More Related Content

Similar to H1FY24 MPS Press Conference Presentation.pptx (20)

Recently uploaded (20)

H1FY24 MPS Press Conference Presentation.pptx

- 1. 18 June 2023 Bangladesh Bank

- 2. 2 ŌĆó Y ear 2020 : COVID-19 : Massive disruptions in livelihood ŌĆōhealth system breakdown and economic collapse; ŌĆó Y ear 2021 : Recovery from COVID-19; ŌĆó Y ear2022 : Russia-Ukraine Crisis provoking global economic and financial sanctions; ŌĆó Y ear 2023 : Looming uncertainties with possible global economic recession. ŌĆó Outcome and Policy Response - 1 ’ā╝ Very low inflation and output ’ā╝ QE & near zero interest rate ŌĆó Outcome and Policy Response - 2 ’ā╝ Growing inflation and output ’ā╝ QE & near zero interest rate ŌĆó Outcome and Policy Response - 3 ’ā╝ Skyrocketing inflation and moderate output growth ’ā╝ QT & aggressive policy rate hikes ŌĆó Outcome and Policy Response - 4 ’ā╝ High inflation and ER pressure ’ā╝ Contractionary policy stances Global Context of H1FY24 MPS

- 3. Global Growth Situation 3 Region Act. Act. Proj. Proj. CY21 CY22 CY23 CY24 World 6.3 3.4 2.8* 3.0* USA 5.9 2.1 1.6* 1.1* Euro Area 5.4 3.5 0.8* 1.4* China 8.4 3.0 5.2* 4.5* India 9.1 6.8 5.9* 6.3* FY21 FY22 FY23 FY24 Bangladesh 6.9 7.1 5.50* 6.5* 6.03** 7.5** (In percent) Source: IMF. *April 2023 WEO, IMF. **GoB.

- 4. Global Price Situation Point-to-Point Inflation (in percent) Item Jun 20 Jun 21 Jun 22 May 23 Energy -36.4 93.6 84.7 -40.8 Non-energy -3.5 43.8 12.0 -170 Food -2.3 34.3 23.5 -21.3 Rice 13.6 -5.3 2.3 17.0 Source: World Bank and FAO. 4 111.6 97.0 180 150 120 90 60 30 0 Dec- 19 Jun-20 Dec- 20 Jun-21 Dec- 21 Jun-22 Dec- 22 May-23 Index Commodity Price Index (Base: 2010 =100) Energy Non-energy Source: World Bank 127.8 124.3 80 100 120 140 160 Dec- 19 Jun-20 Dec- 20 Jun-21 Dec- 21 Jun-22 Dec- 22 May-23 Index Food Price Index (Base: 2014-2016=100) Food Rice Source: FAO

- 5. Inflation in Major Economies 5 Region Act. Act. Act Act. Proj. Proj. CY20 CY21 Jun 22 Apr 23 CY23 CY24 USA 1.2 4.7 9.1 4.9 4.5* 2.3* Euro Area 0.3 2.6 8.6 6.1# 5.3* 2.9* UK 0.9 2.6 8.2 8.7 6.8* 3.0* India 6.2 5.5 7.0 4.7 4.9* 4.4* FY20 FY21 FY22 May 23 FY23 FY24 Bangladesh 5.65 5.56 6.15 8.84 7.5** 6.0** Source: IMF. *April 2023 WEO, IMF. **GoB. # May 2023. (In percent)

- 6. Policy Rate in Major Economies 6 (In percent) Region Dec 21 Jun 22 Dec 22 May 23 USA (FFR) 0.00-0.25 1.50-1.75 4.25-4.50 5.00-5.25 Euro Area (FRT) 0 0 2.50 3.75 UK (BR) 0.25 1.25 3.50 4.50 India (repo) 4.00 4.90 6.25 6.50 Bangladesh (repo) 4.75 5.50 5.75 6.00 Source: BIS.

- 7. Local Context of H1FY24 MPS 7 ŌĆó High inflationary and exchange rate pressures. ŌĆó Substantial erosion of foreign exchange reserves. ŌĆó Larger BOP deficits (combine effects of CAB and FAB deficits) ŌĆó High non-performing loans. ŌĆó Tight liquidity situation. ŌĆó Relatively higher interest rates across all areas.

- 8. Domestic Inflation Scenario 9.96% 9.94% 9.24% 2% 4% 6% 8% 10% Jun-19 Dec- 19 Jun-20 Dec- 20 Jun-21 Dec- 21 Jun-22 Dec- 22 May-23 Point to Point Inflation General Food Non-Food Jun-19 8 Dec- 19 Jun-20 Dec- 20 Jun-21 Dec- 21 Jun-22 Dec- 22 May-23 Average Inflation 10% 9.12% 8.84% 8.60% 8% 6% General Food Non-Food 4%

- 9. Liquidity Situation of Banks and Interest Rate Scenario Item Jun 20 Jun 21 Jun 22 May 23 Excess cash reserves 23,847 62,498 26,876 9,373 Excess liquid assets 1,39,578 2,31,463 2,03,435 1,63,682 Source: DOS, BB (Crore Taka) 9 Item Jun 21 Jun 22 Dec 22 June 23 Call money rate 2.23 4.42 5.80 6.03* Lending rate 7.33 7.09 7.22 7.29@ Deposit rate 4.13 3.97 4.23 4.38@ 91-Day TB rate 0.35 5.95 6.90 6.75* 182-Day TB rate 0.68 6.44 7.30 7.07* Source: BB. @ Apr 2023. * 12 June 2023.

- 10. External Sector Development 10 (Billion USD) Indicator FY Import 5 (- Export 3 (-1 Remittance 1 (1 CAB - FAB 7 Overall Balance 3 Net FX Sale -0 FX Reserves 3 BDT/USD (inter-bank rate) 84 Source: BB. Note: Figures in the parentheses indicate % growth. # as of Apr-23 *Up to 12 June 2023, @ up to 14 June 2023.

- 11. Recent Policy Initiatives 11 ŌĆó To control inflation. ŌĆó To improve the current account balance. ŌĆó To manage exchange rate instability and foreign exchange reserves. ŌĆó To stabilize the financial sector. ŌĆó To strengthen the capital market. Containing demand and making supply side interventions

- 12. Recent Policy Initiatives (1) 12 ŌĆó Raising the policy rate (repo rate) by 25 basis point to 6.0 percent on 16 January 2023. ŌĆó Quantitative tightening through selling huge foreign currencies to banks. ŌĆó Supporting the productive economic sector, including agriculture, CMSMEs, import-substitute and export-oriented industries through various refinance schemes/pre-finance schemes. ŌĆó Relaxing the disbursement policy of refinance scheme for CMSME sector. ŌĆó Formulating the Agricultural Development Common Fund (BBADCF) to increase agricultural output. ŌĆó Introducing the Mudarabah liquidity support (MLS) and Islamic Banks Liquidity Facility (IBLF) for the Shariah- based Islamic banks. ŌĆó Allowing the borrowing from OBU. ŌĆó Establishing the Export Facilitation Pre-finance Fund (EFPF). ŌĆó Introducing the credit guarantee scheme (CGS) for CMSMEs loans.

- 13. Recent Policy Initiatives (2) 13 ŌĆó Discouraging unnecessary and luxury imports. ŌĆó Strengthening the monitoring and price verification of imports. ŌĆó Strengthening the monitoring on foreign exchange dealings by banks and money changers. ŌĆó Reducing the cash foreign currency holdings by money changers. ŌĆó Taking crackdown measures on illegal money changers and MFS providers to mitigate unauthorized and hundi- related transactions. ŌĆó Restricting the all sorts of foreign tours by officials in banks (including BB) and NBFIs. ŌĆó Enforcing 180 days limit for export proceeds repatriation by fixing the exchange rate at 180th day. ŌĆó Reducing the export retention quota and banksŌĆÖ net openposition. ŌĆó Enhancing the interest rate on loans from export development fund. ŌĆó Raising the cash incentive rate (2.5 percent) on inward remittances.

- 14. Recent Policy Initiatives (3) 14 ŌĆó Easing the remittance repatriation and cash incentive distribution process and drawing arrangements with foreign exchange houses. ŌĆó Allowing the mobile financial services in remittance collection and distribution process. ŌĆó Waiving the remittance transaction fees by local banks. ŌĆó Liberalizing the NRBŌĆÖs investment procedure including opening of FC account (PP in place of NID). ŌĆó Enhancing the interest rate on non- resident foreign currency deposits. ŌĆó Allowing Bangladesh Taka (BDT) to depreciate consistent with the market force. ŌĆó Making the MoU with state-owned and private commercial banks with a view to reduce NPL at a certain level and improve the good governance. ŌĆó Taking initiative to amend 5 Acts, related to financial sector, to address financial sector issues. ŌĆó Taking initiative to streamline the appointment of Directors in NBFIs. ŌĆó Ensuring enough liquidity in the capital market. ŌĆó Introduction MI module to develop secondary market for BGTBs.

- 15. New Policy Initiatives 15 1. Adopting a new monetary policy framework by shifting from monetary targeting to interest rate targeting and introducing an interest rate corridor considering the interbank call money rate as the operating target of monetary policy. 2. Taking the decision to increase the policy rates, i.e., repo rate by 50 bps, the reverse repo rate by 25 bps, the special repo adjusted downward to 8.50 percent. 3. Removing the lending rate cap and replacing it with a competitive and market-based reference rate along with a margin 4. Moving towards a market-driven unified and single exchange rate regime to ensure stability in the foreign exchange market, improve the BoP conditions, and protect FX reserves.

- 16. New Monetary Policy Framework 16 Instruments ŌĆó Policy rate ŌĆó Open market operations ŌĆó Reserve requirement ŌĆó Bank rate Operating target ŌĆó Interbank call money rate as a counterpart of short-term interest rate Information variable ŌĆó Inflation forecasts ŌĆó GDP forecasts ŌĆó Money and credit situation ŌĆó BoP outlook Primary monetary policy objective ŌĆó Price stability ŌĆó Financial stability ŌĆó Economic growth

- 17. Interest Rate Corridor 8.50% 6.50% 4.50% Standing Lending Facility Rate(Ceiling) Policy Rate Standing Deposit Facility Rate (Floor) Call Money Rate 17

- 18. Reference Lending Rate 18 ŌĆó The reference lending rate will be known as SMART (Six- month Moving Average Rate of Treasury bill) to be announced monthly through the BB website. ŌĆó SMARTplus a margin of up to 3.00 percent will be applicable for banks, and SMART plus a margin of up to 5.00 percent will be applicable for NBFIs. ŌĆó The lending activities for CMSMEs and consumer loans may be subject to an additional fee of up to 1.00 percent to cover supervision costs and there will be no changes in the interest rates applicable to credit card loans.

- 19. Exchange Rate Unification and GIR Calculation 19 ŌĆó BB will adopt a unified and market-driven single exchange rate regime, allowing the exchange rate between BDT and USD or any other foreign currency to be determined by market forces. ŌĆó Starting from 1 July 2023, BB will no longer sell any forex at a discounted rate. ŌĆó BB will compile and publish gross international reserves (GIR) in line with the BPM6 while keeping track of the current practice of calculating and reporting total foreign assets.

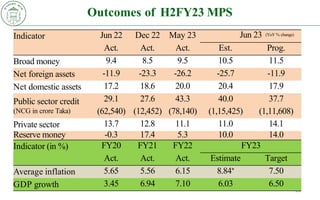

- 20. Outcomes of H2FY23 MPS 20 Indicator Jun 22 Dec 22 May 23 Jun 23 (YoY % change) Act. Act. Act. Est. Prog. Broad money 9.4 8.5 9.5 10.5 11.5 Net foreign assets -11.9 -23.3 -26.2 -25.7 -11.9 Net domestic assets 17.2 18.6 20.0 20.4 17.9 Public sector credit (NCG in crore Taka) 29.1 (62,540) 27.6 (12,452) 43.3 (78,140) 40.0 (1,15,425) 37.7 (1,11,608) Private sector 13.7 12.8 11.1 11.0 14.1 Reserve money -0.3 17.4 5.3 10.0 14.0 Indicator (in %) FY20 FY21 FY22 FY23 Act. Act. Act. Estimate Target Average inflation 5.65 5.56 6.15 8.84* 7.50 GDP growth 3.45 6.94 7.10 6.03 6.50

- 21. Monetary and Credit Projections for FY24 21 (In percent) Item Jun-22 Act. Dec-22 Act. May-23 Act. Jun-23 Est. Dec-23 Proj. Jun-24 Proj. (Pr. Jun.23) Broad money 9.4 8.5 9.5 10.5 9.5 10.0 (11.5) Net Foreign Assets* -13.5 -25.0 -27.8 -26.2 -20.3 4.9 (-11.9) Net Domestic Assets 19.7 21.8 22.4 22.4 16.8 11.0 (17.9) Domestic Credit 16.2 15.1 16.7 16.4 16.9 15.3 (18.5) Credit to the public sector 29.1 27.6 43.3 40.0 43.0 30.0 (37.7) Credit to the private sector 13.7 12.9 11.1 11.0 10.9 11.0 (14.1) Reserve money -0.3 17.4 5.3 10.0 0.0 6.0 (14.0) Money multiplier 4.93 4.63 5.23 4.95 5.07 5.14 (4.82) Source: Bangladesh Bank. *Calculated using the estimated constant exchange rates of end June 2023.

- 22. Objective and Stance of H1FY24 MPS 22 ŌĆó This MPS gives the highest priority in taming inflation by containing the aggregate demand while making the supply-side intervention by ensuring required the flow of funds to the productive sector, including agriculture, CMSMEs, import substitutes and export-oriented industries and services. ŌĆó BB will adopt a unified and market-driven single exchange rate regime to contain exchange rate pressure. With a substantial depreciation of BDT against USD, the exchange rate is staying around Tk. 108.0/$ - very close to the prevailing market conditions as supported by REER based exchange rate and BBŌĆÖs in-house research, requiring no major depreciation at this moment. ŌĆó Given above policy objectives, BB intends to adopt a contractionary monetary policy stance to bring down the rate of inflation to a desired level, while remain supportive to the investment and employing generating activities.

- 23. Near-term Macroeconomic Challenges 23 ŌĆó Near-term macroeconomic challenges are: containing inflation and managing exchange rate pressure. ŌĆó To tackle these challenges, BB is adopting a tight monetary policy stance. The ultimate success of this policy stance, however, depends on a few critical factors: ’ā╝ Effectiveness of the new policy initiatives. ’ā╝ Maintaining the exchange rate stability alongside a surplus financial account. ’ā╝ A pause in the policy rate hike race among the central banks of major economies including the US FED, ECB, etc. ŌĆó Given the favorable developments of these factors, BB aims to tackle inflation and exchange rate pressures while fostering a stable and resilient macroeconomic environment.

- 24. Thank You All