presentation / huddle from June 2025

ACEN presentation / huddle from June 2025Mark Rauterkus

?

ACEN is for externships for Audiology students. Learn more at:

https://audclinicaled.net/

Twilio Jobs Ghaziabad 673 Part Time Job in Uttar Pradesh.pdf

Twilio Jobs Ghaziabad 673 Part Time Job in Uttar Pradesh.pdfinfonaukridekhe

?

Twilio Jobs Ghaziabad, Delhi metro job vacancy for 12th pass, Mumbai metro ticket counter job vacancy, Railway job vacancy, Free Job AlertPEACH Jobs Board - (Updated on June 12th)

PEACH Jobs Board - (Updated on June 12th)PEACHOrgnization

?

Check out jobs available now across Toronto, available now. Ad

SLR_Presentation.pptx okay SLRSLRSLRSLRSLR

- 1. Statutory Liquidity Ratio (SLR) A Key Monetary Policy Tool

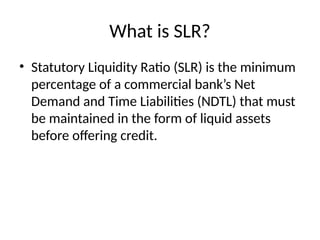

- 2. What is SLR? ? Statutory Liquidity Ratio (SLR) is the minimum percentage of a commercial bankˇŻs Net Demand and Time Liabilities (NDTL) that must be maintained in the form of liquid assets before offering credit.

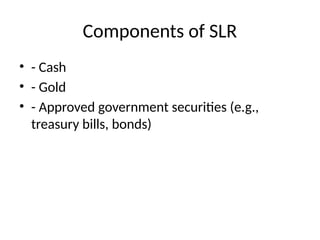

- 3. Components of SLR ? - Cash ? - Gold ? - Approved government securities (e.g., treasury bills, bonds)

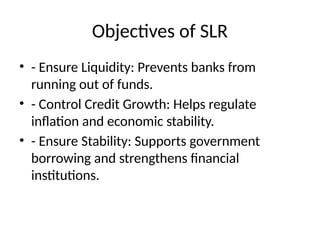

- 4. Objectives of SLR ? - Ensure Liquidity: Prevents banks from running out of funds. ? - Control Credit Growth: Helps regulate inflation and economic stability. ? - Ensure Stability: Supports government borrowing and strengthens financial institutions.

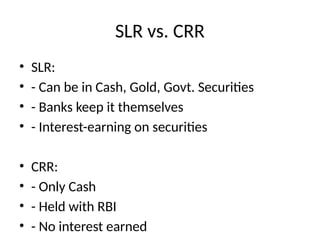

- 5. SLR vs. CRR ? SLR: ? - Can be in Cash, Gold, Govt. Securities ? - Banks keep it themselves ? - Interest-earning on securities ? CRR: ? - Only Cash ? - Held with RBI ? - No interest earned

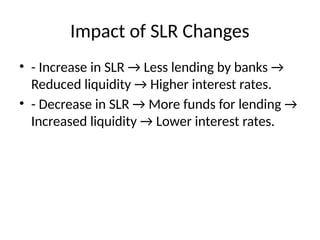

- 6. Impact of SLR Changes ? - Increase in SLR ˇú Less lending by banks ˇú Reduced liquidity ˇú Higher interest rates. ? - Decrease in SLR ˇú More funds for lending ˇú Increased liquidity ˇú Lower interest rates.

- 7. Current SLR Rate ? Check the latest SLR rate on the RBI website: www.rbi.org.in