More Related Content

Similar to capstruc.ppt (20)

More from KEHKASHANNIZAM (13)

Recently uploaded (20)

![ESET Internet Security Crack with License Key 2025 [Latest]](https://cdn.slidesharecdn.com/ss_thumbnails/mid-reseach-250317133026-0d208880-250318082658-2538a2bd-thumbnail.jpg?width=560&fit=bounds)

capstruc.ppt

- 1. Capital Structure and Firm Value

- 2. Does Capital Structure affect value? âĒ Empirical patterns â Across Industries â Across Firms â Across Years â Who has lower debt? âĒ High intangible assets/specialized assets âĒ High growth firms âĒ High cash flow volatility âĒ High information asymmetry âĒ Industry leaders âĒ Is capital structure managed? â If so much time is spent on capital structure then there must be some value to it (or managers/investors are irrational)

- 3. Debt and Equity Only? âĒ Typically thought of and measured this way âĒ Much more complex â Investment opportunities and strategy (needs) â Financing (sources) âĒ Cash balance âĒ Distribution: Dividend and repurchases âĒ Debt capacity âĒ Equity capacity âĒ Existing debt and equity â Other financial policies: Financial Hedging, Cash Flow Volatility, Forms of Compensation

- 4. How does capital structure affect value? âĒ To prove this we start in the âperfect worldâ â Based on the work of Miller and Modigliani â Shows that capital structure is irrelevant âĒ Value is derived from market imperfections âĒ Example: What if a firm is considering issuing debt and retiring equal amounts of equity?

- 5. Current Proposed Assets 8000 8000 Debt 0 4000 Equity 8000 4000 Interest 0.1 0.1 Share Price 20 20 Outstanding Shares 400 200

- 6. Current Recession Expected Expansion Earnings 400 1200 2000 ROA 0.05 0.15 0.25 ROE 0.05 0.15 0.25 EPS 1 3 5 Proposed Recession Expected Expansion EBI 400 1200 2000 Interest 400 400 400 Earnings 0 800 1600 ROA 0.05 0.15 0.25 ROE 0 0.2 0.4 EPS 0 4 8

- 7. Position #1: Buy 100 shares of the levered firm ($20*100=$2,000 Initial Investment) Recession Expected Expansion Earnings 0 400 800 Position #2: Buy 200 shares of the unlevered firm and borrow $2000 (($20*200)-$2,000=$2,000 Initial investment). Recession Expected Expansion Earnings 200 600 1000 Interest 200 200 200 Net Earnings 0 400 800

- 8. Capital Structure is Irrelevant âĒ Miller and Modigliani assume perfect capital markets âĒ Proposition #1: The market value of any firm is independent of its capital structure.

- 9. Firm Value: Perfect Capital Markets 50 70 90 110 130 150 170 190 0% 25% 50% 75% 100% D/E Value V(Unlevered)

- 10. Market Imperfections: Taxes âĒ Taxes â US Tax Code: Deductibility of interest leads to lower cost of debt (Rd(1-t)) â Simple specification overvalues benefit âĒ Ignores personal taxes which â Decreases investors debt return â Increases investors preference for equity ïķ Capital gains: Defer and rate difference ïķ Dividend: Some portion is deductible

- 11. Market Imperfections: Contracting Costs âĒ In imperfect markets, alternative ways to contract optimal behavior are necessary âĒ Costs of financial distress â Underinvestment (rejecting NPV>0 projects), direct, indirect costs, etc. âĒ Benefits of debt â Monitoring function, manages free cash flow problem (Accepting NPV<0 projects), etc. âĒ Contracting costs and taxes are primary motives for static trade off theory debt

- 12. Market Imperfections: Information Costs âĒ With asymmetric information, leverage may reveal something about the existing firm âĒ Market timing: Managers take advantage of superior information â Issue equity when it is overvalued â Issue debt when it is undervalued âĒ Signaling: Managers use financing to signal future prospects of firms â Issue equity to signal good growth opportunities (preserve financial flexibility) â Issue debt when expected cash flows are strong and stable âĒ Motivates Pecking Order Theory

- 13. Can we quantify the value of market imperfections? Debt adds value to the firm due to the interest deductibility (assume taxes only) Assume the simple case: ) (TaxShield PV V V U L ïŦ ï― C D C D D r D r TaxShield PV ïī ïī ï― ï― ) (

- 14. Firm Value: Perfect Capital Markets 50 70 90 110 130 150 170 190 0% 25% 50% 75% 100% D/E Value V(Unlevered) V(Levered)

- 15. More Complex Tax Shields âĒ Uneven and/or limited time payments â Discount all flows back to time 0 âĒ What r do you use? â Certain the tax shield can be used: rD â Uncertain? Higher r

- 16. Financial Distress âĒ As leverage increases, the probability therefore PV of financial distress increases ) ( ) ( t istressCos FinancialD PV TaxShield PV V V U L ïŦ ïŦ ï― âĒ How do we estimate the cost of distress? â Prob(Distress)*Cost of Distress âĒ Probability can be estimated in several ways â Logit/Probit regressions â Debt ratings

- 17. Firm Value: with Taxes and Fiancial Distress 50 70 90 110 130 150 170 190 D/E D/E V(Unlevered) V(Levered) V(Distress)

- 18. Financial Distress: Bankruptcy Costs âĒ Direct Costs â Legal, accounting and other professional fees â Re-organization losses â Estimated btw 4-10% of firm value (t-3) âĒ Indirect Costs â Reputation costs â Market share â Operating losses â Estimated as 7.8% of firm value (t-2)

- 19. Financial Distress: Agency Costs âĒ Risk shifting and asset substitution â Shareholders invest in high risk projects and shift risk to the debt holders â Shareholders issue more debt, diminishing old debt holders protection âĒ Underinvestment âĒ Expropriating funds âĒ Difficult to estimate

- 20. Other Advantages of Debt âĒAgency cost of Equity (motive) â Shirking is less likely when issuing debt â Perquisites are less likely with debt â Over-investment is less likely with debt âĒAgency cost of Free Cash Flow (opportunity) â Retained earnings versus dividends? â Growth and investment opportunities âĒDebt serves as a monitoring device, decreasing managerial discretion âĒBankruptcy as a strategic move???

- 21. Formal Models of Capital Structure âĒ Pecking Order â Firms prefer to raise capital âĒInternally generated funds âĒDebt âĒEquity â Implies capital structure is derived from âĒFinancing needs and capital availability âĒDynamic rather than static âĒAsymmetric information and signaling âĒ Static Trade Off

- 22. Static trade-off theory of debt Maximum Firm Value Firm Value Debt Optimal amount of Debt Actual Firm Value

- 23. Implications of Static Trade Off âĒ Static rather than dynamic âĒ Taxes and Contracting Cost drive value âĒ Readjustment may be sticky â Optimal trade off between cost of issuances and benefit of capital structure âĒ Insights â Large, stable profit firms will have more debt â Higher the costs of distress lower debt â Lower taxes, lower debt â Less (more) favorable tax treatment of debt (equity), lower debt

- 24. Evidence: Taxes âĒ This method usually overestimates the tax consequence â Magnitude of leverage differences across countries and tax regimes is not that big â Equity taxes (personal taxes) are overestimated (Miller) âĒ Timing of capital gains âĒ Higher effective marginal tax rate, higher the leverage (Graham, 2001)

- 25. Evidence âĒ Contracting Costs: Consistent evidence â Higher (lower) the growth opportunities, higher (lower) the potential underinvestment problem, lower (higher) the leverage â Higher growth opportunities would prefer âĒ Shorter maturity debt (or call provisions) âĒ Less restrictive covenants âĒ More convertibility provisions âĒ More concentrated investors (private) âĒ Information costs â Consistent with market timing (SEOâs lead to -3% return) â Inconsistent with signaling and pecking order âĒ Taxes: Higher effective marginal tax rate, higher the leverage

- 26. MM: Proposition II âĒ How does leverage affect rE âĒ Start with the WACC âĒ Solve for rE âĒ The rate of return on the equity of a firm increases in proportion to the debt to equity ratio (D/E). D E a r V D r V E r ïŦ ï― ) ( D a a E r r E D r r ï ïŦ ï―

- 27. MM: Proposition II (with taxes) D c E a r V D r V E r ) 1 ( ïī ï ïŦ ï― ) )( 1 ( D a c a E r r E D r r ï ï ïŦ ï― ïī

- 28. âĒ Blue Inc. has no debt and is expected to generate $4 million in EBIT in perpetuity. Tc=30%. All after-tax earnings are paid as dividends.The firm is considering a restructuring, with a perpetual fixed $10 million in floating rate debt at an expected interest rate of 8%. The unlevered cost of equity is 18%. âĒ What is the current value of Blue? âĒ What will the new value be after the restructuring? âĒ What will the new required return on equity be? âĒ What if we use the new WACC?

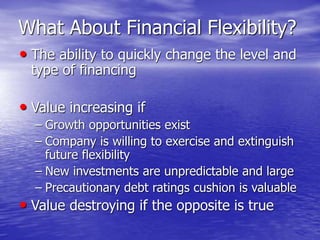

- 29. What About Financial Flexibility? âĒ The ability to quickly change the level and type of financing âĒ Value increasing if â Growth opportunities exist â Company is willing to exercise and extinguish future flexibility â New investments are unpredictable and large â Precautionary debt ratings cushion is valuable âĒ Value destroying if the opposite is true

- 30. How do we value financial flexibility?

- 31. What do we do? âĒ Choosing a target capital structure â Minimize taxes and contracting costs (while paying attention to information costs) â Target ratio should reflect the companyâs âĒ Expected investment requirements âĒ Level and stability of cash flows âĒ Tax status âĒ Expected cost of financial distress âĒ Value of financial flexibility âĒ Dynamic management â Financing is typically a lumpy process â Find optimal point where cost of adjusting capital structure is equal to cost of deviating from target

Editor's Notes

- #2: Notes-Capital Structure

- #3: Notes-Capital Structure

- #4: Notes-Capital Structure

- #5: Notes-Capital Structure

- #6: Notes-Capital Structure

- #7: Notes-Capital Structure

- #8: Notes-Capital Structure

- #9: Notes-Capital Structure

- #10: Notes-Capital Structure

- #11: Notes-Capital Structure

- #12: Notes-Capital Structure

- #13: Notes-Capital Structure

- #14: Notes-Capital Structure

- #15: Notes-Capital Structure

- #16: Notes-Capital Structure

- #17: Notes-Capital Structure

- #18: Notes-Capital Structure

- #19: Notes-Capital Structure

- #20: Notes-Capital Structure

- #21: Notes-Capital Structure

- #22: Notes-Capital Structure

- #23: Notes-Capital Structure

- #24: Notes-Capital Structure

- #25: Notes-Capital Structure

- #26: Notes-Capital Structure

- #27: Notes-Capital Structure

- #28: Notes-Capital Structure

- #29: Notes-Capital Structure

- #30: Notes-Capital Structure

- #31: Notes-Capital Structure

- #32: Notes-Capital Structure