What is Payment Tokenization?

Tokenization enables banks, acquirers and merchants to offer more secure (mobile) payment services.

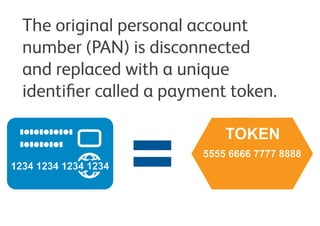

It is the process of replacing card data with alternate values.

The original personal account number (PAN) is disconnected and replaced with a unique identifier called a payment token.

The ŌĆśmappingŌĆÖ between the real PAN and the payment tokens is safely stored in the token vault.

With tokenization the original PAN information is removed from environments where data can be vulnerable.

Why tokenization?

Tokenization heavily reduces payment fraud by removing confidential consumer credit card data from the network.

The original data stays in the bankŌĆÖs control. External systems have no access to this.

Tokens are not based on cryptography and can therefore not be traced back to the original value.

How does tokenization work?

Step 1: A payment token is generated from the PAN for one time use within a specific domain such as a merchantŌĆÖs website or channel.

Tokens are sent to the token vault and stored in a PCI-compliant environment which does not allow merchants to store credit card numbers.

Step 2: Tokens are loaded on the mobile device.

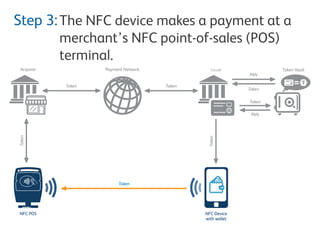

Step 3: The NFC device makes a payment at a merchantŌĆÖs NFC point-of-sales (POS) terminal.

Step 4: The POS terminal sends the token to the acquiring bank, which sends it to the issuing bank through the payment network.

Step 5: The issuer de-tokenizes the token to the real PAN and, if in order, approves the payment.

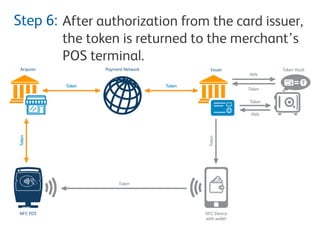

Step 6: After authorization from the card issuer, the token is returned to the merchantŌĆÖs POS terminal.

Payment tokens perform like the original PAN for returns, sales reports, marketing analysis, recurring payments etc.

20. How can I issue tokens?

In order to use tokenization, a bank or merchant should become a token service provider (TSP).

A TSP manages the entire lifecycle of payment credentials including:

1. Tokenization: replaces the PAN with a payment token.

2. De-Tokenization: converts the token back to the PAN using the token vault.

3. Token vault: establishes and maintains the payment token to PAN mapping.

4. Domain management: improves protection by defining payment tokens for specific use.

5. Clearing and settlement: ad-hoc de-tokenization during clearing and settlement process.

6. Identification and verification: ensures the original PAN is legitimately used by the token requestor.

Thinking of issuing payment tokens to e.g. secure mobile payments or secure your online sales channel? Bell ID can help: www.bellid.com ŌĆō info@bellid.com

Martin Cox ŌĆō Global Head of Sales

27. 5. Identification and verification:

Ensures the original PAN is legitimately used

by the token requestor.

28. 6. Clearing and settlement:

Ad-hoc de-tokenization during clearing

and settlement process.

29. Thinking of issuing payment tokens

to secure mobile payments or

secure your online sales channel?

Bell ID can help:

www.bellid.com

info@bellid.com

30. With over 20 years of expertise, Bell ID is considered the worldŌĆÖs leading provider of

lifecycle management solutions for tokens (e.g. smart cards, mobile NFC phones)

deployed in single and multi-application programmes.

www.bellid.com

Martin Cox

Global Head of Sales

m.cox@bellid.com