Trust Income Tax Return: Taxation for Trust | ITR-7 - Tax Craft Hub

A Trust Income Tax Return is a tax filing that must be submitted by a trust or estate to report its income, deductions, and distributions to beneficiaries. Trusts, which are legal entities holding assets for the benefit of certain individuals or organizations, are required to pay income taxes on the income generated by these assets. The trust income tax return, typically filed using IRS Form 1041 in the United States, details the income earned by the trust, such as interest, dividends, and capital gains, and allocates taxable income to either the trust or its beneficiaries, depending on the trust's structure and terms. This ensures proper tax compliance and allocation of tax liability between the trust and its beneficiaries. For More Information Visit Us https://blogs.24efiling.com/trust-income-tax-return/

More Related Content

Similar to Trust Income Tax Return: Taxation for Trust | ITR-7 - Tax Craft Hub (20)

Recently uploaded (20)

Trust Income Tax Return: Taxation for Trust | ITR-7 - Tax Craft Hub

- 1. Trust Income Tax Return: Taxation for Trust | ITR-7 Understanding how to file a Trust income tax return can seem complex. Whether you manage a charitable trust or a business trust, this information will equip you to navigate the requirements and deadlines associated with income tax returns in India. In this article, we look at similar benefits and the procedure for filing a Trust income tax return. What is a Charitable trust? A charitable trust is a type of entity formed to give the public religious or philanthropic installations. Trusts established for charitable or religious purposes and not engaged in commercial activities are eligible for tax benefits as per the Income Tax Act. In other words, a charitable trust is a legal tool for donating money or assets to public causes you care about. These irrevocable structures involve a donor who contributes the initial wealth, trustees who manage it, and beneficiaries (charities) who receive the funds. Donors can enjoy tax benefits, charities gain a steady funding stream, and assets can grow over time for greater impact. There are various types of charitable trusts, like those providing income to the donor first (remainder trust) or to charity first (lead trust). A charitable trust allows for thoughtful philanthropy with potential tax advantages and responsible management of your donation. What is ITR-7 in Income Tax? ITR-7 is an Income Tax Return form used by persons including companies, firms, and Associations of Persons (AOP) who are needed to furnish a return under section 139(4A) or section 139(4B) or section 139(4C) or section 139(4D) of the Income Tax Act. It’s specifically meant for entities similar to trusts, political parties, exploration associations, and educational institutions. What documents are needed for Trust Income Tax Returns? For a charity trust income tax returns, applicable documents similar as audited fiscal statements, bills and payment account, income and expenditure account, balance sheet, details of donations entered, application instruments, and any other supporting documents related to the trust’s income and charges should be submitted along with the return. It’s important to maintain proper records and ensure compliance with the regulations applicable to charitable trusts. How to file a trust Income Tax Return? The charitable trust income tax return must be filed using the ITR-5 return form or ITR-7. In case the Trust is needed to file an income tax return due to taxable income being more than the introductory exemption limit, also ITR 5 can be filed. In case the Trust is needed to file income tax return mandatorily under sections 139(4A) or 139(4B) or 139(4C) or 139(4D) or139(4E) or 139(4F) of the Income Tax Act, also ITR-7 must be filed. All trusts must file income tax returns. In case the Trust needs to get its accounts checked, also the income tax return must be filed along with the digital hand of the chartered accountant who’s responsible for carrying out the inspection.

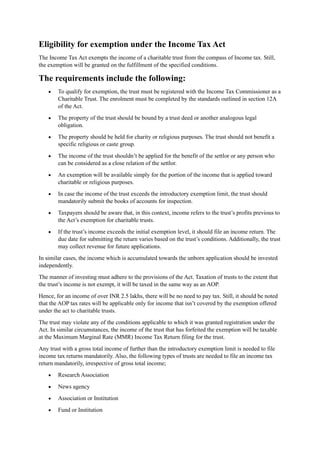

- 2. Eligibility for exemption under the Income Tax Act The Income Tax Act exempts the income of a charitable trust from the compass of Income tax. Still, the exemption will be granted on the fulfillment of the specified conditions. The requirements include the following: • To qualify for exemption, the trust must be registered with the Income Tax Commissioner as a Charitable Trust. The enrolment must be completed by the standards outlined in section 12A of the Act. • The property of the trust should be bound by a trust deed or another analogous legal obligation. • The property should be held for charity or religious purposes. The trust should not benefit a specific religious or caste group. • The income of the trust shouldn’t be applied for the benefit of the settlor or any person who can be considered as a close relation of the settlor. • An exemption will be available simply for the portion of the income that is applied toward charitable or religious purposes. • In case the income of the trust exceeds the introductory exemption limit, the trust should mandatorily submit the books of accounts for inspection. • Taxpayers should be aware that, in this context, income refers to the trust’s profits previous to the Act’s exemption for charitable trusts. • If the trust’s income exceeds the initial exemption level, it should file an income return. The due date for submitting the return varies based on the trust’s conditions. Additionally, the trust may collect revenue for future applications. In similar cases, the income which is accumulated towards the unborn application should be invested independently. The manner of investing must adhere to the provisions of the Act. Taxation of trusts to the extent that the trust’s income is not exempt, it will be taxed in the same way as an AOP. Hence, for an income of over INR 2.5 lakhs, there will be no need to pay tax. Still, it should be noted that the AOP tax rates will be applicable only for income that isn’t covered by the exemption offered under the act to charitable trusts. The trust may violate any of the conditions applicable to which it was granted registration under the Act. In similar circumstances, the income of the trust that has forfeited the exemption will be taxable at the Maximum Marginal Rate (MMR) Income Tax Return filing for the trust. Any trust with a gross total income of further than the introductory exemption limit is needed to file income tax returns mandatorily. Also, the following types of trusts are needed to file an income tax return mandatorily, irrespective of gross total income; • Research Association • News agency • Association or Institution • Fund or Institution

- 3. • University or other Educational Institution • Collective Fund • Securitisation trust • Investor Protection Fund • Core agreement Guarantee Fund • Venture Capital Company or Venture Capital Fund • Trade Union • Authority or Body or Trust or Board or Commission • Structure debt fund What is a Business Trust? A business trust, like a traditional trust, involves a grantor setting up the trust, a trustee managing the assets, and beneficiaries receiving the profits. It’s a flexible tool for managing businesses or assets. Grantors can separate ownership and control, use it for estate planning, or even attract investors as beneficiaries. There are two main types: the Massachusetts Business Trust (acting as a separate legal entity) and the Pure Trust (where the grantor might retain some liability). Taxation can be complex, so consulting a tax advisor is recommended. Overall, a business trust offers a customizable way to manage and distribute business assets, but understanding its structure, tax implications, and suitability is key. Due date for Trust Income Tax Return filing The due date for income tax filing for trusts are as follows • September 30: If the trust is needed to get its accounts checked under the Income Tax Act or any other law. • November 30: If the trust is needed to file Form No. 3CEB. Form 3CEB is required if the trust is involved in specific types of transactions with related parties. • July 31: If the trust doesn’t need to get its accounts checked. How to file an ITR for an unrecorded trust? Unrecorded trusts are generally tested under the provisions applicable to individuals or AOPs. The trustees need to file income tax returns using the applicable ITR form grounded on the type of income earned by the trust. They must report all income, claim deductions, and pay taxes consequently. How to file an ITR for a private trust? Private trusts are usually taxed as separate entities and are needed to file ITRs using Form ITR-5 or ITR-7, depending on the vittles applicable to them. Trustees need to give details of the trust’s income, deductions claimed, and other applicable information while filing the return. Conclusion Filing a Trust income tax return doesn’t have to be a daunting task. By familiarizing yourself with the types of trusts, exemption criteria, and ITR forms (like ITR-5 and ITR-7), you can ensure your trust is

- 4. compliant with tax regulations. Remember, the due date for filing can vary depending on the specific circumstances of your trust. Consult with an expert tax advisor like 24efiling for personalized guidance on your Trust income tax return.