Cash flow statement

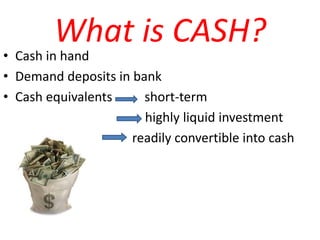

- 2. What is CASH? âĒ Cash in hand âĒ Demand deposits in bank âĒ Cash equivalents short-term highly liquid investment readily convertible into cash

- 3. CASH FLOW STATEMENT âĒ It reflects applications & sources of cash resources resulting in increase/ decrease in cash & cash equivalents.

- 6. Operating activities Deals with day to day *Inflows âĒ Cash from sales âĒ Cash received from debtors âĒ Cash received from commission and fees âĒ Royalty & other revenues business activities. *Outflows âĒ Cash purchases âĒ Payment to creditors âĒ Payment of wages âĒ Income tax âĒ Cash operating expenses

- 7. Investing activities Acquisition and disposal of long-term * Inflows âĒ Sale of fixed asset âĒ Sale of investments âĒ Interest received âĒ Dividend received assets and other investments. * Outflows âĒ Purchase of fixed assets âĒ Purchase of investments

- 8. Financing activities Relate to changes in the composition of * Inflows âĒ Issue of :shares debentures âĒ Proceeds from borrowing: long term short term capital and debt of the company. * Outflows âĒ Cash repayments for the amount borrowed âĒ Interest paid on loan/debentures âĒ Dividends paid on: equity & preference shares

- 9. Limitations of cash flow âĒ It is very difficult to define the term âcashâ. âĒ Controversies over a number of items like cheques,stamps,postal orders,etc to be included in cash or not. âĒ Prepaid and accruals recorded as increase in working capital would actually mislead to equate net income to cash flows.