MoMo #9 - Barry O'Neill

0 likes280 views

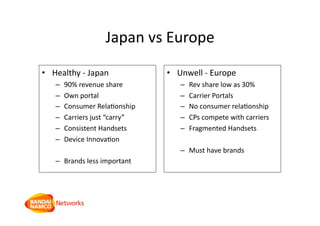

This document discusses differences between mobile game markets in Japan and Europe. Japan has a healthier market characterized by high (90%) revenue shares for content providers, direct consumer relationships without carrier portals, consistent handset support, and less emphasis on brands. Europe has an unwell market with low (30%) revenue shares, carrier portals that isolate consumers, fragmented handsets, and reliance on big brands. The document argues Europe needs a more pro-content provider model, direct consumer connections, open hosting platforms, and tighter handset management to foster innovation as seen in Japan with location-aware games, 3D games, and broader, less brand-focused services.

MoMo #9 - Barry O'Neill

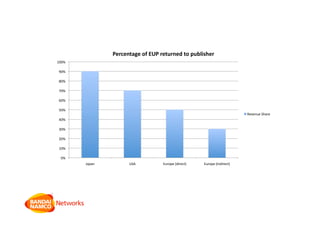

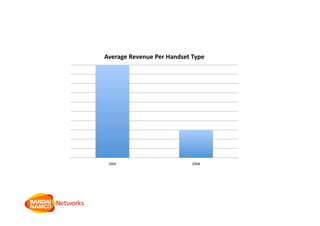

- 24. 0%âĐ 10%âĐ 20%âĐ 30%âĐ 40%âĐ 50%âĐ 60%âĐ 70%âĐ 80%âĐ 90%âĐ 100%âĐ JapanâĐ USAâĐ EuropeâĐ(direct)âĐ EuropeâĐ(indirect)âĐ PercentageâĐofâĐEUPâĐreturnedâĐtoâĐpublisherâĐ RevenueâĐShareâĐ

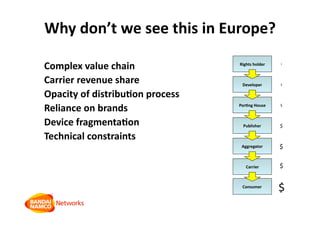

- 26. JapanâĐvsâĐEuropeâĐ âĒâŊ HealthyâĐââĐJapanâĐ ââŊ 90%âĐrevenueâĐshareâĐ ââŊ OwnâĐportalâĐ ââŊ ConsumerâĐRelaQonshipâĐ ââŊ CarriersâĐjustâĐâcarryââĐ ââŊ ConsistentâĐHandsetsâĐ ââŊ DeviceâĐInnovaQonâĐ ââŊ BrandsâĐlessâĐimportantâĐ âĒâŊ UnwellâĐââĐEuropeâĐ ââŊ RevâĐshareâĐlowâĐasâĐ30%âĐ ââŊ CarrierâĐPortalsâĐ ââŊ NoâĐconsumerâĐrelaQonshipâĐ ââŊ CPsâĐcompeteâĐwithâĐcarriersâĐ ââŊ FragmentedâĐHandsetsâĐ ââŊ MustâĐhaveâĐbrandsâĐ

- 28. 28

- 31. 31

- 32. 32

- 34. CreaQngâĐaâĐhealthyâĐmarket.âĐ âĒâŊ HealthyâĐmarketâĐkeyâĐcharacterisQcs.âĐ ââŊ ProâCPâĐrevâĐshare.âĐ ââŊ DirectâĐconnecQonâĐtoâĐcustomers.âĐ ââŊ OpenâĐpla_ormâĐ/âĐownâĐhosQng.âĐ ââŊ TightâĐhandsetâĐmanagement.âĐ âĒâŊ HealthyâĐmarketsâĐdemonstrate:âĐ ââŊ InnovaQonâĐââĐLocaQonâĐaware,âĐconnected,âĐ3D,âĐ mulQâmegabyteâĐïŽles.âĐ ââŊ ServicesâĐaimedâĐatâĐallâĐusers,âĐnotâĐjustâĐgamers.âĐ ââŊ NonâbrandâĐrelianceâĐââĐâĐ ââŊ StrongâĐrevenues.âĐ âĒâŊ iPhoneâĐDemonstratesâĐthatâĐthisâĐcanâĐbeâĐaâĐ possibilityâĐinâĐwesternâĐmarkets.âĐ