Time sereies forecasting(ARCH/GARCH)

?Download as PPTX, PDF?

2 likes?477 views

1) This document discusses time series forecasting of the 3-month US Treasury rate from 1960-2011. 2) Descriptive statistics show the data is positively skewed and not normally distributed. The time series plot shows an increasing trend over time with sudden peaks and decreases. 3) Autocorrelation decreases with lag, and the first lag is significant in the partial autocorrelation function, indicating the series is not stationary. The augmented Dickey-Fuller test confirms the series is stationary after first differencing.

Time sereies forecasting(ARCH/GARCH)

- 1. TIME SEREIES FORECASTING US Treasury rate A.W.D. Udaya Shalika 158888L

- 2. DATA SOURCE ? Tbill ©C 3-month US Treasury rate (source: Board of Governors of the Federal Reserve) ? monthly data from January 1960-December 2011.

- 3. Descriptive Statistics ? varies between 226 (min) and 1813.5(max) with the mean of 520.8. The median value is 387.05 and data seems positively skewed (Skewness 2.22) ? JB(JB=629.8) test and p value is significant(p = 0.00) .Thus it confirms that data is not normally distributed. 0 10 20 30 40 50 60 70 80 0 2 4 6 8 10 12 14 16 Series: TBILL Sample 1960M01 2011M12 Observations 624 Mean 5.127516 Median 4.960000 Maximum 16.30000 Minimum 0.010000 Std. Dev. 2.957858 Skewness 0.808674 Kurtosis 4.365448 Jarque-Bera 116.4868 Probability 0.000000

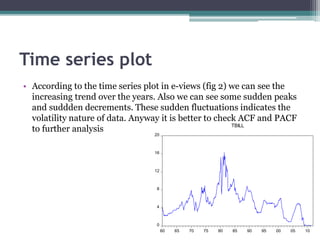

- 4. Time series plot ? According to the time series plot in e-views (fig 2) we can see the increasing trend over the years. Also we can see some sudden peaks and suddden decrements. These sudden fluctuations indicates the volatility nature of data. Anyway it is better to check ACF and PACF to further analysis 0 4 8 12 16 20 60 65 70 75 80 85 90 95 00 05 10 TBILL

- 5. Correlagram According to the ACF we can see that auto correlation decreases with the lag increases In PACF only first lag is significant. By looking at ACF we can simply say that original series is not stationary. Anyway we can confirm further by using Dicky Fuller test as well to check the stationary nature in original series

- 6. Unit Root Test The augmented Dickey- Fuller test confirms that null hypothesis fails that ? not equal to 0. Thus model will be stationary According to the above output of DF test for 1st difference confirms that 1st difference of the series is stationary at 5% of level (p=0.00). Original Series First Difference Series

- 7. Mean Model ccording to the first difference series ACF we can see the 1st lag ACF is significance and others get decaying. In PACF also can see the 1st lag and 2nd lag PACF is significance and others get decaying Based on this we can try MA or AR model for the first difference series

- 9. Testing for Ī«ARCH effectsĪ» -4 -2 0 2 4 -6 -4 -2 0 2 4 65 70 75 80 85 90 95 00 05 10 Residual Actual Fitted When we plotted the residuals we can see that clustering volatility, which means large fluctuations tend to be followed by large fluctuations, of either sign, and small fluctuations tend to be followed by small fluctuations. Further we can confirm this by using squared residuals or ARCH LM test.

- 10. Testing for Ī«ARCH effectsĪ»contd. ACF of Squared residuals of confrims that availability of ARCH effect. All tested lags seems significant and null hypothesis rejected. (H0- first m lags of ACF of squared residuals series are equal to zero vs H1- first m lags of ACF of squared residuals series are not equal to zero). the Q statistics of tested lags are significant, which confirms serial correlation in the residuals.

- 11. Testing for Ī«ARCH effectsĪ»contd Since TR? =67.76 > ?1,0.05 2 = 3.8415 and p=0.00 we reject the null hypothesis (H0- No ARCH Effect vs H1- There is ARCH effect) and conclude that there is statistically significant ARCH effects in the errors of AR(1) model. Therefore, we have to model the exchange rate series by using ARCH/GARCH type models

- 12. Model Selection ? An available method is to observe the PACF of squared returns or squared residuals based on the mean model. If PACF cuts off at lag value q, we can guess the ARCHŻ©qŻ®model is appropriate. Then we can use Garch function to check the AICs of the ARCH (q), ARCH (q-1),ARCH (q+1)models. If the AIC of the ARCH (q) model is the smallest, then the model can be used to fit the data.

- 13. ARCH(2)

- 14. GARCH(1,2)

- 15. 2016/10/16