More Related Content

What's hot (20)

Similar to Lloyds Bank Optimising Liquidity and Yield (20)

Lloyds Bank Optimising Liquidity and Yield

- 1. OPTIMISING LIQUIDITY & YIELD SME April 2016

- 2. BEYOND CREDIT RATINGS 2 Output Qualitative Factors Credit Ratings Institution/Limits LiquidityFunding Lending Exposure 6 Factor Quantitative Framework Basel III Relationship strength, operational reach, news flow and ease of business Input Combining traditional measures with these factors provides a strong framework to set counterparty limits Market Data Capital Buffer Regulatory Environment An approach to assessing and monitoring your bank limits beyond traditional Credit Ratings

- 3. LOW RISK BUSINESS MODEL 3 Increasing recognition of balance sheet strength and de-risking through best in peer group CDS* Apr-2012 101 301 15 417 Apr-2013 50 156 15 221 Apr-2014 53 74 15 142 Apr-2015 57 60 15 132 Apr-2016 59 102 15 176 15/04/16 EXAMPLE: 5YR Wholesale Deposit (bps) PERIOD 3MTH LIBOR LLOYDS BANK CDS ARRANGEMENT FEE TOTAL DIFFERENTIAL Source: Bloomberg Data & Lloyds Bank analytics as -241 Lloyds Bank PLC 102.497 Banco Santander SA 124.779 Santander UK PLC 90.456 Barclays Bank PLC 125.947 Royal Bank Of Scotland PLC 124.573 HSBC Holdings PLC 98.39 Source: Bloomberg Data as at 15/04/16 INSTITUTION CDS (bps) *CDS: A credit default swap is a particular type of swap designed to transfer the credit exposure of fixed income products between two or more parties.

- 4. SUMMARY OF RISK FACTORS LONG TERM SHORT TERM LONG TERM SHORT TERM LONG TERM SHORT TERM Lloyds Bank PLC ┬Ż49,303.71 16 4.80% 13.00% A1 P-1 A+ F1 A A-1 102.497 Banco Santander SA ┬Ż46,678.65 18 4.70% 10.05% A3 P-2 A- F2 A- A-2 124.779 Santander UK PLC N/A N/A 4.00% 11.60% A1 P-1 A F1 A A-1 90.456 Barclays Bank PLC ┬Ż28,191.15 40 4.20% 11.10% A2 P-1 A F1 A- A-2 125.947 HSBC Holdings PLC ┬Ż88,486.56 9 5.00% 11.90% Aa2 P-1 AA- F1+ AA- A-1+ 98.39 Royal Bank Of Scotland PLC ┬Ż26,773.86 44 5.60% 15.50% A3 P-2 BBB+ F2 BBB+ A-2 124.573 15/04/16 FITCH S&P'S CDS Source: Bloomberg data as of INSTITUTION MARKET CAP (MN) MARKET CAP (RANKING) (1) LEVERAGE RATIO (2) FULLY LOADED TIER 1 (3) MOODY'S A typical risk summary used by treasury teams to help determine Bank limits for deposits 3. The Fully Loaded Tier 1 Ratio measures a bank's core equity capital compared with its total risk-weighted assets. This provides a form of measure of a bank's capital adequacy or financial strength. 1. Ranking is based on the largest market capitalised banks (1731) in the world 2. The Basel III leverage ratio is defined as the Capital Measure (the numerator) divided by the Exposure Measure (the denominator), with this ratio expressed as a percentage. The basis of the calculation is the average of the three month-end leverage ratios over a quarter. The ratio provides a form of measure of the bankŌĆÖs capital compared with its financial leveraging and the bankŌĆÖs ability to meet financial obligations. 4

- 5. HSBC Bank PLC Lloyds Bank PLC Santander UK PLC Banco Santander SA Barclays Bank PLC RBS PLC Fitch (review date 19th May 2015) Moody's (review date 28th May 2015) S&P (review date 9th June 2015) FITCH LONG TERM SENIOR DEBT RATING OF LLOYDS BANK PLC & LLOYDS BANKING GROUP UPGRADED TO ŌĆśA+ŌĆÖ FROM ŌĆśAŌĆÖ (19TH MAY 2015) MOODYŌĆÖS LONG-TERM SENIOR DEBT AND DEPOSIT RATINGS OF LLOYDS BANK PLC CONFIRMED AT ŌĆśA1 / P-1ŌĆÖ & OUTLOOK UPGRADED TO POSITIVE (28TH MAY 2015) S&P LLOYDS SENIOR DEBT RATING ARRIFMED AT ŌĆśAŌĆÖ (OUTLOOK STABLE) ON CONCLUSION OF SOVEREIGN SUPPORT REVIEW (9TH JUNE 2015) CREDIT RATING AGENCIES ACTIONS 2015 5 AA- Aa2 AA- A+ A1 A A A1 A A A2 A- A- A3 BBB+ A3 BBB+BBB+ One notch upgrade One notch downgrade Revised rating landscape following Agencies removal of UK Bank assumed Sovereign support post implementation of BRRD regulation Spain not yet adopted BRRD therefore not assessed

- 6. LOW RISK BUSINESS Mortgage credit quality continues to improve with book supported by employment trends and low interest rates 6 LBG: Lloyds Banking Group LTV: Loan to Value HPI: House Price Index Source: Lloyds Banking Group FY2015 Results.

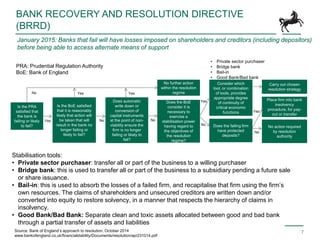

- 7. Is the PRA satisfied that the bank is failing or likely to fail? Is the BoE satisfied that it is reasonably likely that action will be taken that will result in the bank no longer failing or likely to fail? Does automatic write down or conversion of capital instruments at the point of non- viability ensure the firm is no longer failing or likely to fail? Does the BoE consider it is necessary to exercise a stabilisation power having regard to the objectives of the resolution regime? Does the failing firm have protected deposits? Consider which tool, or combination of tools, provides appropriate degree of continuity of critical economic functions No action required by resolution authority Place firm into bank insolvency procedure, for pay- out or transfer Carry out chosen resolution strategy No further action within the resolution regimeNo Yes Stabilisation tools: ŌĆó Private sector purchaser: transfer all or part of the business to a willing purchaser ŌĆó Bridge bank: this is used to transfer all or part of the business to a subsidiary pending a future sale or share issuance. ŌĆó Bail-in: this is used to absorb the losses of a failed firm, and recapitalise that firm using the firmŌĆÖs own resources. The claims of shareholders and unsecured creditors are written down and/or converted into equity to restore solvency, in a manner that respects the hierarchy of claims in insolvency. ŌĆó Good Bank/Bad Bank: Separate clean and toxic assets allocated between good and bad bank through a partial transfer of assets and liabilities January 2015: Banks that fail will have losses imposed on shareholders and creditors (including depositors) before being able to access alternate means of support Yes Yes No No No Yes Yes No ŌĆó Private sector purchaser ŌĆó Bridge bank ŌĆó Bail-in ŌĆó Good Bank/Bad bank PRA: Prudential Regulation Authority BoE: Bank of England Source: Bank of EnglandŌĆÖs approach to resolution, October 2014 www.bankofengland.co.uk/financialstability/Documents/resolution/apr231014.pdf BANK RECOVERY AND RESOLUTION DIRECTIVE (BRRD) 7

- 8. Bail-in order of priority (from January 2015) *Interest incurred post-insolvency and liquidators will only arise in the event of liquidation where both will belong to the holding company 1 2 3 4 5 7 8 9 6 10 Source: Bank of EnglandŌĆÖs approach to resolution, October 2014 www.bankofengland.co.uk/financialstability/Documents/resolution/apr231014.pdf Shareholders (ordinary shares) Shareholders (preference shares) Interest Incurred post-insolvency* Unsecured subordinated creditors (eg subordinated bondholders) Unsecured Senior Creditors Floating charge holders Preferential creditors (secondary) Preferential creditors (ordinary) Liquidators* Fixed charge holders BANK RECOVERY AND RESOLUTION DIRECTIVE (BRRD) 8 Potential running order of a Bail In with supporting ring fence structure

- 9. Bail-In Waterfall (2) 12.0 2.1 Tier 2 ECN tier 2 Fully loaded CET1 Tier 1 18.8 2.7 1.4 10.3 Dec 2013 pro forma 4.4 CET1* and total capital vs. peers(1) (%) 2015 CAPITAL POSITION OF PEER BANKS 9 Lloyds Banking Group is a strongly capitalised bank within its peer group with a ┬Ż81bn Bail In buffer Bail-In ┬Ż28.5bn ┬Ż19.5bn ┬Ż33.0bn ┬Ż222.0bn ┬Ż229.0bn ┬Ż33.0bn Equity Capital Sub Debt Senior Unsecured greater than one year Unsecured Funding (e.g. Corporate & Local Authority Deposits) FSCS (Retail) Secured Funding ┬Ż81BN 1) Peers are RBS, Barclays and HSBC as reported at Q3 2015 and Standard Chartered at HY 2015 2) Lloyds Banking Group as of 31st December 2015 3) LBG: 13.0% pro forma *CET1: A measurement of a bank's core equity capital compared with its total risk-weighted assets. This is the measure of a bank's financial strength.

- 10. ┬Ż10 loss ------------------ ------------------ ┬Ż300 assets ┬Ż290 assets ┬Ż290 assets ┬Ż3 sub-debt ┬Ż2 sub-debt ┬Ż10 loss on assets ┬Ż10 loss on assets ┬Ż120 deposits ┬Ż128 other liabilities ┬Ż9 Equity ┬Ż40 senior liabilities of which ┬Ż10 unsecured ┬Ż40 senior liabilities of which ┬Ż10 unsecured ┬Ż33 senior liabilities of which ┬Ż3 unsecured ┬Ż9 Equity ┬Ż120 deposits ┬Ż128 other liabilities ┬Ż120 deposits ┬Ż128 other liabilities Worked Bail In Example Bank PLC has a balance sheet worth ┬Ż300, funded by equity of ┬Ż9 and other liabilities of ┬Ż291. Bank PLC incurs losses on its assets of ┬Ż10, ┬Ż9 of equity and ┬Ż1 sub-debt are written down to absorb the ┬Ż10 loss. This reduces the assets and liabilities to ┬Ż290. The new balance sheet to meet the PRAŌĆÖs capital requirements. The ┬Ż9 of equity and ┬Ż1 of sub-deb have been written off to absorb the ┬Ż10 loss. Consequently, ┬Ż7 of unsecured senior liabilities and ┬Ż2 of sub-debt is converted to equity. 1 2 3 Source: Bank of EnglandŌĆÖs approach to resolution, October 2014 www.bankofengland.co.uk/financialstability/Documents/resolution/apr231014.pdf 1 2 3 ┬Ż300 ┬Ż300 Net ┬Ż290/Gross ┬Ż300 ┬Ż290 ┬Ż290 ┬Ż290 BANK RECOVERY AND RESOLUTION DIRECTIVE (BRRD) 10

- 11. PRUDENTIAL REGULATION AUTHORITY (PRA) STRESS TEST SCENARIOS 2014 11 Sourced from the Bank of England site (16/12/2014). http://www.bankofengland.co.uk/financialstability/Documents/fpc/keyelements.pdf Annual GDP Annual Inflation Unemployment HPI & CRE Analysis of key metrics used by PRA HPI: -35 CRE: -30% +5.2% -3.9% +5.9% -3.9% SCENARIOSCAPITALRULESMETHODOLOGY Key UK economic metrics (to trough): ’é¦ GDP (Gross Domestic Product): 3.9% ’é¦ CPI rate: 6.5% ’é¦ Unemployment: +5.2% ’é¦ HPI (House Price Index): -35% ’é¦ CRE (Commercial Real Estate) : -30% ’é¦ Base Rate: 4.25% ’é¦ Equities: -28% Market shock assessed against EBA (European Banking Authority) scenarios. ’é¦ PRA implementation of CRDIV (Capital Requirement Regulation & Directive) Capital Rules as outlined in PS 7/13 ’é¦ No prudential filter applied for AFS assets ’é¦ Hurdle rates CET1 > 7% base, > 4.5% stress ’é¦ Leverage ratio > 3% in base. No hurdle in stress ’é¦ Dynamic balance sheet with deleveraging restrictions. ’é¦ No post 31-Dec capital actions included (balance sheet as of close 31 Dec 13) ’é¦ Securitisation & Market risk methodology aligned to EBA. ’é¦ No additional methodology restrictions

- 12. PRUDENTIAL REGULATION AUTHORITY (PRA) STRESS TEST SCENARIOS 2015 12Sourced from Bank of England site (01/12/2015). http://www.bankofengland.co.uk/financialstability/Documents/fpc/results011215.pdf Analysis of key metrics used by PRA -3.9% SCENARIOSCAPITALRULESMETHODOLOGY Key UK economic metrics (to trough): ’é¦ Oil falls to USD 38p/b ’é¦ World GDP falls 7% from IMF World economical forecast ’é¦ China house prices ŌĆō 35% ’é¦ Hong Kong CRE ŌĆō 45% ’é¦ China GDP slows from 7.5% to 1.7% ’é¦ CPI rate: -1.0% ’é¦ UK house prices: -20% ’é¦ UK Base Rate: 0% ’é¦ CET1 ratio > 4.5% of RWAs ’é¦ New Threshold for 2015 ŌĆō 3% of leverage exposure measure ’é¦ Stress scenario would reduce aggregate CET1 ratio across 7 banks from 11.2% to low of 7.6% in 2016 ’é¦ Aggregate Tier 1 leverage ratio falls from 4.4% at the end of 2014 to low of 3.5% in 2016 ’é¦ Designed to assess resilience of UK banks ’é¦ 2015 stress test has 3 main components: 1. Macroeconomic factors 2. Trade risk element of stress 3. Stressed projections for potential misconduct ’é¦ In house modelling played a greater role than 2014 test CPI and Bank Rate in the UK in the 2014 and 2015 stress scenarios Differences in severity of GDP shocks between the 2014 and 2015 stress tests Projected cumulative five-year impairment charges in China and Hong Kong UK residential property price index and commercial real estate index in the 2014 and 2015 stress scenarios

- 13. PRUDENTIAL REGULATION AUTHORITY (PRA) STRESS TEST ŌĆō 2014 VS 2015 13 4.7% 5.0% 3.9% 5.0% 4.6% 5.0% 3.5% 4.2% 3.6% 4.1% 2.4% 3.9% 2.0% 2.9% 4.1% 3.5% 3.0% 3.2% 2.6% 3.3% 2014 2015 2014 2015 2014 2015 2014 2015 2014 2015 Lloyds Banking Group Royal Bank of Scotland HSBC Barclays Santander UK Leverage Ratio Leverage Ratio (PRA Stressed) PRA Stress Leverage Ratio Test Results 12.0% 13.7% 10.8% 12.7% 11.2% 11.8% 10.0% 11.1% 11.8% 11.7% 5.0% 9.5% 4.6% 5.9% 8.7% 7.0% 7.0% 6.8% 7.6% 9.5% 2014 2015 2014 2015 2014 2015 2014 2015 2014 2015 Lloyds Banking Group Royal Bank of Scotland HSBC Barclays Santander UK CET1 Ratio CET1 Ratio (PRA Stressed) PRA Stress CET1 Ratio Test Results Sourced from the Bank of England site (01/12/2015). http://www.bankofengland.co.uk/financialstability/Documents/fpc/results011215.pdf Past performance is not a guarantee of future results

- 14. BASEL III REPLACES INDIVIDUAL LIQUIDITY ADEQUACY STANDARD (ILAS) 14 Key changes for Bank stress event buffer *30 Day coverage period is called Liquidity Coverage Ratio (LCR) Cash comes in 2 types Basel III Coverage Period* ILAS Coverage Period Day 1 30 Days 94 Days 1 2 ’ü▒ Current A/C ’ü▒ Client A/C ’ü▒ Cash Management ’ü▒ Call A/C ’ü▒ Term / Notice ’ü▒ Current A/C ’ü▒ Client A/C ’ü▒ Cash Management * Subject to economic incentive guidelines for calculation of LCR Operational Investment Cash held contractually less than 30 days falls into the Basel III Coverage period

- 15. OUTFLOW COVERAGE: LIQUIDITY COVERAGE RATIO (LCR) 15 LCR 1 day to 30 days coverage duration Operational* ’ü▒Current A/C ’ü▒Client A/C ’ü▒Cash Mgmt Investment ’ü▒Call A/C ’ü▒Current A/C ’ü▒Client A/C ’ü▒Cash Mgmt Day 30 32 Days 95 Days 3 months 6 monthsDay 1 Notice A/CŌĆÖs 25% Outflow 40% Outflow Last 30 days of term deposits needs to be covered as Investment at 40% * Subject to economic incentive guidelines for calculation of LCR Until notice is given there is no coverage outflow Cash held contractually less than 30 days is now less attractive to deposit takers

- 16. OUR PRODUCT GUIDE 16 <3MTH Call Account Transactional Bank Account* <3MTH Fixed Term Deposit 32 Day Notice Account 3-12MTH Fixed Term Deposit 12MTH Fixed Term Deposit 12MTH+ Fixed Term Deposit OPERATIONAL CASH Generally required within 3 Months for day to day business CORE CASH Generally required between 3 to 12 Months not for day to day business STRATEGIC CASH Generally not required for at least 12 Months 3-12MTH 12MTH+ *Transactional Bank Account is not provided by Financial Markets and is available from your Local Relationship Management Team Deposit products available from Lloyds Banking Group

- 17. Description ’é¦ Variable interest rate is paid on funds that remain committed on a rolling 32 day basis ’é¦ Minimum of ┬Ż10ŌĆÖ000 and a maximum of ┬Ż5,000,000 1 can be withdrawn giving Lloyds Bank 32 calendar daysŌĆÖ notice, providing the remaining balance is over ┬Ż10,000 ’é¦ Interest is calculated by reference to the Bank of England Bank Rate ’é¦ 32 Day Notice Accounts are available in GBP only Benefits ’é¦ Participate fully in any increase in the Bank of England Bank Rate. ’é¦ Interest is paid to the account daily. Limitations and Risks ’é¦ The interest rate received on funds will decrease if the Bank of England Bank Rate decreases ’é¦ Funds are committed for a minimum period of 32 calendar days ’é¦ Once notice is given a Reversion Rate will be applied on the notice account balance. The Reversion Rate will apply for the entirety of the notice period. 32 DAY NOTICE ACCOUNT 17 32 Day Notice Account that pays a variable interest rate and has improved return over 32 day Fixed Term Deposit for the same tenor Quick Facts: Account Type Notice Deposit Currency GBP Minimum Notice Period 32 Days Interest Payment Frequency Daily Minimum Opening Balance 10,000 (┬Ż) Minimum Withdrawal Amount 10,000 (┬Ż) Minimum Account Balance 10,000 (┬Ż) Maximum Account Balance1 5,000,000 (┬Ż) GBP Interest Rate2 Variable interest rate tracking BoE Bank Rate with an agreed margin. Reversion Rate BoE Bank Rate 1. Larger amounts may be available at Lloyds BankŌĆÖs discretion 2. Indicative Interest Rate only. The Interest Rate will be agreed with you at account opening.

- 18. OPTION TO USE A LAYERED APPROACH 18 You can chose to use our layering deposit solution that may deliver flexibility of liquidity ŌĆó The example above left shows an example rolling layered deposit approach where we take an example ┬Ż1M portfolio, split out into 4 equal amounts and place into a 3, 6, 9 and 12 month deposits. ŌĆó On the maturity of each deposit there are two ways the deposits can be rolled: 1. Preserving current maturity Each deposit is then rolled at its maturity date into the same term. 2. Maximising Return When each deposit matures a new 12 month deposit is entered into. At any time there is a 3 month liquidity on ┬╝ of the portfolio. 0 5 10 15 Months 250 250 250 250 DepositSize┬Żk Rolling layered deposit ŌĆō initial set up 0 5 10 15 20 Months DepositSize┬Żk 1. Rolling and preserving current maturity 0 5 10 15 20 Months DepositSize┬Żk 2. Rolling into 12 month deposits This is a hypothetical illustration, actual results may vary 250 250 250 250 250 250 250 250 250 250 250 250 250 250 250 250 250 250 250 250 25 250 250250 250 250 250

- 19. CASH-FLOW VS YIELD PORTFOLIO REVIEW An approach to assessing cash-flow to potentially improve yield Typical deposit portfolio: Long Date (12m+) Medium Date (3m ŌĆō 11m) Short Date (1 day ŌĆō 3m) Call Operational Long Date (12m+) Medium Date (3m ŌĆō 11m) Call Revised deposit portfolio: ŌĆó Enhanced blended return = Y% Operational Short Date (1 day ŌĆō 3m) Supports payment profile Potential mix change but still supports payment profile 19 Return on capital Return on capital ŌĆó Blended return = X% ŌĆó Or ┬Żx return sum Please note this is for illustrative purposes only Scenario 1 Scenario 2

- 20. MONTHLY CASH-FLOW TOOL EXAMPLE 20 Change your return with Lloyds Bank Returns are based on current Lloyds Bank deposits rates. Past performance is not a guarantee of future results and potential returns and forecasts may not be achieved

- 21. UK OUTLOOK 21 Source: Lloyds Bank International Financial Outlook, April 2016 Forecast may not be achieved. Lloyds Banking Group house view on key rates

- 22. PROGRESS AGAINST STRATEGIC PRIORITIES 22 Source: Lloyds Banking Group FY2015 Results.

- 23. DISCLAIMER 23 This presentation is for information purposes only. It is intended as a summary only and whilst it contains some information about the potential risks and benefits of various financial instruments it should not of itself, form the basis for any investment decision. Whilst Lloyds Bank has exercised reasonable care in preparing this presentation and any views, analysis or other information expressed or presented are based on sources it believes to be accurate and reliable, no representation or warranty, express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. If you receive information from us which is inconsistent with other information which you have received from us, you should refer this to your Lloyds Bank Sales representative for clarification. Not all products or transactions will fulfill your requirements. You should be aware that any product or transaction which you enter into with us is, in the absence of any written agreement to the contrary, on the basis that you are able to make your own independent assessment and decision as to your requirements and whether that product or transaction fulfils those requirements. Your decision will be based on your own knowledge and experience and any professional advice which you may have sought in relation to the financial, legal, regulatory, tax or accounting aspects of the proposed product or transaction. Lloyds Bank, its directors, officers and employees accept no responsibility or liability for any loss (whether direct, indirect, consequential, loss of profit or damages) howsoever caused or howsoever arising, in relation to this presentation or any subsequent product or transaction entered into. Lloyds Banking Group plc and its subsidiaries may participate in benchmarks in any one or more of the following capacities; as administrator, submitter or user. Benchmarks may be referenced by Lloyds Banking Group plc for internal purposes or used to reference products, services or transactions which we provide or carry out with you. More information about Lloyds Banking Group plcŌĆÖs participation in benchmarks is set out in the Benchmark Transparency Statement which is available on our website. This communication does not constitute an offer to sell or a solicitation of an offer to buy securities in the United States (ŌĆ£USŌĆØ) and is not being directed at persons who are located in the US or who are US Persons, as defined in Rule 902 of Regulation S under the U.S Securities Act 1933, as amended (altogether, ŌĆ£US PersonsŌĆØ). Lloyds Bank is a trading name of Lloyds Bank plc and Bank of Scotland plc, which are both subsidiaries of Lloyds Banking Group plc. Lloyds Bank plc. Registered Office: 25 Gresham Street, London EC2V 7HN. Registered in England and Wales no. 2065. Bank of Scotland plc. Registered Office: The Mound, Edinburgh EH1 1YZ. Registered in Scotland no. SC327000. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority under registration numbers 119278 and 169628 respectively. (09.15).

- 24. 24