Stochastic Differential Equations: Application to Pension Funds under Adverse Selection

?

1 like?526 views

Shown in #MCDE2014 Magno Coloquio de Doctorantes en Econom©¬a 2014, in Mexico City, November 2014. Rights Reserved to Escuela Superior de Econom©¬a, Instituto Polit©”cnico Nacional

![rk(x, ?1,?2) :=

Z

U2

Z

U1

rk(x, u1, u2)?1(du1|x)?2(du2|x)

J`T

(x, ?1,?2) := E?1,?2

x [

Z T

0

rk(x(t),?1,?2)dt]

Jk(x, ?1,?2) := lim

T!1

sup

1

T

Jk

T (x, ?1,?2)](https://image.slidesharecdn.com/ssddee-141109184628-conversion-gate02/85/Stochastic-Differential-Equations-Application-to-Pension-Funds-under-Adverse-Selection-10-320.jpg)

![dx(t) = (”╠x(t) + u1(t) u2(t))dt + dW(t)

x(0) = x

r1(x, u1, u2) = x

r2(x, u1, u2) = u2

Contribution Strategy

u1, u2 2 [0, d]

Withdrawal Strategy](https://image.slidesharecdn.com/ssddee-141109184628-conversion-gate02/85/Stochastic-Differential-Equations-Application-to-Pension-Funds-under-Adverse-Selection-16-320.jpg)

![J1= sup

2P(U1)

?

x + (”╠x + !(x) ?2(Īż|x))h01(x) +

1

2

#2h00 1 (x)

= sup

[!(x)h01(x)] + [x(1 + ”╠) ?2(Īż|x)]h01(x) +

2P(U1)

1

2

#2h00 1 (x)

J2= sup

2P(U2)

?

(x) + (”╠x + ?(Īż|x) (x))h02(x) +

1

2

#2h00 2 (x)

= sup

[ (x)(1 h02(x))] + (”╠x + ?1(Īż|x))h02(x) +

2P(U2)

1

2

#2h00 2 (x)](https://image.slidesharecdn.com/ssddee-141109184628-conversion-gate02/85/Stochastic-Differential-Equations-Application-to-Pension-Funds-under-Adverse-Selection-17-320.jpg)

Stochastic Differential Equations: Application to Pension Funds under Adverse Selection

- 1. Stochastic Differential Games: An Application to Pension Funds under Adverse Selection Mario A. Garc©¬a-Meza Jos©” Daniel L©«pez-Barrientos Magno Coloquio de Doctorantes en Econom©¬a

- 2. Overview Adverse Selection Stochastic Differential Games An Application to Pension Funds: Separating Equilibrium Conclusions

- 6. dx(t) = b(x(t), u1(t), u2(t))dt + (x(t))dW(t)

- 7. 8i6= j, xi 2 Si : fi(x?i , x?j ) $ fi(xi, x?j )

- 9. Lu1,u2?(x) := Xn i=1 bi(x, u1, u2) @? @xi (x) + 1 2 Xn i,j aij(x) @2? @xi@xj (x) dx(t) = b(x(t), u1(t), u2(t))dt + (x(t))dW(t)

- 10. rk(x, ?1,?2) := Z U2 Z U1 rk(x, u1, u2)?1(du1|x)?2(du2|x) J`T (x, ?1,?2) := E?1,?2 x [ Z T 0 rk(x(t),?1,?2)dt] Jk(x, ?1,?2) := lim T!1 sup 1 T Jk T (x, ?1,?2)

- 11. J1(??1,??2) ! J1(?1,??2) for every ?1 2 ?1 J2(??1,??2) ! J2(??1,?2) for every ?2 2 ?2

- 12. Optimal Response ?1 = Ī▒I knowĪ▒ ?1 = silence ?1 = Ī▒Who doesnĪ»t?Ī▒ ?1 = Ī▒I love you tooĪ▒ ?1 = Ī▒Thank youĪ▒ ?1 = Ī▒I love me tooĪ▒ ?2 = Ī▒I love youĪ▒

- 13. Optimal Response J1(??1,?2) = sup ?12?1 J1(?1,?2) J2(?1,??2) = sup ?22?2 J2(?1,?2)

- 14. Optimal equations of Average Payoff J1 = r1(x, ??1,?2) + L??1,?2 h1(x) = sup 2?U 1{r1(x, , ?2) + L,?2 h1(x)} J2 = r2(x, ??1,??2) + L??1,?2?h2(x) = sup 2?U 2{r2(x, ??1, ) + L??1, h2(x)}

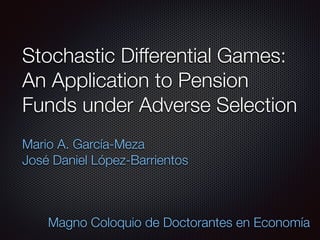

- 16. dx(t) = (”╠x(t) + u1(t) u2(t))dt + dW(t) x(0) = x r1(x, u1, u2) = x r2(x, u1, u2) = u2 Contribution Strategy u1, u2 2 [0, d] Withdrawal Strategy

- 17. J1= sup 2P(U1) ? x + (”╠x + !(x) ?2(Īż|x))h01(x) + 1 2 #2h00 1 (x) = sup [!(x)h01(x)] + [x(1 + ”╠) ?2(Īż|x)]h01(x) + 2P(U1) 1 2 #2h00 1 (x) J2= sup 2P(U2) ? (x) + (”╠x + ?(Īż|x) (x))h02(x) + 1 2 #2h00 2 (x) = sup [ (x)(1 h02(x))] + (”╠x + ?1(Īż|x))h02(x) + 2P(U2) 1 2 #2h00 2 (x)

- 18. h01(x) 1 1 1 0 0 h02(x) (0(x), d(x)) (0(x), u(x)) (0(x), 0(x)) (d(x), d(x)) (d(x), u(x)) (d(x), 0(x))

- 19. h01(x) 1 1 1 0 Contribute Nothing, Withdraw all possible Contribute nothing,withdraw arbitrary amount Contribute Living off my nothing, withdraw rents nothing 0 Contribute all possible,withdraw all possible Contribute all possible,withdraw arbitrary amount Contribute all possible,withdraw nothing h02(x) Abandon ship! New Money Buy and Hold

- 21. Conclusions An SDG with additive structure and average payoff can yield Nash equilibria with deterministic strategies that construct a separating equilibrium for pensions funds, thus solving the adverse selection problem This work can be extended still more by adding for example (1) The control set from fund manager(s), (2) The agent has to optimize through the selection of an optimal portfolio

- 22. References Pension Funds and Adverse Selection Akerlof (1970). The Market for Ī░lemonsĪ▒: Quality uncertainty and the market mechanisms. The quarterly journal of economics, 488-500. Blake, D. (1999). Annuity markets: Problems and Solutions. Geneva Papers on Risk and Insurance. Issues and practice, 358-375. Model for Stochastic Differential Game Escobedo-Trujillo, B. A., Lopez-Barrientos, J.D. (2014) Nonzero- Sum stochastic Differential Games with Additive structure and average payoff. Journal of Optimization Theory and Applications.